(pdf)

In early April, the Department of Labor reported that nearly 10 million Americans filed claims for unemployment insurance (UI) between March 15 and March 28. The Federal Reserve Bank of St. Louis estimated prior to the passage of the Phase 3 relief package that 47 million people may be laid off between now and the end of June, driven by the COVID-19 (coronavirus) pandemic that has shut down much of the American economy.

While the Phase 3 relief package passed by Congress included a generous, federally funded, temporary increase in weekly UI benefits, lawmakers left one major question unanswered: how do policymakers best assist the millions of people who may lose employer-sponsored health insurance (ESI) during this economic and public health crisis?

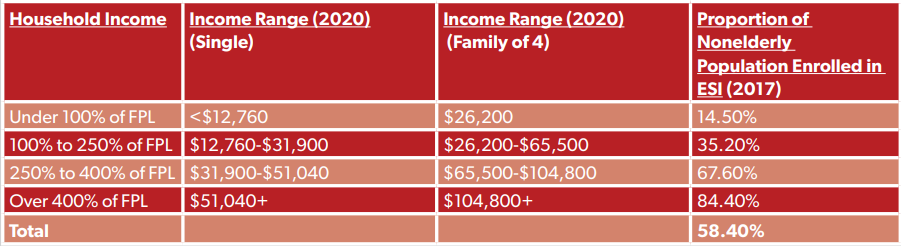

Though we cannot know exactly how many people will lose access to ESI in the coming months, a rough estimate of millions is not out of the question. According to the Kaiser Family Foundation (KFF), 58.4 percent of the nonelderly population was enrolled in ESI in 2017. People in households making between 250 and 400 percent of the federal poverty line (FPL) ($31,900 to $51,040 per year for individuals, $65,500 to $104,800 for a family of four) were more likely to be enrolled in ESI than those in households making between 100 and 250 percent of FPL, and those in households making 100 percent of FPL or less (67.6 percent vs. 35.2 percent vs. 14.5 percent, respectively).

Health Management Associates (HMA), a health care consulting firm, just projected that between 12 million and 35 million people will lose access to ESI during this crisis (that includes both displaced workers and their family members who were covered by ESI).

If there is a silver lining for these workers and their families, it is that HMA projects a vast majority will find low- or no-cost coverage through Medicaid (between 10.6 million and 23.0 million, according to their projections). This will put a significant strain on federal and state taxpayers, but this projection leaves 1.1 million to 12.0 million people who will either need to turn to the ACA marketplace or will be uninsured as a result of losing their ESI.

Pandemic Health Accounts: Better for Families and Taxpayers

We propose creating for every household that loses access to ESI - and does not have access an adequate insurance option - a Pandemic Health Account (PHA).

These accounts, which share many similarities with Health Savings Accounts (HSAs), would serve as a bridge between a household’s loss of ESI and the start of their next job with ESI benefits. For that reason, we propose a federal credit designed to help a displaced worker (and, if applicable, their family) afford and choose the health insurance option that best suits their own needs. This credit could be applied to COBRA premiums, an ACA marketplace plan, or a short-term limited duration (STLDI) plan for around four months. Congress may elect to extend that benefit, depending on the duration of the economic crisis. (Lawmakers did the same for the 2009 COBRA subsidy; more on that below.)

COBRA would usually be the most expensive choice for a displaced worker, with ACA marketplace plans being less expensive than COBRA and STLDI plans being less expensive than ACA plans. Because COBRA is the most expensive option, we peg the generosity of the benefit to a share of the average ESI premium for individuals and families. Since the average ESI plan for individuals covers 83 percent of the premium, and the average ESI plan for families covers 71 percent of the premium, we propose that the PHA amount aim to cover 75 percent of the average cost of an ESI plan for an individual or a family, pro-rated to four months.

Therefore, we propose a PHA benefit amount of roughly $2,000 for individuals and $6,000 for joint or family accounts. (This comes out to $500 per month for individuals and $1,500 per month for families.)

We estimate a wide range of potential costs for these PHAs, based on two primary factors: 1) how many people are eligible for and receive PHAs, and 2) what portion of the PHAs are for individuals and what portion are for families. On the low end, if one million individuals were to receive the $2,000 benefit, it would cost taxpayers $2 billion. On the high end, if 12 million families were to receive the $6,000 benefit, it would cost taxpayers $72 billion.

These accounts would differ from HSAs in a few important ways:

PHA holders would not have to be in a high-deductible health plan (HDHP), a requirement for HSA holders;

PHA holders would be able to use their account dollars on premiums (mirroring the permissions in place for HSA holders, who can use their accounts for COBRA premiums or premiums paid while receiving UI benefits);

PHA holders would be subject to the same annual contribution limits as HSA holders (in 2020, $3,550 per year for individual accounts and $7,100 for joint accounts), but the federal government’s contributions to their PHA would not count against their annual contribution limit;

PHA holders would not be able to use funds for non-medical expenses after age 65 (HSA holders can use their remaining funds for non-medical purposes once they reach age 65 and join Medicare).

Some lawmakers have instead proposed a COBRA subsidy, similar to what Congress enacted during the Great Recession in 2009. A House Democratic proposal would subsidize 100 percent of COBRA premiums, compared to a 65-percent subsidy enacted in 2009. While directly subsidizing COBRA premiums would make the program much more affordable for many, this option would be expensive and would limit health care choices for displaced workers.

We also expect various policymakers to propose 1) incentives for states to expand Medicaid, 2) permanent expansion of the Affordable Care Act, and 3) temporary or permanent expansion of the Medicare and Medicaid programs. We think that the PHA option is a better path forward for lawmakers, because the benefits are more targeted, less permanent, more stable for taxpayers, and offer more flexibility to displaced workers:

Predictable expenditures for taxpayers: rather than permanently expanding an existing program (i.e. Medicaid or the ACA’s PTCs), which taxpayers would have to cover long after the pandemic is over, the PHA option could be a defined, predictable benefit from the federal government (much like the $1,200 direct payments or the $600 per week UI increases in Phase 3) that is meant to support displaced workers during this economic crisis;

Flexible options for displaced workers: PHA dollars could be used for most types of medical expenses. PHAs would allow account holders to opt in to COBRA coverage, purchase a plan on the ACA exchanges, purchase an STLDI plan, and/or subsidize their insurance premium costs while saving some PHA dollars for deductibles, out-of-pocket expenses, OTC medications, and more;

Long-term savings opportunities for Americans: While NTU has warned against creating permanent, expensive changes to public programs in response to COVID-19, setting up a PHA for millions of Americans and giving them a head start on savings may encourage them to continue to save once they are back on their feet.

We acknowledge that not all policymakers will agree with the PHA model, given it mirrors some features of HSAs; indeed, many Democrats and progressives are less than enthusiastic about HSA expansion. However, the PHA option presented here could not only help millions of Americans maintain health coverage during the COVID-19 crisis, it could help shore up the ACA marketplaces with new customers.

We discuss some implementation questions and considerations for the PHA option below, and we also review both the universe of existing options and why some of the other, existing proposals to help the newly uninsured fall short.

The PHA Option: Design and Cost Considerations

While NTU does not recommend introducing a taxpayer-funded benefit lightly, given our long track record of advocating for fiscal responsibility, we have made clear that these unique public policy challenges will result in some level of new federal spending.

Policymakers can design the PHA benefit to be temporary, limited, and predictable, depending on the answers to some of the following questions:

Who’s eligible? We believe the PHA option should be limited to workers who have lost access to their ESI and do not have access to a spouse’s plan, a parent’s plan (if under age 26), Medicare, or Medicaid, although policymakers could opt to expand eligibility. However, there are many eligibility questions that may arise if Congress were to design a plan like ours. Should furloughed workers, or workers that have their hours reduced, but that retain access to ESI, have access to some part of the benefit? This would help them meet out-of-pocket costs as they see less money coming through the door.

What about workers who already have HSAs? Millions of Americans already have HSAs, and no doubt a portion of workers who lose access to ESI will have an existing HSA. We believe it makes the most sense for the government to deliver the PHA credit directly to those workers’ existing HSAs, rather than go through the process of setting up a new account.

Should there be an income phaseout? In an effort to make the PHA option more fiscally responsible, we believe the benefit should start to phase out at certain income levels (for individual and joint filers) so that relief is focused on those who need it most. Congress has a few options if designing an income phaseout. They could emulate the recent phaseout for Phase 3’s direct payments, which began at $75,000 for individuals and $150,000 for joint filers (and phased out completely at $99,000/$198,000). Congress could also model the phaseouts like the IRS does for ACA PTCs, at a certain percentage of the federal poverty line (FPL).

We acknowledge policymakers may disagree with some of these design suggestions, but if there is interest in this option - one that is more predictable for taxpayers and offers a more flexible benefit to displaced workers - we stand ready to assist with the particular details.

Implementation Concerns and the Need for Immediate Relief

One legitimate concern with the PHA option is the need to immediately bridge coverage gaps for recently displaced workers. Most will lose their ESI at the end of the same month they are laid off, meaning that many workers laid off in March have lost their ESI as of April 1. With the Department of Treasury and the Small Business Administration facing implementation challenges when it comes to business loan programs, and the Internal Revenue Service taking anywhere from several weeks to several months to issue direct payments to taxpayers, one legitimate question in response to the PHA option is how long it would take to stand up PHAs for millions of displaced workers.

Congress has a few options to smooth the implementation of PHAs. We consider the tradeoffs for these options below:

Conduct the PHA application and setup processes through existing HSA providers: Congress could outsource some of the eligibility determinations and application processing to the health insurers, banks, and financial institutions that already manage HSAs for millions of Americans. Rather than demand that the Treasury Department or Health and Human Services Department get to work immediately verifying that millions of Americans are eligible for the PHA option, the Departments could create a standardized process for dozens or hundreds of insurance companies and banks to do so. Lawmakers would need to include some oversight requirements to protect against fraud and abuse committed by either applicants who are not actually PHA-eligible or private entities seeking the PHA cash for applicants who are not eligible.

Include a safe harbor for premium payments from displaced workers: If it will take federal agencies several weeks or months to deliver cash to these new PHAs, displaced workers should receive a grace period if they can’t afford to pay premiums between their election of COBRA or an ACA plan and the delivery of PHA cash. Lawmakers could consider allowing displaced workers to defer premium payments for some period of time, say 60 or 90 or 120 days, to give federal agencies the breathing room to set up the PHAs. Of course, this could create cash flow problems for health insurers. This could be mitigated by having insurers verify a new enrollee’s PHA option eligibility (see above), front the premium costs that would be paid for through the PHA, and then apply to the federal government for temporary reimbursement of those premium payments. Once the federal government reimburses the insurer (this could be monthly or quarterly, whichever option insurers determine will provide them necessary liquidity to continue coverage), they could either deduct that reimbursement from the PHAs they set up with said insurer or - for administrative simplicity - load up the PHA as normal and require the insurer to then repay what the federal government reimbursed them.

Require displaced workers taking the COBRA option to open up an PHA through the same insurer they receive COBRA benefits from: If it will take federal agencies several weeks or months to actually deliver cash to eligible workers’ PHAs, and if insurers will be asked to advance some premium payments on behalf of enrollees, one way to prevent administrative confusion is to require that any worker using the PHA option to retain their COBRA coverage open a PHA through their COBRA insurer. This would help ensure that an health insurance company is not covering payments on behalf of a COBRA enrollee and then waiting on that enrollee to pay them back from an PHA that is set up with some other insurer or with a bank.

A Possible Model: Healthy Indiana Plan’s POWER Accounts

As interested policymakers consider the PHA option above, one potential model for plan design is the Healthy Indiana Plan (HIP) Pioneering the Personal Wellness and Responsibility (POWER) account. HIP is Indiana’s Medicaid expansion plan, pioneered by Vice President Mike Pence (formerly the governor of Indiana) and CMS Administrator Seema Verma.

HIP is open to all Indiana adults making between 0 percent and 138 percent of the FPL. There are two major kinds of HIP plans, HIP Basic and HIP Plus. HIP Plus is a comprehensive health care plan, including vision and dental coverage, and comes with almost no co-pays for covered health care products and services. HIP Basic is a less comprehensive plan with small co-pays, like $4 for a doctor’s visit or $75 for a hospital stay. All HIP members are automatically enrolled in HIP Plus (more on why below).

All HIP members have a POWER account. The state of Indiana fills this HSA-like account with $2,500 each year, and over the course of 12 months HIP members pay back a small portion of that through small monthly contributions ($10 per month for people at 100 percent of the FPL, $20 per month for people at 138 percent of the FPL, and less than $10 per month for people below 75 percent of the FPL). Other than those small monthly contributions, though, HIP members have barely any cost-sharing requirements. Their first $2,500 of medical expenses (the ‘deductible’) is covered through the POWER account, and the state covers nearly all expenses after $2,500.

A HIP member who has money left in their POWER account at the end of the year can roll those funds over to the next year, which decreases their required monthly contribution. If a HIP member completes certain preventive services during the year, the state will match their rollover funds at 100 percent - further decreasing a HIP member’s required contributions for the next year.

There are modest penalties for HIP members who do not keep up with monthly contributions, which are meant to encourage members to contribute month to month. For members making between 101 and 138 percent of the FPL, failure to make monthly payments will result in a six-month suspension from the program. For members making 100 percent of the FPL or less, failure to make monthly payments drops them from HIP Plus to the less generous HIP Basic. Certain adults with medical conditions are exempt from the penalties, as are individuals living in a disaster zone.

While the POWER model would not translate perfectly to our PHA option, it is a demonstration that governments can cleanly and widely distribute HSA-like accounts to beneficiaries in need. According to a 2018 progress report from the state of Indiana to CMS:

“There was an increase in enrollment from approximately 370,000 fully and conditionally enrolled members at the end of Demonstration Year One...to approximately 423,000 fully and conditionally enrolled members at the end of Demonstration Year Three.” [a 14-percent increase]

The program was cost-effective, meeting “budget neutrality requirements” for three years in a row and coming in at a lower cost than originally projected for the program.

One reasonable conclusion? Government-funded, temporary, HSA-like accounts can be done at scale, and there is expertise at the federal level to do it.

The Shortfalls of Existing Options

People who currently lose their ESI have a few options to obtain insurance, typically within 30 to 60 days of their job loss:

COBRA: They can elect for Consolidated Omnibus Budget Reconciliation Act (COBRA) continuing health coverage, which almost all employers are required to offer. COBRA allows employees to continue on their ESI plan, typically for up to 18 months after the job loss, but COBRA coverage is expensive. COBRA recipients usually must cover 102 percent of the plan’s premium costs; to put that in perspective, in 2019 employers covered - on average - 83 percent of an individual plan’s premium costs and 71 percent of a family plan’s premium costs. Existing studies suggest a majority of COBRA-eligible workers do not take up the option, with an overwhelming majority citing cost as the primary reason why they do not opt in to COBRA.

Affordable Care Act (ACA/Obamacare) plans: Individuals making between 0 percent and 400 percent of the FPL (up to $51,040 per year for individuals and $104,800 per year for a family of four) are eligible for premium tax credits (PTCs) that offset the cost of a plan on the ACA marketplace. KFF has a helpful subsidy calculator that estimates the impact of these subsidies. For example, a family of four making 400 percent of the FPL ($104,800), with two 40 year old adults and two children (one 10 years old and one 5 years old), would receive around $7,608 per year in PTC financial support, covering 43 percent of their premium costs on the ACA marketplace. The family would be responsible for the remaining $10,073 per year. While this is a less expensive option for most people than COBRA, some families with unemployed workers may still struggle coming up with hundreds of dollars per month for ACA coverage. Of course, this large subsidization rate is underwritten through taxpayers.

Medicaid: Displaced workers making up to 138 percent of FPL ($17,609 per year for individuals in 2020, $36,156 for a family of four) are eligible for Medicaid in the 36 states (plus Washington, D.C.) that expanded Medicaid under the ACA. In 14 states that did not expand Medicaid, many of these adults will not be eligible. In both expansion states and non-expansion states, though, the benefit will only help a subset of the workers who lose their jobs due to the pandemic. Even more concerning is the strain the pandemic will put on the federal-state cost-sharing structure of Medicaid. Though the Phase 3 relief package included a temporary 6.2-percent increase in the federal government’s share of Medicaid costs in all 50 states, states with stressed budgets may still face significant difficulties in covering the costs of new and existing Medicaid beneficiaries through the duration of the pandemic.

Short-term limited duration (STLDI) plans: These plans, which the Centers for Medicare and Medicaid Services (CMS) recently determined could last up to 12 months and be renewed for up to three years (an expansion of the Obama administration’s limits of STLDI), are designed to benefit people experiencing what they anticipate will be temporary gaps in their insurance coverage. These plans are often less expensive than ACA marketplace plans, but that is partly because they don’t have to comply with certain ACA requirements regarding lifetime limits and pre-existing condition protections. While the Trump administration has expanded STLDI options for consumers, they may not be the best choice for all workers and families whose lose their ESI plans due to a job loss.

To review, here are just a few reasons why the existing options are not sufficient to support the millions of people who will lose ESI during the economic downturn:

A majority of workers eligible for COBRA say it is too expensive.

ACA plans may offer workers and their families a more affordable option than COBRA, but some middle-class families could still be on the hook for hundreds of dollars per month in premiums. And unfortunately, proponents of expanding the ACA have recommended permanent changes to the program during this pandemic that will cost taxpayers billions of dollars long after the crisis is over.

Medicaid covers too few of the workers who will lose ESI, whether those workers are in an expansion state or not. And with states already struggling to handle the public health and fiscal impacts of the crisis in a number of ways, any additions to Medicaid enrollment will put additional pressures on state budgets.

STLDI plans may work as an affordable option for some people hoping to experience only brief disruptions in their health insurance coverage, but may not work as well for families with high health care costs and/or pre-existing conditions.

ACA PTC Expansion

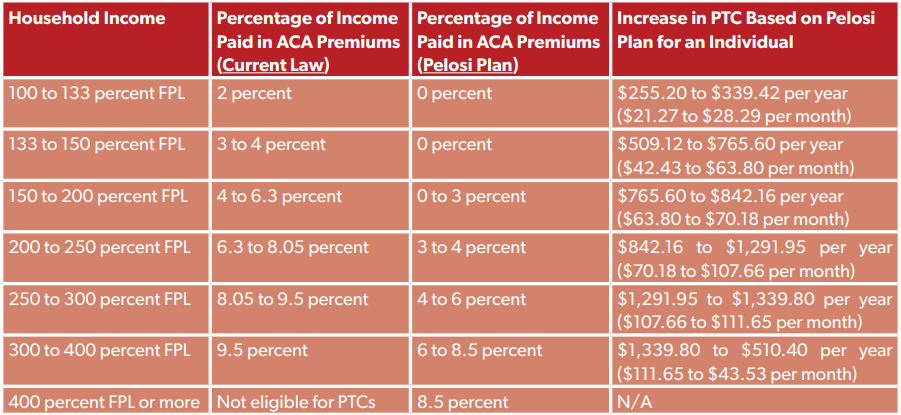

Speaker Pelosi’s Phase 3 pitch included a permanent expansion of the ACA’s premium tax credits. Her plan would have lowered the maximum percentage of income a household on an ACA plan would have had to pay in premiums, from 9.5 percent of household income to 8.5 percent of income. This also would have included more generous PTCs at every income level and would have allowed families making over 400 percent of the FPL ($51,040 for individuals, $104,800 for a family of four) to receive PTCs. Here’s a demonstration of the changes:

Though the per-year and per-month federal costs for PTC expansion may be lower than the costs for the PHA option, there are a few short- and long-term issues with solely relying on permanent ACA expansion to help workers losing their ESI:

Even PTC expansion will leave many households (especially those making 400 percent of the FPL or more) on the hook for thousands of dollars in ACA premium costs, not to mention their deductibles and cost-sharing requirements. The PHA option may be more expensive in the short term, but that is because it is meant to help displaced workers temporarily bridge the gap between the loss of their ESI and their next job with access to ESI.

In the long term, a permanent expansion of PTCs will be more expensive for taxpayers. As demonstrated by the table above, the more generous PTCs in the Pelosi plan add up to hundreds of dollars in additional federal costs per ACA enrollee, not to mention hundreds of dollars in likely federal costs for enrollees making north of 400 percent of the FPL.

There is another reason that PTC expansion will be more expensive in the long term, and it has to do with the fundamental design of PTCs. The PTCs set a maximum income limit that a household can pay in ACA premiums, but premium growth is far outpacing wage growth and has been for some time. For example, take a household of four that has $100,000 of income in 2020, a $20,000 premium, and an 8.5-percent limit on the amount they can pay in ACA premiums under the Pelosi plan. That means they will pay $8,500 in ACA premiums over the year, and the PTCs will cover the other $11,500. Let’s assume premiums grow at five percent and wages by three percent over the year. The household’s 2021 income will be $103,000, they will have a $21,000 premium, and they will still have an 8.5-percent limit on the amount they can pay in ACA premiums under the Pelosi plan. That means they will pay $8,755 in ACA premiums over the year, and the PTCs will cover the other $12,245 (a $745 increase for the taxpayer). It is easy to see how exponential premium growth, compared to more modest wage growth, could lead to exploding federal costs for PTCs, both above and below 400 percent of the FPL.

Permanent ACA expansion would offer some small and temporary relief in the short term, but would fall short of the immediate relief needed for displaced workers. It would also be more expensive than the PHA option in the long run.

The COBRA Subsidy

The American Recovery and Reinvestment Act (ARRA) of 2009 stimulus package paid 65 percent of displaced workers’ premium costs under COBRA for 15 months, as long as that worker lost their job in September 2008 or later. The subsidy started to phase out for individuals making more than $125,000 per year and joint tax filers making more than $250,000 per year, and phased out completely at $145,000/$290,000.

According to a Department of Treasury study, “the ARRA subsidy reduced the cost of COBRA [for the typical family] from about $13,500 to $4,725.” This could be helpful to individuals and families looking to retain their ESI coverage.

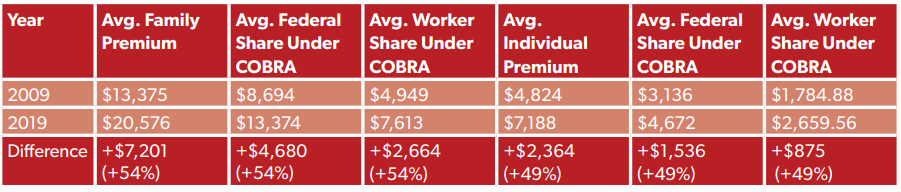

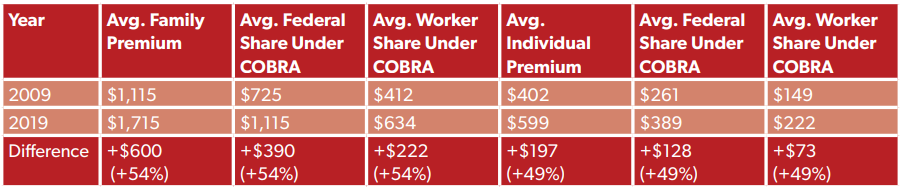

An important caveat for Congress as they consider COBRA subsidies in 2020, though, is that ESI plans are much more expensive than they were even 10 years ago. According to KFF, the average ESI premium for an individual plan in 2019 was $7,188 per year ($599 per month), 49 percent higher than in 2009. It was $20,576 per year for a family plan ($1,715 per month), 54 percent higher than in 2009. Not only would this make the same level of subsidy (65 percent) more expensive for the federal government, but it would also make it harder for workers to pay even their subsidized share (37 percent).

We illustrate this dynamic in the table below, expressed in per-year costs:

Or, expressed as per-month costs:

Another issue with simply copying and pasting the 2009 model is how that COBRA subsidy worked for employers. Employers covering their former workers under COBRA were required to front the 65 percent subsidy, and the federal government reimbursed them through a payroll tax credit. It doesn’t appear that cash flow was a major issue for the employers participating in the 2009 program, but it may be a more significant concern in 2019, given the scale of the economic disruption caused by COVID-19 and the rising cost of ESI.

While the added federal costs of a 65-percent COBRA subsidy are a legitimate concern, so are the concerns that a 65-percent subsidy is not enough for displaced workers. One issue with a lower subsidy is adverse selection. As KFF points out:

“Subsidizing COBRA premiums 100% during the emergency period would make this option more affordable to those out of work. In addition, a full subsidy could reduce adverse selection. The people most likely to elect unsubsidized COBRA tend to have costly health care needs; one survey estimated 4.8 million COBRA beneficiaries in 2008 cost their former employers more than $10 billion that year.”

What’s more, survey data collected by the Departments of Treasury and Labor following the 2009 subsidy program indicate that relatively few subsidy-eligible workers even took up the option, given how expensive COBRA coverage is. The Treasury Department estimated that between one-quarter and one-third of “eligible unemployed workers” enrolled in COBRA. There was also a significant lack of knowledge about the COBRA subsidy - “less than one-third of subsidy-eligible workers reported knowledge of the subsidy,” even though employers were required to notify their employees.

The unique conditions of this economic downturn, and the lessons the government learned from the 2009 subsidy, lead to some important questions policymakers would need to answer:

At what level do policymakers subsidize COBRA premiums? With much higher ESI costs than in 2009 and much larger job losses, a 65-percent subsidy will cost the federal government much more than it did in 2009. Congress budgeted $25 billion over three years for the 2009 COBRA subsidy. Reports indicate the program cost far less than that, primarily due to a lack of COBRA take-up. It is difficult, though, to predict take-up in this economic crisis, either at a 65-percent subsidy level or at some higher level. A 100-percent subsidy, as suggested by KFF, could help prevent adverse selection and provide more support for displaced workers than the 2009 subsidy. However it would also increase COBRA take-up and, consequently, the federal government’s costs to offer the program.

How should stakeholders spread the word? Clearly, a majority of subsidy-eligible workers in 2009 did not know the COBRA subsidy even existed, despite legal requirements for employers to share that information. Would a COBRA subsidy program need to include a public awareness campaign, and/or utilize messengers beyond just a displaced worker’s employer?

We also note that, if policymakers’ goal is to help displaced workers retain access to their ESI, the PHA option accomplishes this while giving workers even more options to obtain coverage (including coverage on the ACA marketplace or through an STLDI plan). The PHA option would also eliminate the need for employers to ‘front’ the COBRA subsidy costs, which could create cash flow troubles, and could also mitigate some of the awareness issues that accompanied the 2009 COBRA subsidy.

Conclusion

Clearly one of the most difficult questions policymakers are facing is how to help the millions of people who will lose access to their health insurance in the coming months. We acknowledge that there is no perfect answer, but the following principles guide us to the conclusions we reach in this Issue Brief:

To best contain costs, solutions should be narrowly tailored to reach displaced workers. We believe policy options should be crafted for those who cannot turn to Medicaid, Medicare, a spouse’s coverage, or some other affordable option.

Solutions should not create a permanent, open-ended expansion of benefits that will leave taxpayers on the hook for billions of dollars long after the crisis is over. Instead, solutions should be focused on helping displaced workers bridge the gap between their loss of ESI and their next job with health insurance coverage.

Solutions should put patients in control of their health care, letting them choose whatever option (ACA plan, COBRA, STLDI, or something else) that works best for them and their families.

For all of these reasons, we believe our Pandemic Health Account (PHA) proposal merits consideration from lawmakers. The federal government could help set up these targeted, dollar-limited accounts to help displaced workers bridge their coverage gaps and spend on a plan that fits their needs. Those workers, their families, and ultimately taxpayers, will be better off over the long run. We stand ready to work with policymakers on these ideas, and other creative solutions to meet these unprecedented challenges.