Dear Chair Wyden, Ranking Member Crapo, and Members of the Senate Finance Committee:

On behalf of National Taxpayers Union (NTU), the nation’s oldest taxpayer advocacy organization, I wish to submit a statement for the record for the Committee’s October 20 hearing, “Health Insurance Coverage in America: Current and Future Role of Federal Programs.”[1] NTU strongly believes that lawmakers should narrow their focus and work towards closing health coverage gaps in a manner that favors the lower costs and increased efficiency of private health coverage over federal health programs. Unfortunately, some of the recent proposals from lawmakers that would greatly expand Medicare coverage or enhance Affordable Care Act (ACA) premium subsidies for six-figure households would increase the taxpayer’s burden for subsidizing health coverage in the U.S. without meaningfully reducing coverage gaps.

NTU’s Stake in Health Coverage Policy

Given the nation’s taxpayers heavily subsidize both private and public health coverage, NTU has an important stake in the present and future direction of federal subsidies for health coverage. Some context may help frame our viewpoints and policy recommendations.

According to a Congressional Budget Office (CBO) study released in 2020, federal support for health insurance -- for individuals under 65 alone (i.e., not including the cost of Medicare coverage for individuals 65 and older) -- was projected to total $921 billion in fiscal year (FY) 2021.[2] Nearly half of that support (47 percent, or $433 billion) went to Medicaid and the Children’s Health Insurance Program (CHIP), programs designed to primarily support low-income and disabled individuals. Just under a third of FY 2021 taxpayer support for health coverage (32.9 percent, or $303 billion) went to the tax exclusion employers and employees receive for employer-sponsored health insurance. The remaining 20 percent or so of federal support went to ACA marketplace subsidies (in most cases, premium tax credits (PTCs)) or Medicare coverage for individuals under 65.

Put another way, the federal government currently spends (or foregoes taxation on) nearly $1 trillion supporting the health coverage of individuals under 65. These combined costs are projected to grow nearly 48 percent over the next 10 years -- outpacing expected inflation -- to $1.36 trillion in FY 2030.[3]

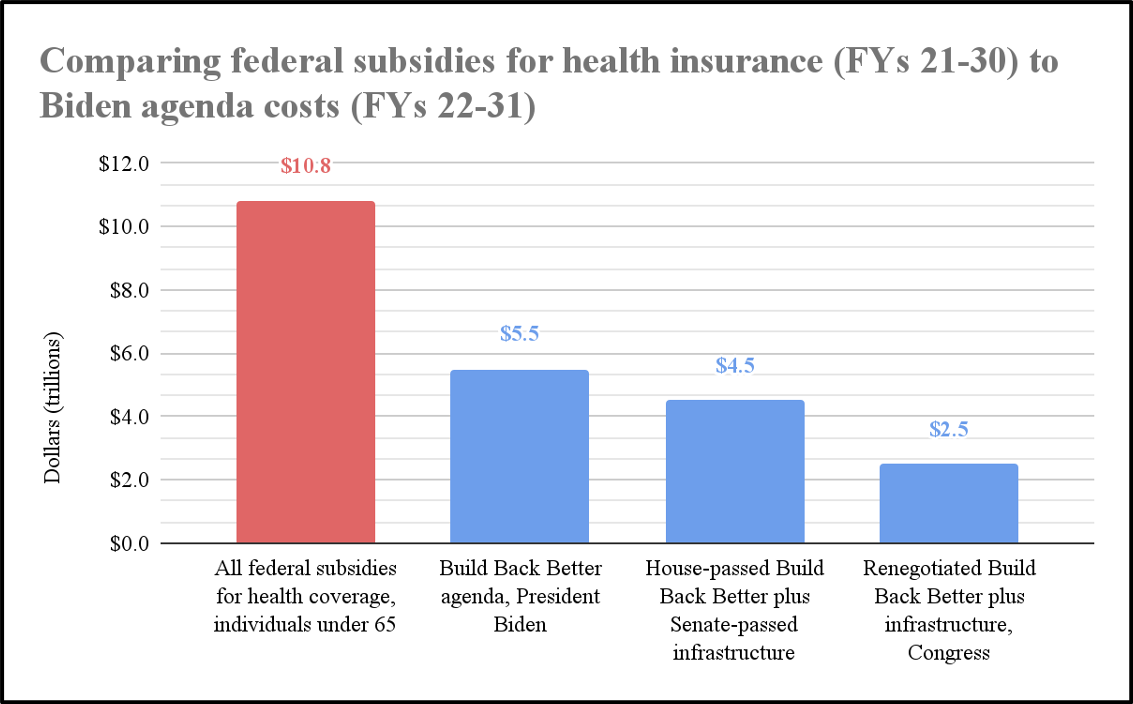

Put yet another way -- framing these costs over 10 years, as lawmakers are doing with their reconciliation and infrastructure plans -- federal spending and subsidies for health coverage for individuals under 65 will total a staggering $10.8 trillion over the decade.[4] This is nearly double the reported cost of President Biden’s original Build Back Better agenda of $5.5 trillion.

Lawmakers’ approaches to closing health coverage gaps and/or subsidizing health coverage can have substantially larger budget implications for taxpayers than the entire reconciliation package being fiercely negotiated in Congress, making the Committee’s hearing an extremely important endeavor.

NTU Principles for Health Coverage Policy

As a taxpayer advocacy organization, NTU urges lawmakers to pursue health coverage policies that adhere to two broad principles: 1) have a narrow focus to closing health coverage gaps that prioritizes low-income individuals who do not have access to subsidized care elsewhere, and 2) pursue the lower costs and increased efficiency of private health coverage over federal health programs.

NTU Concerns With ACA and Medicare Expansion Proposals

Unfortunately, several current reconciliation proposals violate both of these principles while committing taxpayers to hundreds of billions of dollars in additional health coverage subsidies over the next decade.

Premium Tax Credit (PTC) Expansion

NTU has warned for years that ACA premium tax credit (PTCs) expansion is ill-suited to reducing coverage gaps in a cost-effective manner, primarily for three reasons: 1) expansion is expensive (a $212 billion deficit impact over 10 years, according to a 2020 estimate from the Congressional Budget Office);[5] 2) targeting generous PTCs to households making six figures or more is a poor use of limited taxpayer dollars; and 3) PTCs are not designed to bend the cost curve for private health coverage, and will only increase in cost as premium hikes outpace wage increases.[6]

We have also demonstrated how, under House Democrats’ PTC expansion plan, an upper-middle class family of four that sees their income steadily rise from $125,000 per year to $250,000 per year over a 15-year period, earning $2.7 million over that time (or about $180,000 per year on average), could receive nearly $60,000 in PTCs under the reconciliation expansion plan.[7] This would be an extraordinary misallocation of taxpayer dollars, supporting the premium costs of an affluent household that likely does not need taxpayer-funded assistance. While a substantial portion of PTC dollars may still go to low-income families in the form of refundable credits, we are seeing some early evidence that a concerning proportion of PTC recipients under the temporary, American Rescue Plan expansion of PTCs are making above 400 percent of the federal poverty level (FPL) -- over seven percent (or 150,000) of 2.1 million HealthCare.gov enrollees from February through August 2021.[8]

We would add that several design features of the PTC expansion increase taxpayer subsidies of health coverage but may not meaningfully reduce health coverage gaps, including but not limited to: 1) increasing the value of PTCs for existing beneficiaries by reducing the proportion of income that households are expected to contribute to insurance premiums, including for individuals making above 400 percent of the FPL, 2) allowing individuals to access PTCs regardless of income level, 3) allowing individuals who received any unemployment benefits in a year to access PTCs as if they made only 150 percent of the FPL, and 4) limiting recapture of excess PTCs regardless of income. Given the Joint Committee on Taxation (JCT) estimated that these provisions for 2020-2022 alone would have a $45.6 billion budget impact,[9] it is conceivable that lawmakers seeking to make these policies permanent could spend tens of billions of dollars over a decade subsidizing care for individuals who already have or otherwise would have coverage.

Medicare Benefit Expansion

Depending on how lawmakers structure the timing of expanding Medicare to dental, vision, and hearing benefits, and depending on how universal lawmakers make the benefits, the 10-year costs of Medicare benefit expansion may run up to $350 billion.[10] This potentially significant commitment of taxpayer dollars would not provide comprehensive health insurance to a single individual in the country, but instead would provide ancillary benefits to tens of millions of seniors, many of who already have dental, vision, and hearing coverage through Medicare Advantage.

The reconciliation proposal would provide universal dental, vision, and hearing coverage under Medicare Part B, but over 90 percent of Medicare Advantage enrollees are in plans that offer some access to dental, vision, and hearing coverage.[11] What’s more, of all Medicare beneficiaries (in traditional Medicare and Medicare Advantage) the median cost in 2018 for hearing care was $60, for dental care was $244, and for vision care was $130.[12] While we would not dispute that dental, vision, and hearing care is health care, and while we would not dispute the plain evidence that some seniors are in need of dental, vision, or hearing care and struggle to afford it, the reconciliation proposal misfires in providing a universal, taxpayer-funded benefit to millions of beneficiaries who already have coverage for such services.

Together, the ACA and Medicare expansion proposals envisioned by House Democrats could cost $553 billion, according to a recent CBO estimate.[13] While not every dollar therein would go to beneficiaries who have access to coverage and care already, the above evidence suggests that hundreds of billions of dollars at minimum would not meaningfully reduce the coverage gap.

Lawmakers Should Focus Coverage Gap Efforts Narrowly

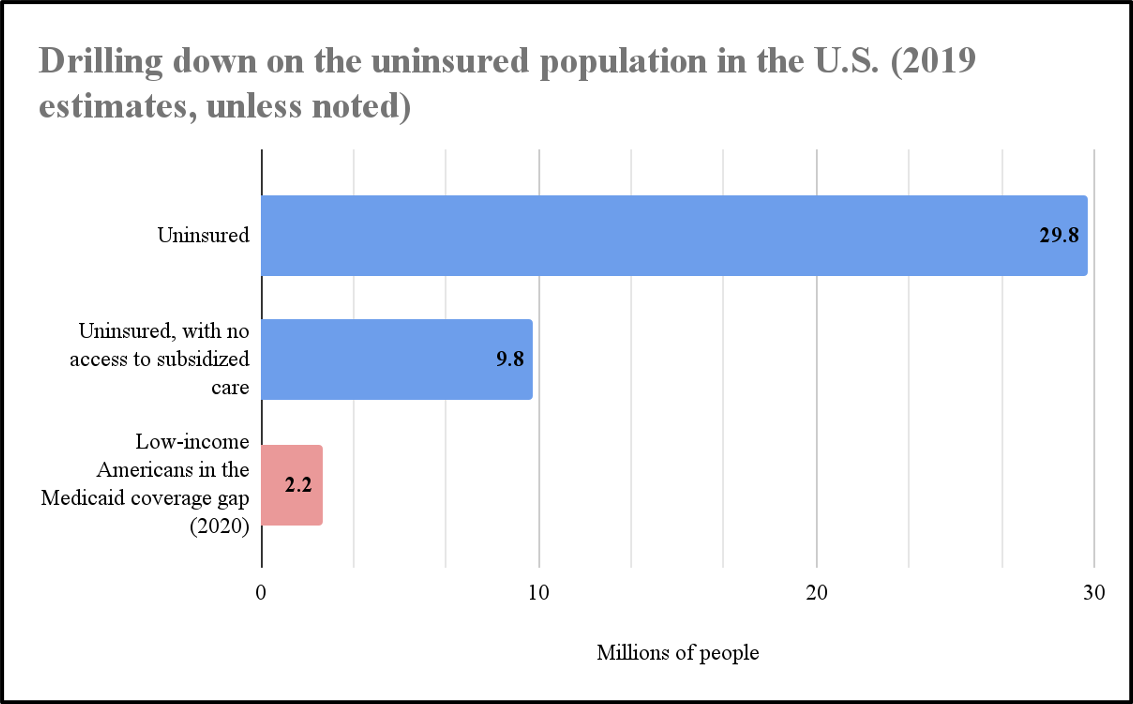

While numerous headlines and reports focus on the fact that nearly 30 million people in the U.S. are uninsured, few reports we have reviewed provide a narrower focus on what proportion of that uninsured population both a) cannot afford any type of comprehensive health coverage and b) cannot access any subsidized health coverage under current law and policy.

CBO’s 2020 report, “Who Went Without Health Insurance in 2019, and Why?” is instructive.[14]

Of 29.8 million Americans uninsured in 2019, two-thirds (20 million total) were eligible for subsidized coverage, either through Medicaid, CHIP, employment-based coverage, or ACA marketplace subsidies.[15]

Of the remaining 9.8 million Americans, who were uninsured in 2019 and could not access subsidized coverage, around 40 percent (four million) were not lawfully present in the U.S. NTU does not weigh in on immigration matters, so we focus our analysis here on the remaining 5.8 million Americans: those who are not covered by Medicaid but would be if their state expanded Medicaid under the ACA (3.2 million) and those who have income that is too high to receive ACA subsidies and also do not have access to employer-sponsored care.

More recent estimates of the Medicaid coverage gap are closer to 2.2 million than 3.2 million,[16] meaning that this is the population lawmakers should be focusing on with new initiatives to close the coverage gap. There is a major difference between attempting to provide coverage to 30 million Americans (one in nine Americans) and 2.2 million Americans (less than one in 100 Americans). And a far narrower problem calls for far narrower solutions.

Lawmakers Should Focus on Cost-Effective Private Sector Solutions to Closing Coverage Gap

Some lawmakers are considering a federal Medicaid expansion proposal that would cost up to $323 billion over a decade to close the 2.2 million-person coverage gap noted above.[17] Unfortunately, substantial research indicates that the subsidy cost per person for public health coverage is much higher than private health coverage, and that public health programs are subject to high improper payment rates that put taxpayer dollars at risk. Policymakers may see fewer taxpayer dollars do more to reduce the coverage gap by helping low-income Americans obtain more cost-effective private health coverage instead.

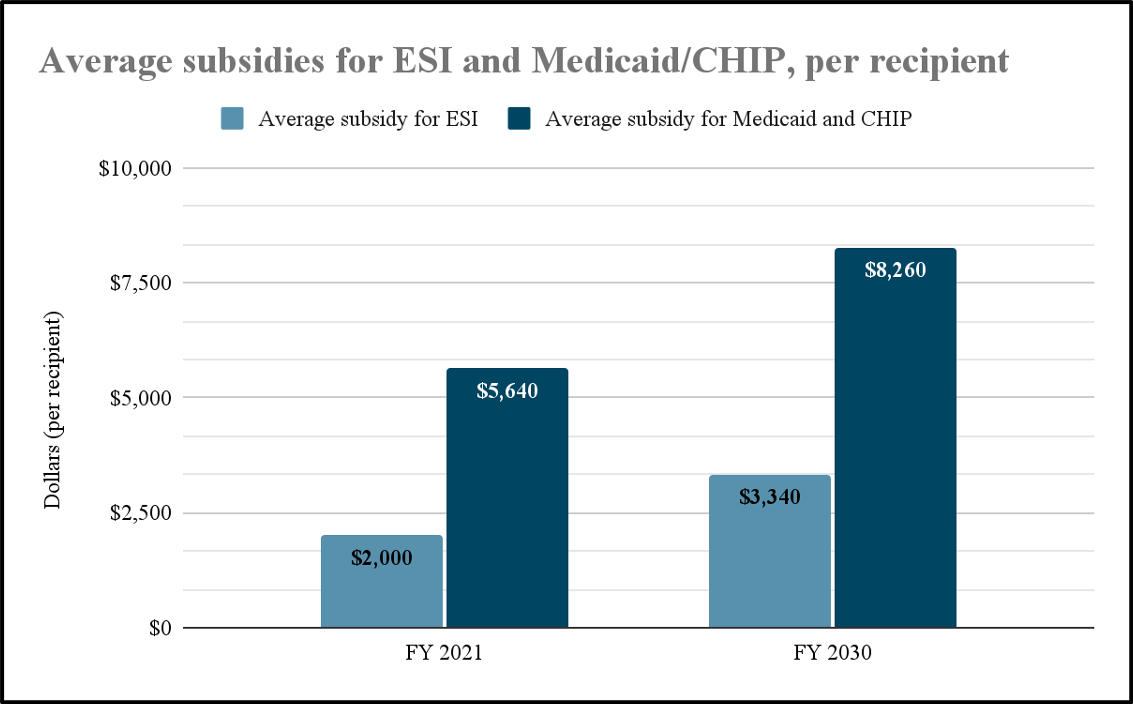

The average subsidy per recipient of employer-provided coverage (ESI) was $2,000 in FY 2021, according to CBO.[18] Compare this to $5,640 per recipient under Medicaid and CHIP. CBO projects that gap will narrow over the next decade, but Medicaid and CHIP subsidies will still more than double the average subsidy for ESI.

In other words, ESI subsidies are far more cost-effective on a per-recipient basis than Medicaid and CHIP. While the difference may be explained by a number of factors, one worth considering is the extraordinarily high improper payment rate in Medicaid.[19]

According to 2020 data from the Centers for Medicare and Medicaid Services (CMS), Medicaid comprised nearly two-thirds of all CMS improper payments in Medicare and Medicaid in 2020, $86.5 billion out of $134.2 billion.[20] The Medicaid improper payment rate of 21.36 percent was 18.6 times higher than improper payments in Medicare Part D and 3.1 times higher than improper payments in Medicare Advantage, two subsidized health coverage programs that rely primarily on private insurers.

And as health experts like the Galen Institute’s Brian Blase have pointed out, access to care (and not just coverage) in Medicaid raises concerns for proponents of the program. As Blase wrote in 2020:

“Coverage is not the same thing as care. A 2019 study by the Medicaid and CHIP Payment and Access Commission, a congressional advisory group, found that one-third of primary care physicians and nearly two-thirds of psychiatrists do not accept Medicaid patients. Doctors cite difficult Medicaid paperwork, administrative burdens, and poor reimbursement rates as reasons they do not accept more patients on the program.”[21]

That said, closing the coverage gap is a laudable goal both on public health grounds and fiscal grounds, if the problem and the solutions are properly defined. Estimates for the cost of uncompensated or charity care (the latter a subset of uncompensated care payments) vary, but range from anywhere between $14 billion for nonprofit hospitals’ charity care (2017 estimate)[22] to $41.6 billion for all hospitals’ uncompensated care (2020).[23] CBO has found that “it is likely that being uninsured results in worse health outcomes, at least for some people.”[24] In short, there are societal and taxpayer costs to millions of Americans wanting access to affordable health coverage with no subsidized options available to them.

However, the evidence is clear that the private sector will have more cost-effective solutions to reducing the coverage gap. Two avenues where lawmakers should explore reforms and, possibly, support for low-income Americans are 1) employer-provided care and 2) consumer-directed health savings accounts (HSAs).

As noted above, taxpayer support for employer-sponsored insurance (ESI) is far lower than subsidies for public health coverage. That said, the tax exclusion for ESI is far from perfect. Some evidence demonstrates the exclusion puts upward pressure on health insurance premiums, at the expense of higher wages, and it is worth noting that 37 percent of the tax benefit in 2018 went to households making 600 percent or more of the FPL.[25]

Lawmakers could explore reforms to the ESI exclusion that more narrowly target the benefit at taxpayers who need support and/or incentivize businesses that currently do not offer ESI to low-wage or low-income employees and contractors to do so.

HSAs are another promising and cost-effective route for lawmakers. JCT estimated the costs of HSA tax subsidies for FYs 2020 through 2024 to total $66 billion, an average of $13.2 billion per year.[26] If the average number of Americans contributing to an HSA hovers between 10 million and 12 million people per year,[27] then the tax expenditure cost per person is between just $1,100 and $1,320 per person. NTU has outlined numerous ways that lawmakers can expand both access to HSAs and the list of health expenses HSAs can cover.[28]

Conclusion

In short, NTU appreciates that lawmakers are attempting to reduce health coverage gaps, and we acknowledge that closing health coverage gaps could bring benefits to society and to federal taxpayers. That said, Congress should take care to narrowly define both the uninsured problem that federal policies can fix and the big-picture solutions that lawmakers should pursue to help people that truly need taxpayer-funded assistance. Furthermore, those big-picture solutions should focus on the cost effectiveness of private health coverage, rather than public programs that come with significant cost, access, and improper payment concerns. NTU is pleased to work with Committee members on policies that adhere to these principles. Should you have any questions, I am at your service.

Sincerely,

Andrew Lautz, Director of Federal Policy

CC: Members of the Senate Committee on Finance

[1] Senate Committee on Finance. “Health Insurance Coverage in America: Current and Future Role of Federal Programs.” October 2021. Retrieved from: https://www.finance.senate.gov/hearings/health-insurance-coverage-in-america-current-and-future-role-of-federal-programs (Accessed October 19, 2021.)

[2] Congressional Budget Office (CBO). “Federal Subsidies for Health Insurance Coverage for People Under 65: 2020 to 2030.” September 2020. Retrieved from: https://www.cbo.gov/system/files/2020-09/56571-federal-health-subsidies.pdf (Accessed October 19, 2021.)

[3] Ibid.

[4] Ibid.

[5] CBO. “Estimated Effect on the Deficit of Rules Committee Print 116-56, the Patient Protection and Affordable Care Enhancement Act.” June 24, 2020. Retrieved from: https://www.cbo.gov/system/files/2020-06/Patient_Protection_and_Affordable_Care_Enhancement_Act_0.pdf (Accessed October 19, 2021.)

[6] Lautz, Andrew. “What's the Deal With Premium Tax Credits?” National Taxpayers Union, September 23, 2021. Retrieved from: https://www.ntu.org/publications/detail/whats-the-deal-with-premium-tax-credits

[7] Ibid.

[8] Department of Health and Human Services. “2021 Final Marketplace Special Enrollment Period Report.” September 2021. Retrieved from: https://www.hhs.gov/sites/default/files/2021-sep-final-enrollment-report.pdf (Accessed October 19, 2021.)

[9] Joint Committee on Taxation. “Estimated Revenue Effects Of H.R. 1319, The “American Rescue Plan Act Of 2021,” As Amended By The Senate, Scheduled For Consideration By The House Of Representatives.” March 9, 2021. Retrieved from: https://www.jct.gov/publications/2021/jcx-14-21/ (Accessed October 19, 2021.)

[10] CBO. “H.R. 3, The Elijah E. Cummings Lower Drug Costs Now Act.” December 10, 2019. Retrieved from: https://www.cbo.gov/system/files/2019-12/hr3_complete.pdf#page=10 (Accessed October 19, 2021.)

[11] Freed, Meredith; Cubanski, Juliette; Sroczynski, Nolan; Ochieng, Nancy; and Neuman, Tricia. “Dental, Hearing, and Vision Costs and Coverage Among Medicare Beneficiaries in Traditional Medicare and Medicare Advantage.” Kaiser Family Foundation, September 21, 2021. Retrieved from: https://www.kff.org/health-costs/issue-brief/dental-hearing-and-vision-costs-and-coverage-among-medicare-beneficiaries-in-traditional-medicare-and-medicare-advantage/ (Accessed October 19, 2021.)

[12] Ibid.

[13] CBO. “Re: Provisions in Reconciliation Legislation That Would Affect Health Insurance Coverage of People Under Age 65.” October 19, 2021. Retrieved from: https://energycommerce.house.gov/sites/democrats.energycommerce.house.gov/files/documents/Letter_Honorable_Jason_Smith.pdf (Accessed October 19, 2021.)

[14] For more, see: CBO. “Who Went Without Health Insurance in 2019, and Why?” September 2020. Retrieved from: https://www.cbo.gov/system/files/2020-09/56504-Health-Insurance.pdf (Accessed October 19, 2021.)

[15] Statistics in this section are sourced from CBO’s report, unless otherwise noted.

[16] Garfield, Rachel; Orgera, Kendal; and Damico, Anthony. “The Coverage Gap: Uninsured Poor Adults in States that Do Not Expand Medicaid.” Kaiser Family Foundation, January 21, 2021. Retrieved from: https://www.kff.org/medicaid/issue-brief/the-coverage-gap-uninsured-poor-adults-in-states-that-do-not-expand-medicaid/ (Accessed October 19, 2021.)

[17] CBO. “Re: Provisions in Reconciliation Legislation That Would Affect Health Insurance Coverage of People Under Age 65.” October 19, 2021. Retrieved from: https://energycommerce.house.gov/sites/democrats.energycommerce.house.gov/files/documents/Letter_Honorable_Jason_Smith.pdf (Accessed October 19, 2021.)

[18] Congressional Budget Office (CBO). “Federal Subsidies for Health Insurance Coverage for People Under 65: 2020 to 2030.” September 2020. Retrieved from: https://www.cbo.gov/system/files/2020-09/56571-federal-health-subsidies.pdf (Accessed October 19, 2021.)

[19] Improper payments are evidence that fraud or misuse of funds may exist, but are not completely indicative of fraudulent payments or other misdeeds. As CMS writes: “improper payments are payments that did not meet statutory, regulatory, administrative, or other legally applicable requirements and may be overpayments or underpayments.” For more, see: CMS. “2020 Estimated Improper Payment Rates for Centers for Medicare & Medicaid Services (CMS) Programs.” November 16, 2020. Retrieved from: https://www.cms.gov/newsroom/fact-sheets/2020-estimated-improper-payment-rates-centers-medicare-medicaid-services-cms-programs#_ftn1 (Accessed October 19, 2021.)

[20] Ibid.

[21] Blase; Brian; Adolphsen, Sam; and Turner, Grace-Marie. “Why states should not expand Medicaid.” Galen Institute, October 6, 2020. Retrieved from: https://galen.org/assets/Reasons-Not-to-Expand-Medicaid-100620.pdf (Accessed October 19, 2021.)

[22] Bai, Ge; Yehia, Farah; and Anderson, Gerard F. “Charity Care Provision by US Nonprofit Hospitals.” JAMA Internal Medicine, February 17, 2020. Retrieved from: https://jamanetwork.com/journals/jamainternalmedicine/fullarticle/2760774 (Accessed October 19, 2021.)

[23] American Hospital Association. “Fact Sheet: Uncompensated Hospital Care Cost.” January 2021. Retrieved from: https://www.aha.org/fact-sheets/2020-01-06-fact-sheet-uncompensated-hospital-care-cost (Accessed October 19, 2021.)

[24] CBO. “Who Went Without Health Insurance in 2019, and Why?” September 2020. Retrieved from: https://www.cbo.gov/system/files/2020-09/56504-Health-Insurance.pdf (Accessed October 19, 2021.)

[25] Congressional Research Service. “Tax Expenditures: Compendium of Background Material on Individual Provisions.” December 2020. Retrieved from: https://www.govinfo.gov/content/pkg/CPRT-116SPRT42597/pdf/CPRT-116SPRT42597.pdf#page=901 (Accessed October 19, 2021.)

[26] Ibid.

[27] Ibid.

[28] Lautz, Andrew. “Ideas to Expand and Promote the Use of Health Savings Accounts: An Alternative to Government-Run Health Insurance.” National Taxpayers Union, October 21, 2019. Retrieved from: https://www.ntu.org/publications/detail/ideas-to-expand-and-promote-the-use-of-health-savings-accounts-an-alternative-to-government-run-health-insurance