On February 20, President Donald Trump issued a proclamation imposing tariffs under Section 122 of the Trade Act of 1974 to address “fundamental international payments problems.” Several small businesses and states sued to block the tariffs. On April 10, the Court of International Trade (CIT) held a hearing to consider the lawsuits.

Section 122 requires the President to proclaim import duties of up to 15% and/or import quotas for up to 150 days whenever fundamental international payments problems require special import measures to restrict imports to deal with large and serious United States balance-of-payments deficits, to prevent an imminent and significant depreciation of the dollar in foreign exchange markets, or to cooperate with other countries in correcting an international balance-of-payments disequilibrium.

Here are four takeaways from the CIT oral hearing.

1. The definition of “balance of payments” was a major topic. The phrase came up 194 times during the course of the hearing. One of the judges asked: “Please help us figure it out. It’s a term in a statute, and we’re trying to define it.”

Fortunately, the Department of Justice (DOJ) brief to the CIT settles this issue. The DOJ brief points out, “Congress intended that any action taken pursuant to Section 122 be consistent with the then-existing GATT [General Agreement on Tariffs and Trade] rules and any future international rules entered into force.”

Those Restrictions to Safeguard the Balance of Payments rules state:

“Import restrictions instituted, maintained or intensified by a contracting party under this Article shall not exceed those necessary to forestall the imminent threat of, or to stop, a serious decline in its monetary reserves, or in the case of a contracting party with very low monetary reserves, to achieve a reasonable rate of increase in its reserves.”

The DOJ’s position would mean that, for the Trump Administration’s tariffs to be legal under Section 122, they must be intended to address monetary reserves that are very low or seriously declining. And the U.S. Treasury Department reports that the United States has $252.565 billion in official reserve assets as of April 3, 2026, the highest level in history.

2. In oral arguments, the DOJ disregarded this and swapped in a different definition: “Our main legal position is that you have to look to what comprises the balance of payments. Look to the sub-accounts to decide whether there’s a deficit or not. The current account is the most appropriate account to look to for whether there is a deficit in the balance of payments.”

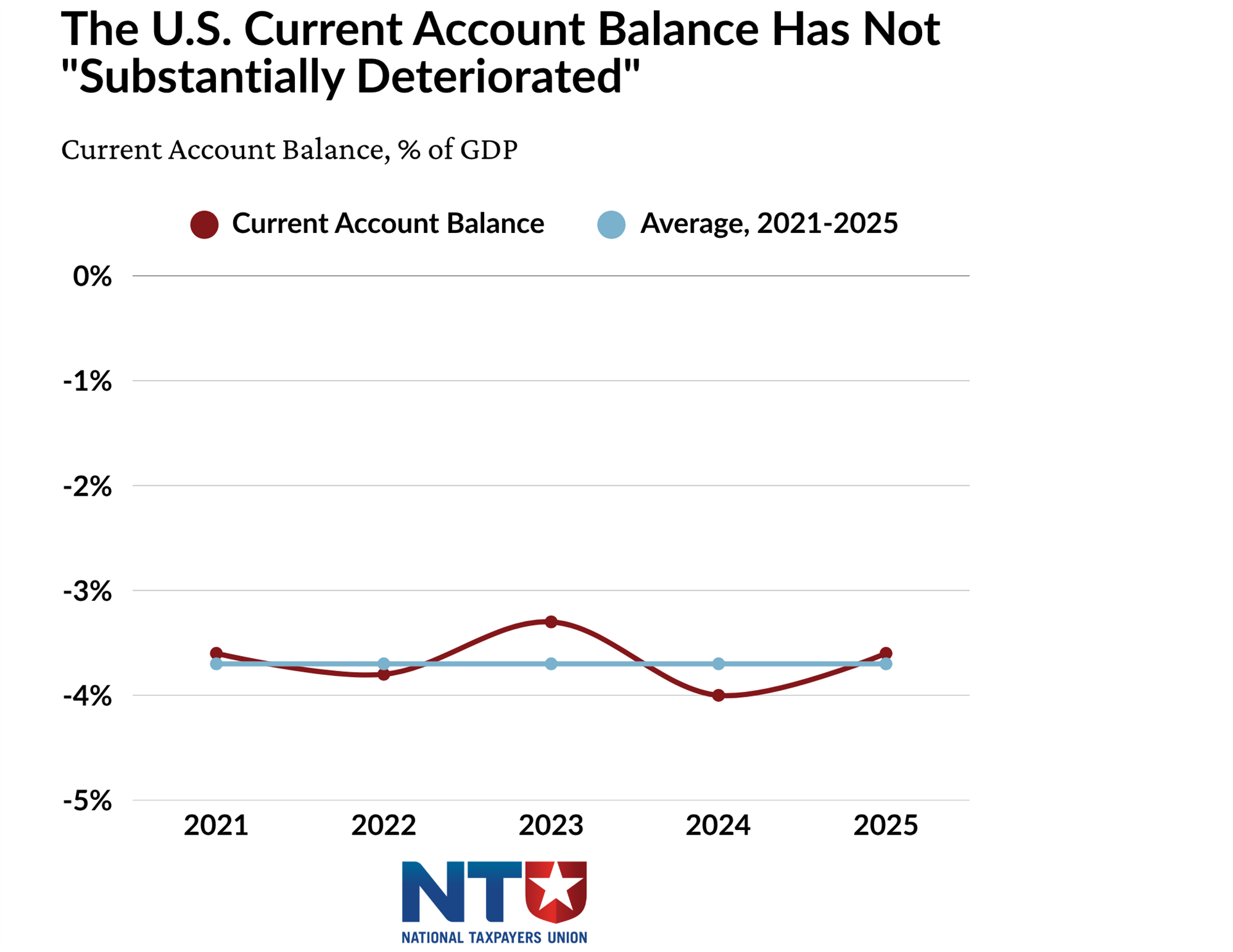

3. DOJ proceeded to exaggerate the size of the U.S. current account deficit, arguing the United States has suffered a “substantial deterioration:” “Our current account deficit is now in excess of $1.1 trillion and has been growing larger and larger over the last five years since 2020.”

That is mostly incorrect. The current account balance actually shrank by $69 billion between 2024 and 2025. A more meaningful measure is the size of the current account balance relative to the size of the U.S. economy. By this measure, the current account deficit was smaller in 2025 than in 2024 and also lower than the average for the last five years, 2021–2025.

4. DOJ asserted that the Court cannot review a presidential finding that there is a large and serious balance of payments deficit: “We’re acknowledging the court does have the power to interpret what the statute means. What does balance of payments deficit mean, okay, that’s one response. But the legislative history does recognize that the President has a measure of discretion. Where that discretion comes into account is making the factual finding, which the court can’t review: whether the deficit is large and serious.”

The Justice Department’s position ultimately reduces Section 122 to a blank check—“the President can impose tariffs of up to 15% for up to 150 days whenever he feels like it.” That’s a hard argument to square with the plain text of the statute, the GATT/WTO rules that even DOJ says the government must respect, and the actual trajectory of the U.S. current account deficit since 2000. The Administration has clearly misconstrued Section 122 and acted outside its delegated authority.