We would all like to follow the rules and laws we wish existed instead of the ones that actually exist. That’s just what the Office of the U.S. Trade Representative (USTR) is trying to pull off in its defense of Section 122 “balance-of-payments” (BoP) tariffs.

Earlier this year, the Supreme Court disallowed President Trump’s massive “Liberation Day” tariffs in a 6-3 decision. The decision should have saved taxpayers from hundreds of billions of dollars a year in illegal tariffs. Instead, Trump blasted the decision as “deeply disappointing,” said the justices who joined the majority opinion should be “absolutely ashamed,” and immediately issued a proclamation imposing replacement tariffs to address purported BoP problems under Section 122 of the Trade Act of 1974. Section 122 requires the president to impose temporary duties if the government faces “fundamental international payments problems” including serious BoP deficits.

Those tariffs may also be thrown out by the courts. Several states, a spice importer, and a toy company sued to have them overturned. On May 7, in a 2-1 decision, the U.S. Court of International Trade ruled the tariffs were not permissible, largely based on the Administration’s use of “trade deficits” and “current account deficits” as stand-ins for “balance-of-payments deficits.”

Its decision was appealed by the Trump Administration, and the government continues to collect Section 122 duties as the case moves forward. The Justice Department’s brief to the Court of International Trade defending the tariffs included an important point:

Congress intended that any action taken pursuant to Section 122 be consistent with the then-existing GATT (General Agreement on Tariffs and Trade) rules and any future international rules entered into force for the United States.

In other words, for Section 122 tariffs to be legal, they must comply with World Trade Organization (WTO) rules. Those rules include a requirement that countries imposing tariffs enter into consultations with the WTO to discuss the nature of its balance-of-payments problems. On June 22, USTR submitted its brief to the WTO defending Section 122 tariffs. USTR was in the unenviable position of defending tariffs that are indefensible based on current WTO rules.

USTR’s fundamental dilemma: Section 122 tariffs are inconsistent with WTO rules

USTR’s opening statement to the WTO Balance-of-Payments Committee paid lip service to the idea that Section 122 tariffs are consistent with the rules. However, it provided no evidence to back that up. That’s probably because, as a close reading of its statement shows, providing such evidence is impossible.

The USTR submission began by selectively quoting WTO rules: “GATT Article XII:1 provides that a Member may impose import restrictions in order to ‘safeguard its external financial position and its balance of payments.’” USTR left out the subsequent qualifying paragraph:

Import restrictions instituted, maintained or intensified by a contracting party under this Article shall not exceed those necessary: (i) to forestall the imminent threat of, or to stop, a serious decline in its monetary reserves, or (ii) in the case of a contracting party with very low monetary reserves, to achieve a reasonable rate of increase in its reserves. (emphasis added)

This language was intended to provide a safeguard for countries that faced declines in monetary reserves under a fixed-exchange rate regime, which the United States has not had for over 50 years.

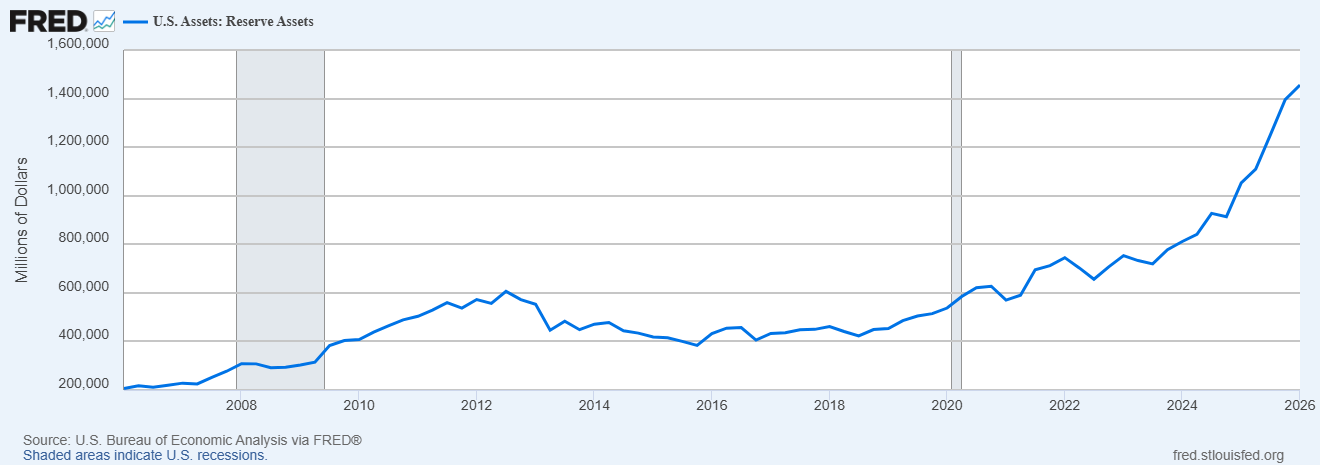

More importantly, U.S. reserve assets are currently at an all-time high of nearly $1.5 trillion.

Figure 1: Balance-of-payments tariffs must address a serious decline in monetary reserves under WTO rules. The Bureau of Economic Analysis reports that U.S. reserve assets have never been higher.

USTR’s submission conceded that, based on WTO rules, it is impossible as a practical matter for the United States to face a drain on our monetary reserves:

[A] serious decline in monetary reserves is not an appropriate measure of a balance-of-payments problem for the United States . . . This is because the U.S. dollar is the world’s reserve currency. As such, any imminent threat of a serious decline in U.S. dollar reserves held by the United States is largely mitigated by the ability of the United States Treasury to print more money.

Since the United States does not face the decline in monetary reserves required to implement Section 122 tariffs under WTO rules, USTR asked the WTO to disregard its rules and use a “proxy” measure provided by the United States that would rubber-stamp tariffs:

Therefore, for the United States, the net international investment position is an appropriate proxy for the reserves language identified in GATT Article XII:2.

As one WTO member pointed out, the United States “appears to be effectively rewriting a key WTO provision.”

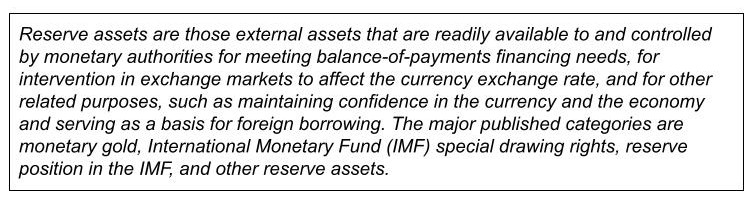

Box 1: The federal government’s own definition of reserve assets conflicts with the proxy definition proposed by USTR.

USTR’s secondary problem: its proposed proxy measure is inconsistent with the Trump Administration’s economic and tariff policies.

USTR cited our negative net international investment position (NIIP) as evidence of a BoP problem.

The NIIP is a measure of all foreign investment in the United States compared to all U.S. investment abroad. When foreign investment increases, or when a U.S. company reshores a factory to the United States, the Bureau of Economic Analysis reports it as an increase in our negative NIIP. And the cornerstone of the Trump Administration’s trade policy is to attract more foreign investment—in other words, to increase the country’s negative NIIP.

The White House website has an entire section, The Trump Effect, that tracks foreign investment. The Commerce Department runs a program, SelectUSA, dedicated to attracting foreign investment. In his July 3 Mount Rushmore speech, Trump himself said “As of last week, $19.2 trillion pouring into the United States right now from all over the world. That’s the investment being made.” That’s also a 90% increase in our negative NIIP.

President Trump appears to understand that we should welcome international investment, not characterize it as a “deterioration” in our investment position as USTR has done.

Section 122 tariffs should expire on July 24 unless Congress extends them. In the meantime, the government will have collected an estimated $35 billion in duties—money that it should be required to refund, with interest, if the CIT decision stands.

As the Department of Justice has stated in its legal briefs, Section 122 tariffs must be consistent with international rules. They are not. The USTR argument to the contrary boils down to this: “It is impossible for there to be a serious decline in U.S. dollar reserves as required to impose tariffs. Therefore, you should ignore the rules and use the proxy rules we are providing.”

Who can blame USTR? We would all like to follow the rules and laws we wish existed instead of the ones that actually exist.