(pdf)

What Is the Premium Tax Credit?

The premium tax credit (PTC) is a refundable tax credit, which in most years is available to households making between 100% and 400% of the federal poverty level (FPL) who do not have access to affordable coverage through work, Medicare, or Medicaid, and who purchase health insurance on either HealthCare.gov or the state exchanges set up under the Affordable Care Act

The premium tax credit (PTC) is a refundable tax credit, which in most years is available to households making between 100% and 400% of the federal poverty level (FPL) who do not have access to affordable coverage through work, Medicare, or Medicaid, and who purchase health insurance on either HealthCare.gov or the state exchanges set up under the Affordable Care Act- For purposes of coverage through work, coverage is determined to be “affordable” if the employee contribution is less than 9.5 percent of household income; Democrats want to make this 8.5 percent in reconciliation

- The American Rescue Plan Act (ARPA) expanded PTCs to any household making 100% or more of the FPL

- Democrats want to make this expansion permanent in reconciliation

- ARPA also allowed anyone who received unemployment insurance (UI) benefits in 2021 to access PTCs that could cover the full premium costs of a health insurance plan purchased on the exchanges

- Democrats want to extend this provision through 2025

- Democrats also want to extend PTCs to individuals making between 0% and 100% of the FPL from 2022 through 2024, regardless of whether or not they have access to an affordable plan through work

- Lawmakers see this as a bridge to a federally-run Medicaid program that covers adults making between 0% and 138% of the FPL (i.e., Medicaid expansion populations) in states that have not expanded Medicaid

- This provision would effectively eliminate the income test for PTCs, at least for three years

How Much is the PTC Worth?

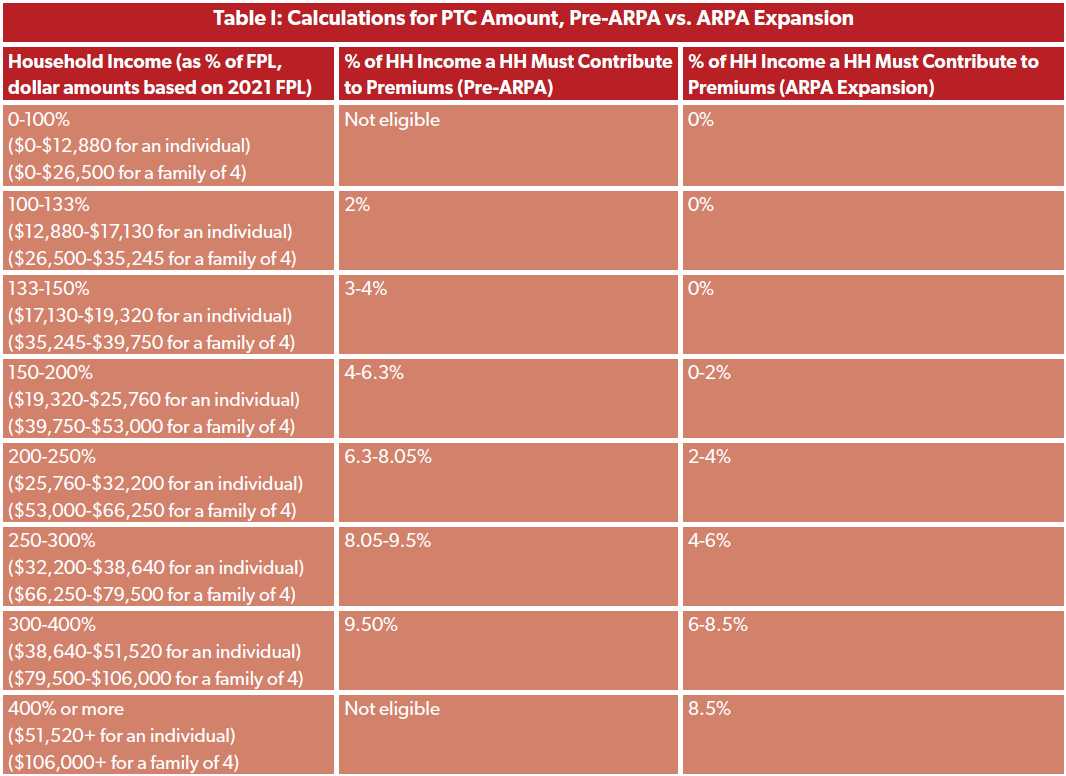

- The PTC is refundable (meaning credits can exceed the amount of taxes a taxpayer or household owes in a given year) and advanceable on a monthly basis; the amount depends on household income, the plan selected, and premium rates

- The following table demonstrates what percentage of income certain households are expected to contribute to premiums, both under pre-ARPA law and under the temporary ARPA expansion in 2021 and 2022 (which Democrats want to make permanent); the difference between premium amounts for the second lowest-cost silver plan and the household contribution is covered as a PTC:

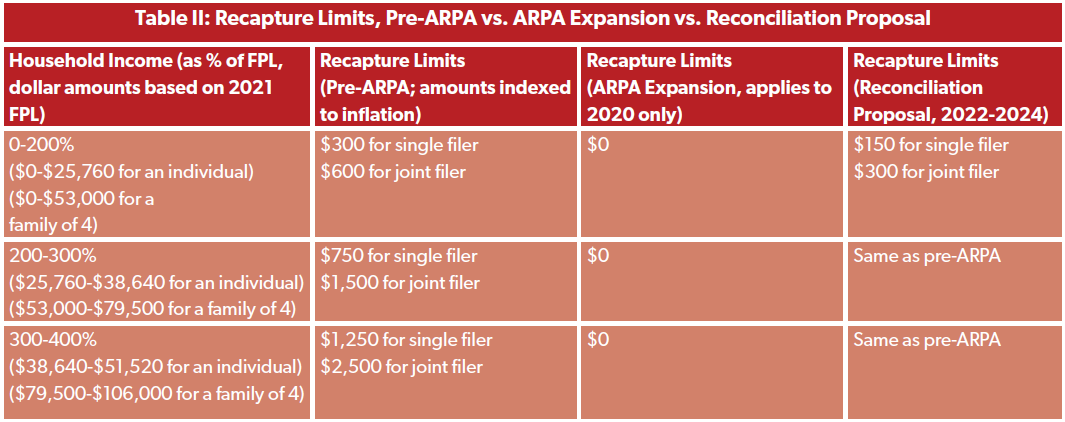

- Since the PTC is refundable and advanceable, and since the IRS bases estimated PTC amounts on prior-year income, the agency has the authority to recapture overpayments, subject to certain limits

- Here are those limits 1) before ARPA, 2) under temporary ARPA rules, and 3) under proposed reconciliation legislation:

- IRS data indicate that overpayment of PTCs may be a serious problem; according to CRS review of IRS data, around 3.2 million households received advance payments that were more than they were eligible for in 2018. These taxpayers paid back approximately $4.4 billion of these overpayments

- By comparison, just 2.3 million households received advance payments that were less than they were eligible for in 2018

How Many People Receive PTCs?

- According to Kaiser Family Foundation (KFF) data, in 2020 9.1 million Americans received a total of $53.7 billion in PTCs

- That’s an average subsidy of about $5,900 per enrollee (or about $491 per month)

- The average subsidy significantly differed by state, with a range of as low as $3,216 per enrollee ($268 per month) in Massachusetts to $10,968 per enrollee (or $914 per month) in Wyoming

- Just four states comprised nearly half of PTC dollars in 2020:

- Florida: $10.9 billion for 1.7 million enrollees ($6,371 per enrollee)

- California: $6.9 billion for 1.3 million enrollees ($5,435 per enrollee)

- Pennsylvania: $5.2 billion for 0.9 million enrollees ($6,186 per enrollee)

- North Carolina: $3.1 billion for 0.4 million enrollees ($7,285 per enrollee)

- According to recent HHS data, roughly 2.8 million Americans newly signed up for ACA coverage during the 2021 special enrollment period (Feb. 15 - Aug. 15) alone

- 2.1 million signed up on HealthCare.gov and more than 730,000 signed up on state-based exchanges

- Because of generous new subsidies, more than 1.2 million of these new sign ups are paying less than $10 per month in premiums (i.e., less than $120 per year)

- Around 150,000 new enrollees on HealthCare.gov had incomes north of 400% of the FPL

What Does the PTC Cost the Federal Government?

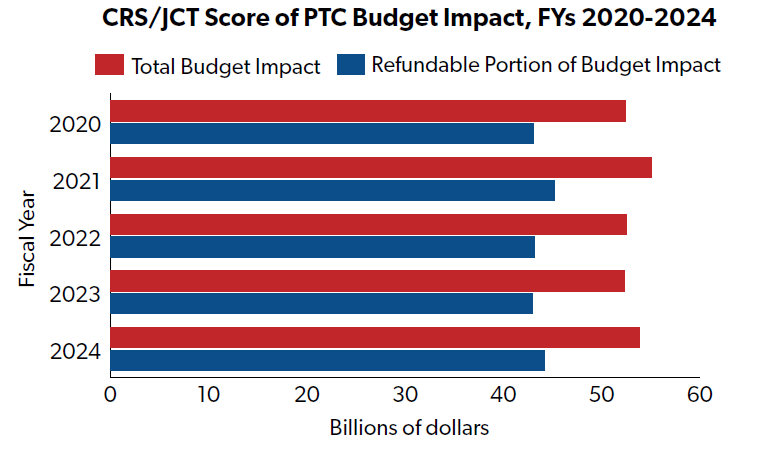

- According to CRS, the pre-ARPA version of PTCs were projected to cost the federal government between $52 billion and $55 billion per year from FYs 2020 through 2024

- The graph below demonstrates the fiscal impact, with a second set of bars demonstrating the portion of total spending that is on refundable PTCs:

- JCT estimated that three ARPA provisions -- 1) expanding PTCs from 2021-2022, 2) no excess PTC recapture in 2020, and 3) allowing UI recipients in 2021 to receive a more generous PTC in 2021 regardless of income -- would have a budget impact of $45.6 billion

- Almost three-quarters of the budget impact ($34.8 billion out of $45.6 billion) comes from the more generous PTCs

- An additional 14 percent ($6.3 billion) comes from no recapture

- The remaining 13 percent ($4.5 billion) comes from UI provisions

What Are NTU’s Arguments Against PTC Expansion Proposals?

- NTU has identified three major problems with permanent expansion of PTCs, as envisioned by Congressional Democrats for years:

- Expansion is expensive (a $212 billion deficit impact over 10 years, according to a 2020 estimate from the Congressional Budget Office);

- Targeting generous PTCs to households making six figures or more is a poor use of limited taxpayer dollars; and

- PTCs are not designed to bend the cost curve for private health coverage, and will only increase in cost as premium hikes outpace wage increases

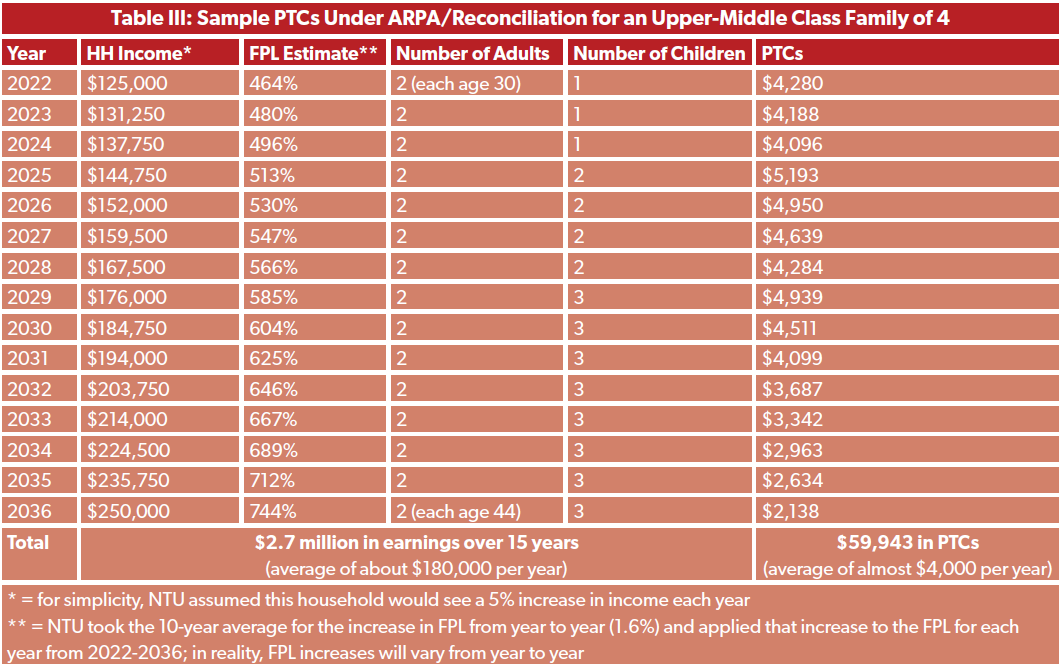

- To demonstrate how PTCs can waste limited taxpayer dollars on subsidies for households that do not need the assistance, we’ll walk you through the potential PTCs an upper-middle class household could receive over 15 years

- This sample household includes two 30-year-old adults earning a combined $125,000 in 2022, which should just about put them in the top quarter of income-earning households in the nation; they have one new child

- The household sees 5% income increases each year from 2022-2036, rising to $250,000 in income in 2036; they have two more children over those 15 years

- Based on estimates from KFF’s marketplace calculator, this household would earn $2.7 million over 15 years (average of about $180,000 per year) and would receive nearly $60,000 in taxpayer-funded PTCs during that time (an average of about $4,000 per year)

Where Can I Find Additional Resources?