Key Facts

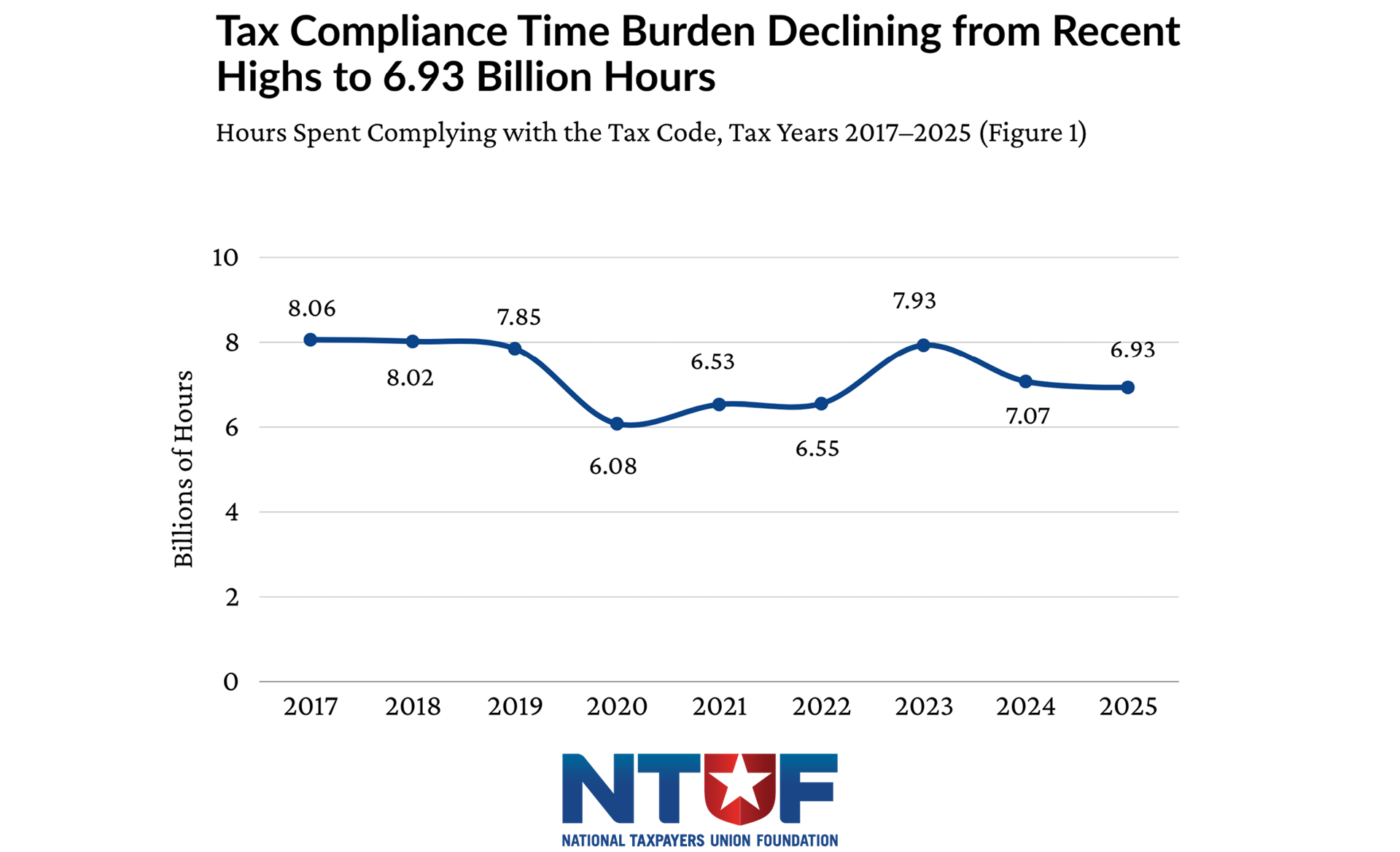

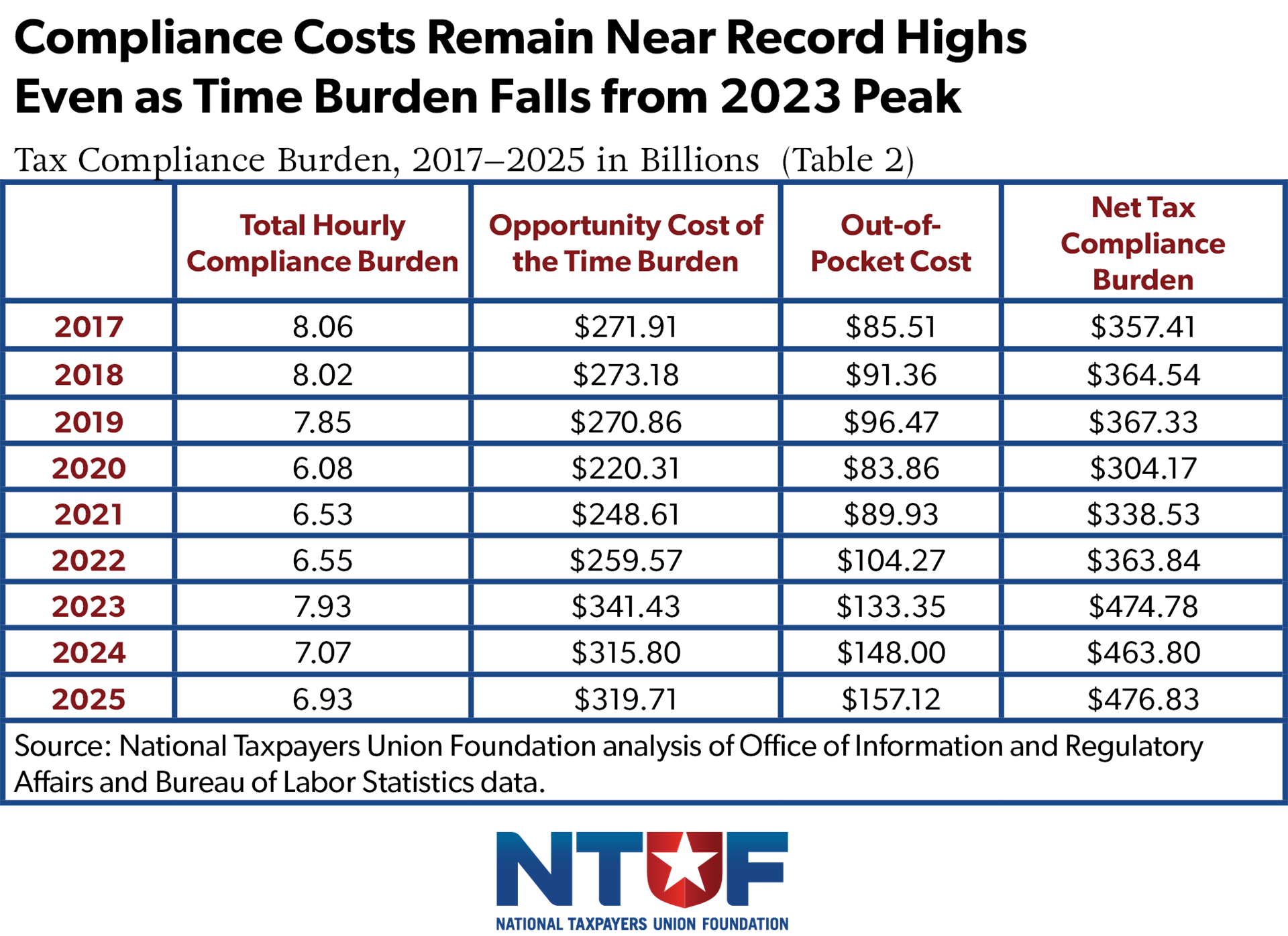

- Taxpayers will spend an estimated 6.93 billion hours to complete their 2025 taxes—down from a peak of 7.93 billion hours in 2023 and marking the second consecutive annual decline.

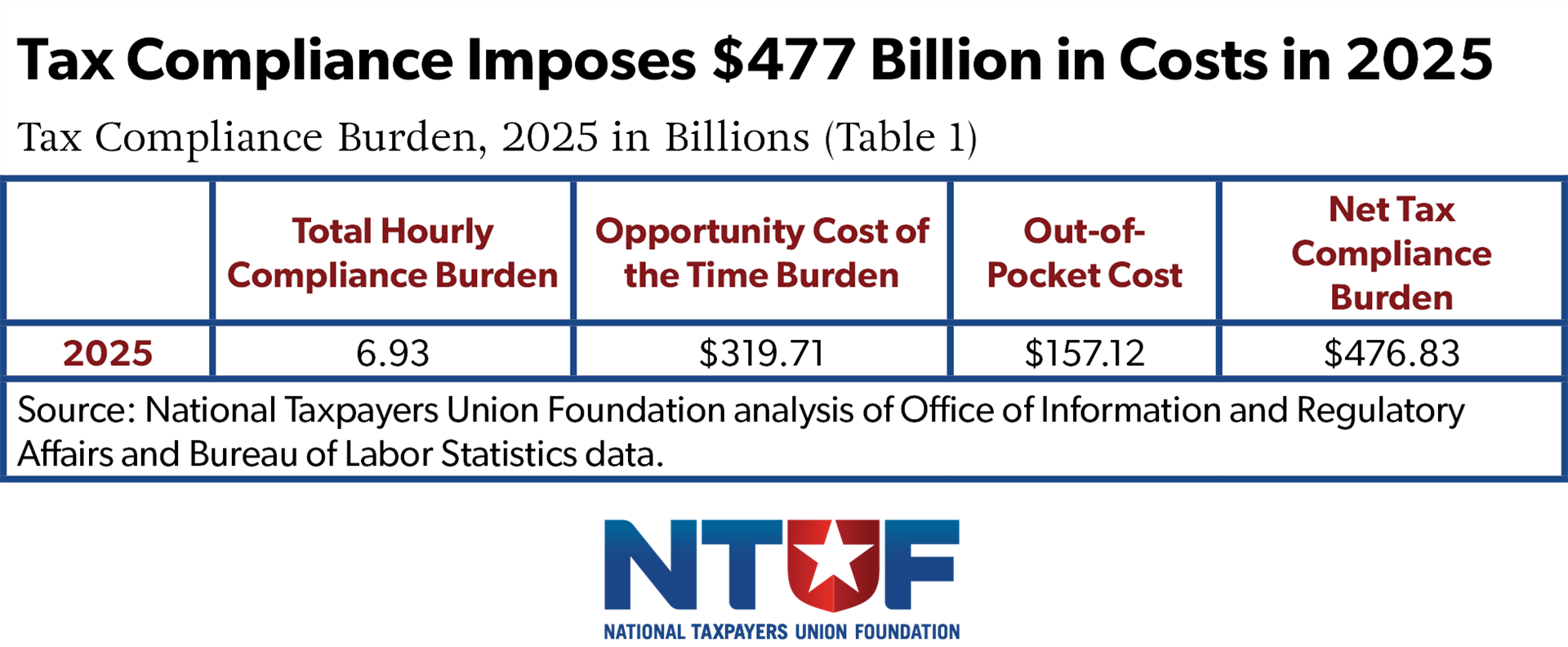

- Tax compliance costs include $319.7 billion in lost time and at least $157.1 billion in out-of-pocket expenses, including tax software and professional services.

- The out-of-pocket estimate is incomplete because the IRS has not yet completed analysis for some tax forms, as required under the Paperwork Reduction Act.

- Since 2000, Congress has made 9,630 changes to the tax code—roughly one per day. Most changes add new rules, thresholds, or reporting requirements that make compliance more burdensome.

- The TCJA reduced the tax code to 3.96 million words, but subsequent pandemic-era provisions and new deductions have pushed it back up to roughly 4.26 million words.

- By nearly doubling the standard deduction, the Tax Cuts and Jobs Act simplified filing for about 30 million Americans—and the One Big Beautiful Bill Act helped lock in those gains, with more than 90% of taxpayers avoiding itemization altogether.

Introduction

For the 2026 filing season (for income earned during tax year 2025), taxpayers will spend nearly 6.93 billion hours complying with the federal tax code. This is equivalent to $319.7 billion in lost productivity based on private-sector labor costs. This is a substantial hidden cost on taxpayers, accounting for the value of time spent navigating the tax system instead of working, investing, or engaging in other activities.

Federal taxes impose costs that extend beyond what taxpayers ultimately owe each April to the Treasury. Complying with the tax code requires Americans to collectively spend billions of hours each year understanding complex rules, gathering documentation, and completing forms. In addition, taxpayers will incur at least $157.1 billion in out-of-pocket expenses for paid preparers or software. However, the actual amount is likely substantially higher, as the IRS has not fully estimated these costs across many complicated forms, as is required under the Paperwork Reduction Act.

This marks the second consecutive year of decline in the time burden following a peak of 7.93 billion hours in 2023. On the other hand, the overall cost of compliance remains near historic highs, driven in large part by inflation and the rising out-of-pocket expenses for tax preparation and assistance.

There is some encouraging news in the data. For the portion of the tax code most familiar to Americans—individual income taxes filed on Form 1040—the Internal Revenue Service (IRS) projects that the total time burden will fall by roughly 181 million hours, freeing up an estimated $8.35 billion in opportunity costs for taxpayers. Overall, the average taxpayer will spend about 12 hours and $290 to complete their return.

The One Big Beautiful Bill Act (OBBBA) locked in substantial compliance savings for taxpayers, including the doubled standard deduction. Going forward, both the IRS and Congress have opportunities to build on this progress by improving transparency in burden measurement and advancing reforms that simplify the tax code, reduce unnecessary filing requirements, and make the tax filing experience more efficient for taxpayers.

Much of the recent reduction in compliance hours reflects improvements in the IRS’s burden estimation methodology rather than fundamental simplification of the tax code. Updates to the Service’s modeling better capture taxpayer behavior and filing patterns, but significant gaps remain, particularly in estimating out-of-pocket costs across many forms, as is required under the Paperwork Reduction Act.

The Tax Code’s Complexity and Compliance Burden

Background and Methodology

Each year, the Internal Revenue Service (IRS) is required under the Paperwork Reduction Act (PRA) to estimate the time and out-of-pocket costs that taxpayers incur when complying with federal tax forms and reporting requirements. These estimates for forms or groups of forms, referred to as “information collections,” are reviewed and approved by the Office of Management and Budget (OMB) and published through the Office of Information and Regulatory Affairs (OIRA), along with detailed supporting documentation describing the underlying assumptions and methodology.

NTUF compiles and analyzes these IRS burden estimates across all tax-related information collections to measure the total cost of complying with the federal tax code. A copy of the IRS burden data was captured on March 27, 2026 and updated on April 7 to include a significant revision made by the IRS to the estimate for the Employer's Quarterly Federal Tax Return information collection. These collections account for a wide range of activities, including recordkeeping, tax planning, form completion, and submission, reflecting the full scope of taxpayer compliance obligations.

To better assess the economic impact of the time burden, NTUF converts reported compliance hours into an opportunity cost using average private-sector labor compensation. Based on data from the Bureau of Labor Statistics, the average hourly compensation—including wages, salaries, and benefits—for non-federal civilian workers was $46.15 as of December 2025. Applying this rate to total compliance hours provides an estimate of the value of time that taxpayers spend navigating the tax system instead of engaging in productive activity.

Out-of-pocket cost estimates are drawn directly from IRS submissions under the PRA. However, these estimates remain incomplete, as many IRS information collections report zero costs even though documentation shows that the Service has not yet developed a methodology to calculate them. As a result, the total compliance burden reported in this study likely understates the true financial cost imposed on taxpayers.

IRS Paperwork Dominates the Federal Burden

Before examining trends in tax compliance specifically, it is important to understand the IRS’s outsized impact on the broader federal paperwork burden.

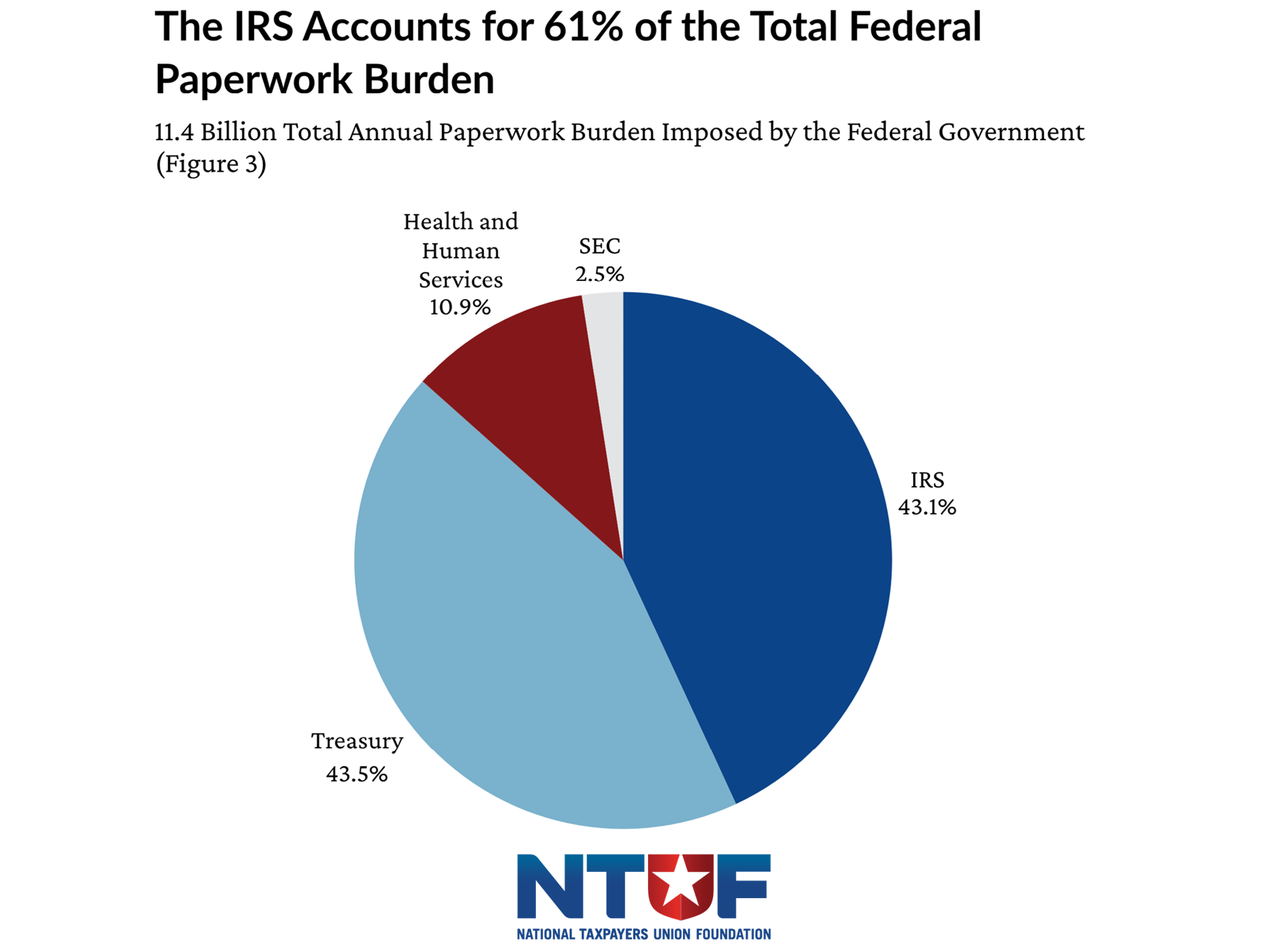

Across all federal agencies, Americans complete an estimated 11.4 billion hours of paperwork this year. Of that total, the IRS alone accounts for 61%. By comparison, the Department of Health and Human Services imposes approximately 1.7 billion hours of paperwork annually, while the Securities and Exchange Commission accounts for about 400 million hours. No other agency comes close to the scale of the IRS’s reporting requirements.

This concentration reflects the central role of the tax system in federal administration, but it also underscores the massive burden that tax compliance places on individuals and businesses. Although IRS forms represent only a small share of total federal information collections, they account for the majority of the time Americans spend complying with government paperwork requirements.

Total Tax Compliance Burden Easing from Record Highs

The latest data shows that the total compliance burden imposed by the tax code is beginning to ease from recent highs. Taxpayers will spend an estimated 6.93 billion hours complying with the tax system in 2025, down from a peak of 7.93 billion hours in 2023. This marks the second consecutive year of decline in reported time burdens.

To put that figure in perspective, 6.93 billion hours is equivalent to over 791,000 years of continuous 24/7 work—a staggering amount of time devoted to tax compliance each year. You would be able to watch the entire Star Trek saga including all of the regular and animated series and movies from start to finish roughly 7.5 million times.

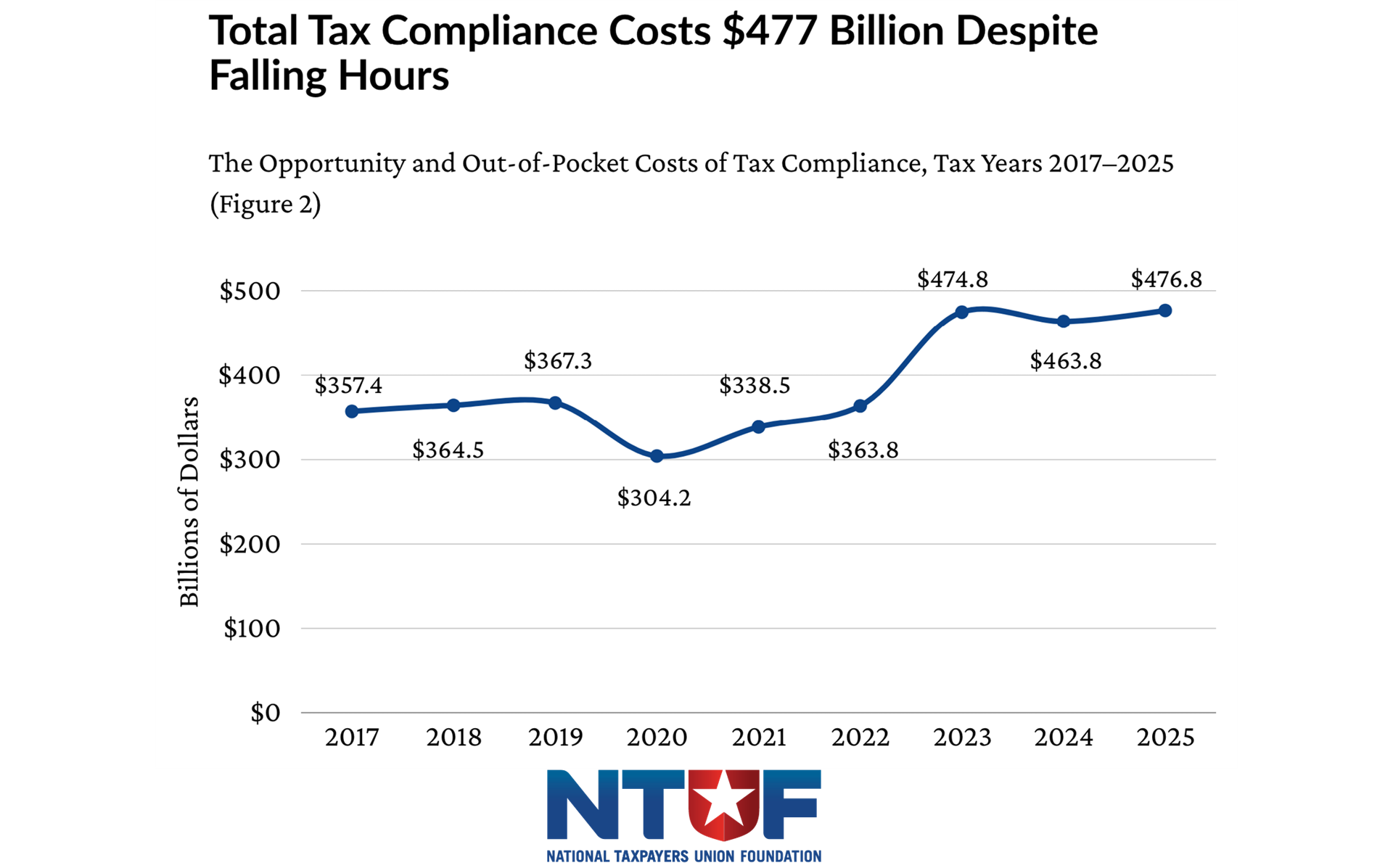

The total cost of compliance remains near historic highs, reaching approximately $477 billion in 2025. This total consists of the opportunity cost of time ($319.7 billion) reflecting the economic value of the 6.93 billion hours taxpayers spend complying with the tax code, and out-of-pocket costs ($157.1 billion) as estimated by the IRS for tax preparation software, professional services, and related expenses.

It is important to note that this figure understates the true cost due to incomplete IRS estimates. Last year, NTUF went through all 392 information collections listed at the time as having zero cost and reported that 102 of these collections—just 26%—had little to no out-of-pocket cost while the rest of the supporting documents acknowledged that cost estimates were unavailable.

If tax compliance were a company, its $477 billion price tag would rank it among the largest enterprises in the Fortune Global 500. The cost of complying with the tax code lags the annual revenues of Walmart ($681 billion) or Amazon ($638 billion) but surpasses Apple ($391 billion).

Comparing the Burden over the Recent Past

Over the longer term, tax compliance burdens have fluctuated in response to policy changes and updates in IRS estimation methods. Following enactment of the Tax Cuts and Jobs Act (TCJA) of 2017, total compliance hours declined significantly—from more than 8 billion hours in 2017 to just over 6 billion hours in 2020—as key reforms like increasing the standard deduction and trimming the number of filers subject to the Alternative Minimum Tax helped reduce paperwork burdens. In subsequent years, reported burdens increased again, reaching a recent high in 2023 before declining over the past two filing seasons.

The IRS also updates the methodology it uses to better capture the impact on taxpayers. For example, the sharp drop in 2020 reflected a long-delayed IRS methodology update that corrected overestimated business compliance hours. This change had been in the works for years, but the IRS held off until after the TCJA’s effects could be measured.

Explaining the Changes in the IRS Information Collection Compared to a Year Ago

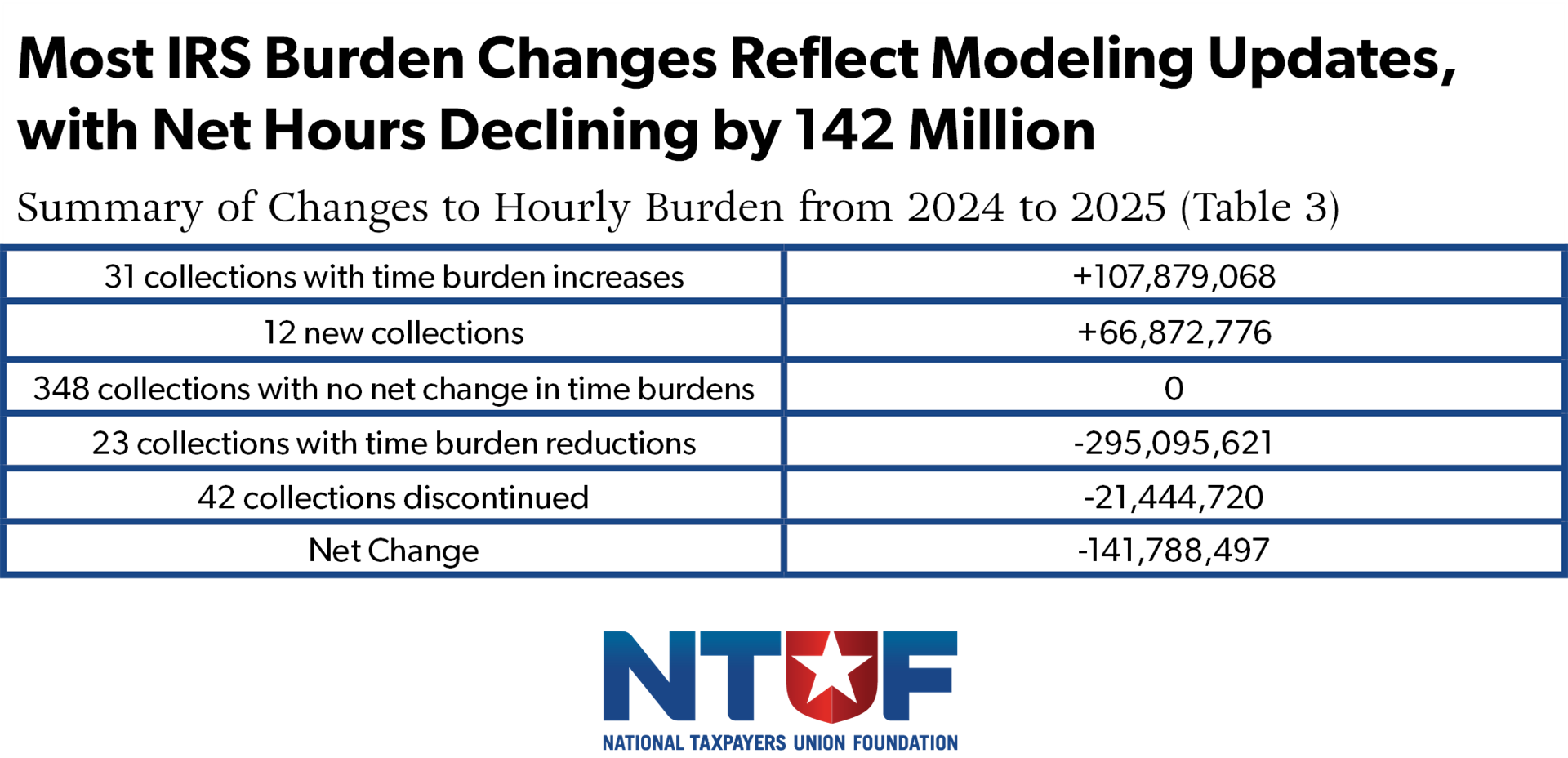

The reported hourly burden for 2025 shows a net decline from the previous year, driven by a combination of discontinued collections and revisions to existing IRS burden estimates.

As shown in Table 3, the number of active IRS information collections fell from 446 to 414 over the past year. At the same time, most collections saw no change in their estimated burden: 349 collections, or 84% of the total, were renewed without any adjustment to their time estimates.

Thirty-one collections had increased burden estimates, adding approximately 107.9 million hours. These increases were driven largely by updated assumptions about the number of filers and responses rather than changes in underlying requirements. For example:

- The largest increase came from applications for Employer Identification Numbers, which added more than 66 million hours following revisions to estimated filers and time per response.

- Similarly, Individual Retirement Account contribution reporting added 9.3 million hours due solely to 22.7 million more expected responses.

- Health Savings and Medical Savings Account-related filings added more than 6.4 million hours reflecting an increase in the number of expected responses by 38.5 million.

There were 12 new information collections, contributing 66.9 million additional hours. Most of this (64.9 million hours) comes from the new Trump Account election. The IRS’s initial estimate notes:

“IRS estimates that during 2026 up to 45 million individuals may be impacted by filing the new Form 4547 to provide this information with respect to the 74 million potential children who may be eligible for Trump accounts during the first year of the program. The number of filings will decrease in future years based on the number of children born in a given year. The burden estimate for the average time to complete the collection of information for each respondent is 1 hour 28 minutes. IRS estimates that approximately 45 million respondents will be impacted.”

Twenty-three collections saw reduced burden estimates, lowering the total by approximately 295 million hours. The majority of this reduction—about 181 million hours—comes from revised estimates for individual income tax compliance, reflecting updates to IRS modeling and filing assumptions rather than changes in the underlying complexity of the tax code.

Business income tax collections also saw a significant reduction, declining by approximately 78.1 million hours, again driven by updated estimates of the number of responses. Additional reductions occurred across several collections where revised filing data lowered projected respondent counts, including Form 4506-C, which is used to authorize third parties to request tax transcripts, due to a revised Service estimate decreasing the number of respondents.

The Complexity Burden of Sections of the Tax Code

Top 10 Time Burdens of the Tax Code

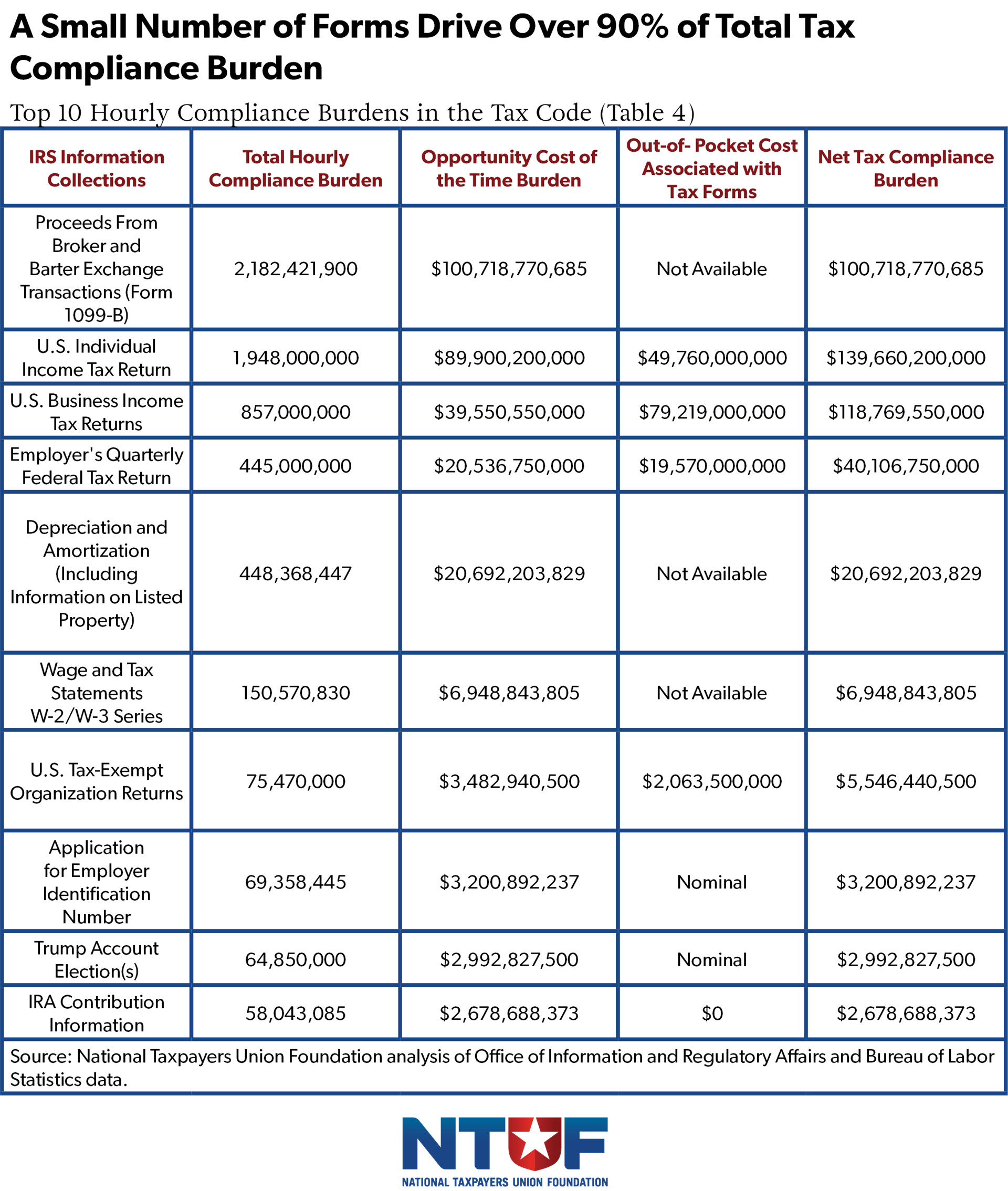

A relatively small number of tax forms account for a disproportionate share of total compliance burden. As shown in Table 4, the largest IRS information collections impose hundreds of millions of hours of paperwork annually, often driven by reporting requirements rather than the filing of individual tax returns. Combined, these represent 91% of the total burden hours and 93% of the compliance costs associated with the tax code.

With an estimated 2.18 billion hours required to comply, Form 1099-B alone surpasses the entire burden of individual income tax returns. The IRS anticipates receiving 4.36 billion submissions of this form—nearly 13 for every person in the United States. This information collection vastly expanded due to digital asset taxation provisions enacted in the Infrastructure Investment and Jobs Act.

Other major contributors include information reporting requirements for retirement accounts, health savings accounts, and business income, as well as new reporting requirements associated with “Trump Accounts,” which now appear among the largest sources of compliance burden. Together, these collections reflect the increasing complexity of tracking and reporting financial activity across multiple parts of the tax code.

In the public-facing database, six of these collections appeared with $0 out-of-pocket costs. In reviewing the supporting statements associated with each of these, only three likely have an actual zero or minimal cost. The IRA supporting statement noted, “There are no start-up or maintenance costs for this collection. The collection does not require respondents to obtain specialized equipment or professional services.” Similarly, the supporting statements for Employee Identification Numbers and the Trump Accounts documented that the expenses would be “nominal.”

The supporting statements of the remaining three information collections each had language indicating that the IRS has not been able to ascertain the burdens imposed on taxpayers. For example, the supporting statement for the 1099-B includes the following:

“This information collection will be included in the consolidated OMB submission for information returns currently being developed. IRS is working on the methodology for evaluating information return burden and cost; and will update the cost and burden estimates as part of the consolidation.”

In cases like this, OIRA’s website should list the out-of-pocket expense as “Not Available” or “Unknown,” not as zero.

The Overall Individual Income Tax Compliance Burden: Lower than Last Year

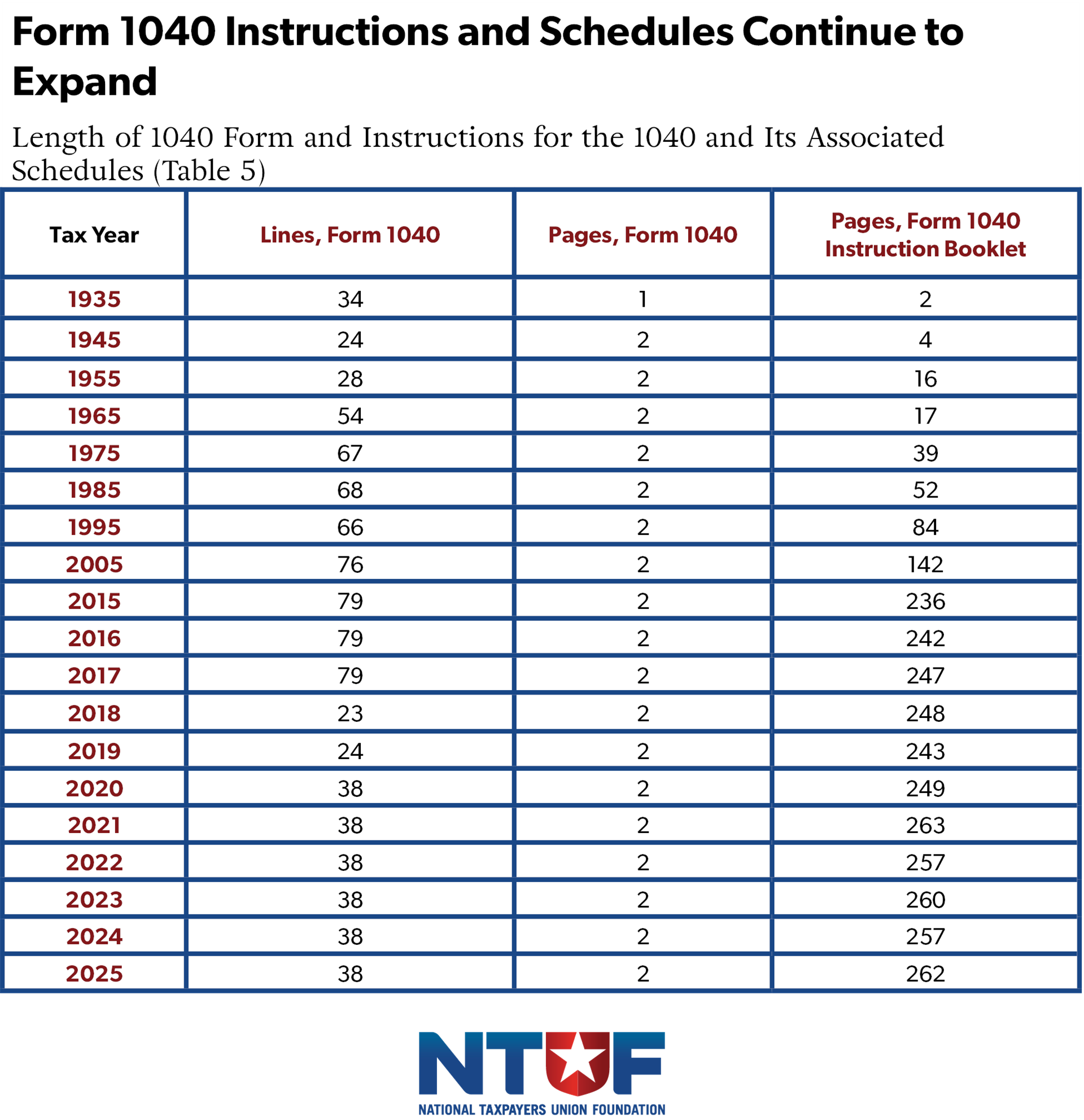

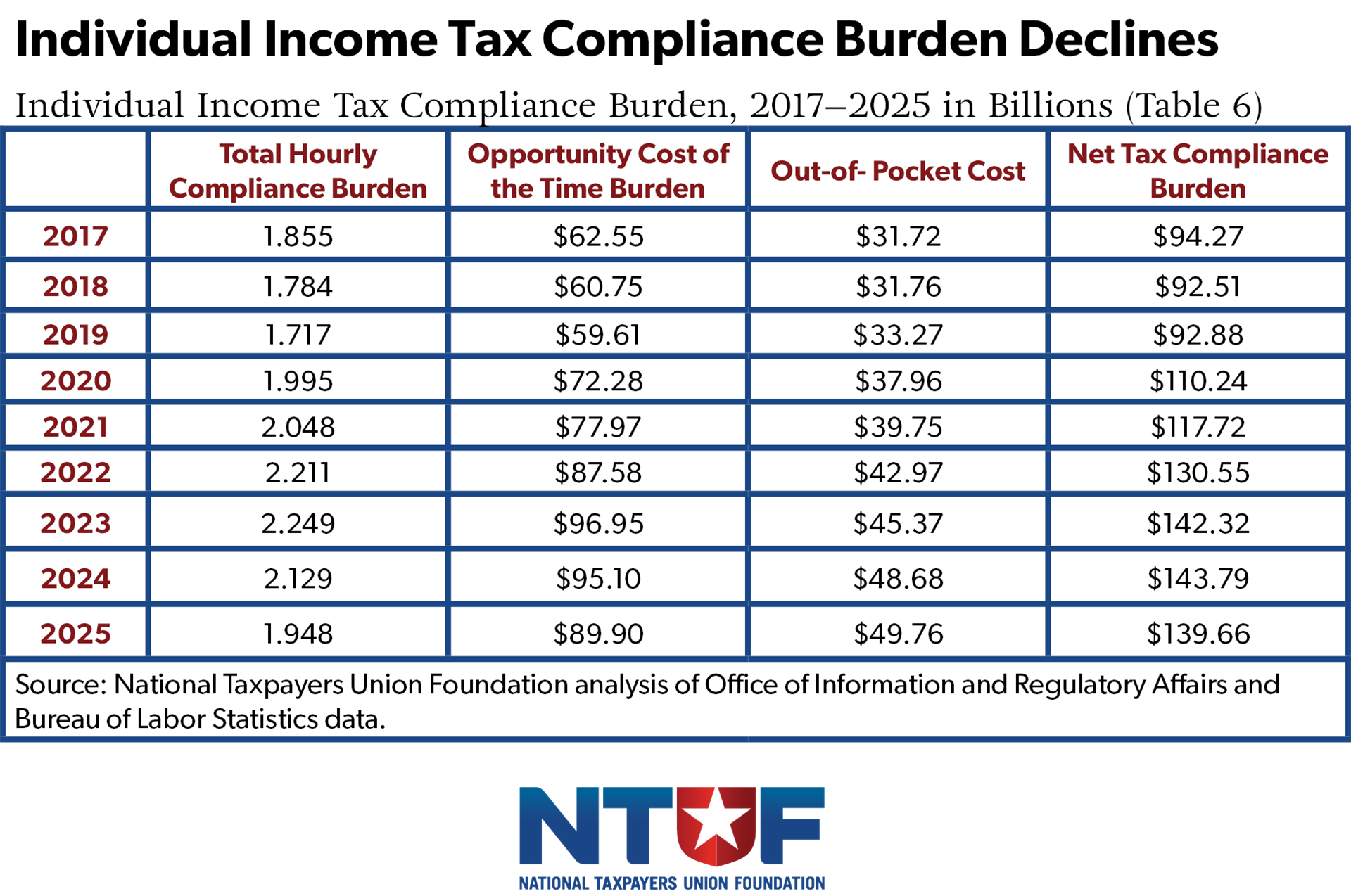

The part of the tax code most familiar to Americans is Form 1040, along with its associated schedules and instructions. While the form itself has been simplified on paper in recent years, the forms and instructions are much longer than in the early years of the income tax code. New deductions for this year added to the length of instructions associated with the 1040 form compared to last year.

As shown in Table 6, the hourly compliance burden for the individual income tax declined again in 2025. Much of the decline in reported time burden reflects updates to the IRS’s burden model and underlying filing assumptions rather than a meaningful simplification of the tax code. At the same time, new provisions—such as expanded credits, exclusions, and reporting requirements—are expected to increase compliance time for certain taxpayers, partially offsetting these reductions. However, it should be remembered that, if the TCJA expired, burdens—and rates—would have gone up significantly.

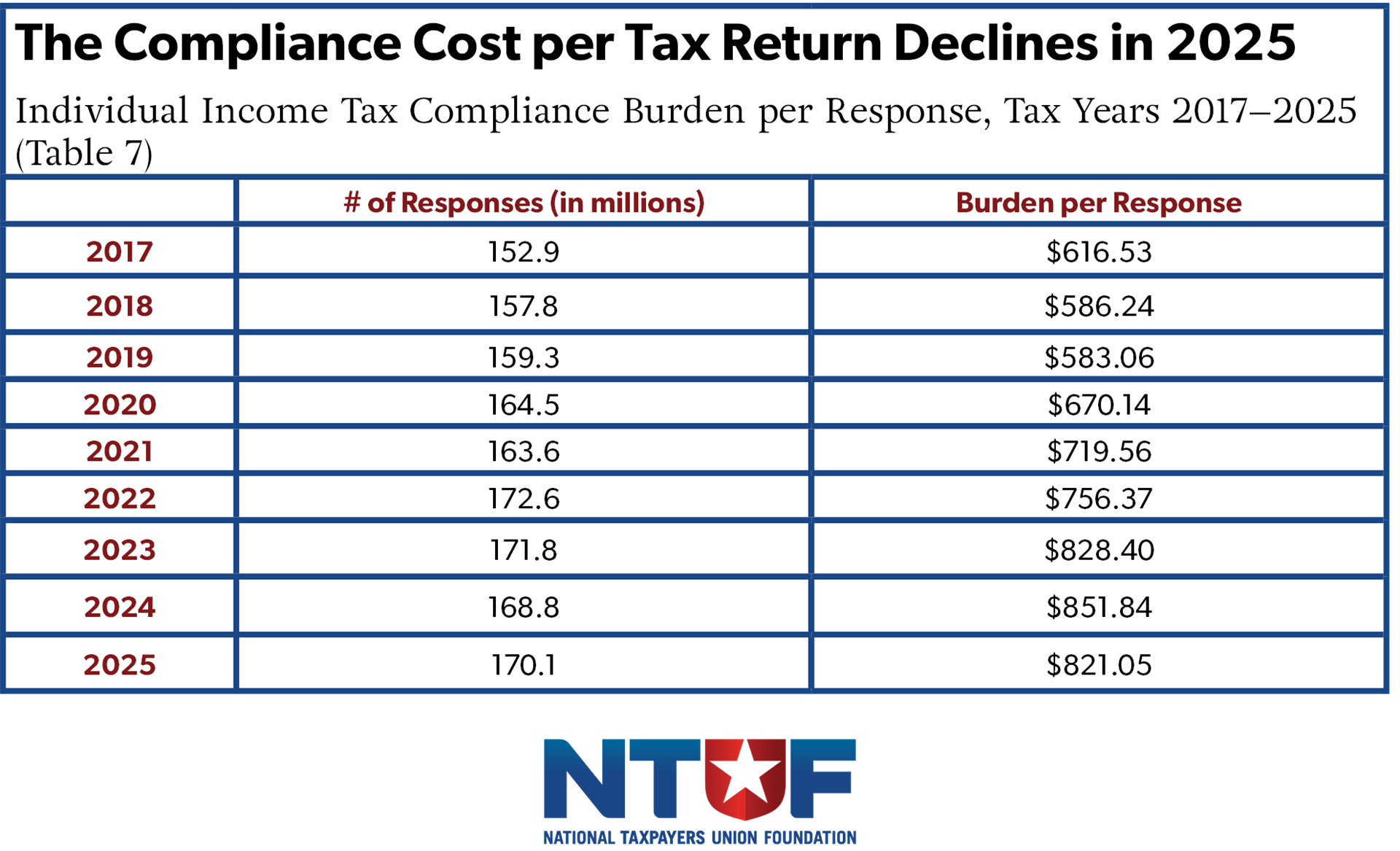

Table 7 shows that the burden per filer has eased modestly in 2025 following several years of increases. The average cost per return rose from about $616 in 2017 to nearly $852 in 2024, before declining to approximately $821 in 2025. While this represents a welcome improvement, the cost per return remains well above pre-pandemic levels.

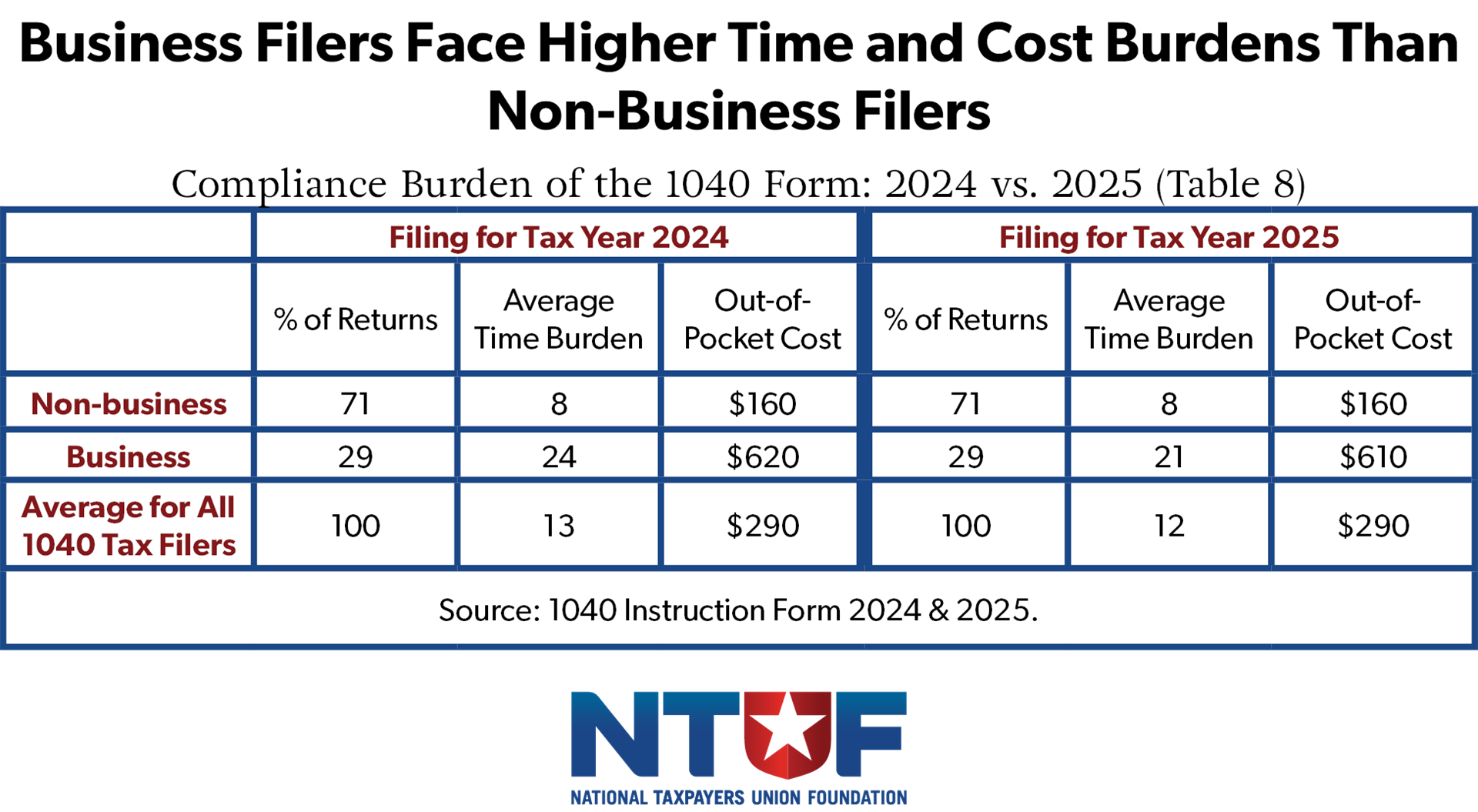

The experience of taxpayers varies significantly depending on the complexity of their return. As shown in Table 8, non-business filers—who account for about 71% of returns—spend roughly 8 hours and $160 to complete their return.

In contrast, filers with business income face substantially higher burdens. Although their average time burden declined from 24 hours to 21 hours in 2025, their out-of-pocket costs remain high at about $610 per return. Overall, the average taxpayer spent about 12 hours and $290 to file in 2025, reflecting a modest decline in time with little change in costs.

Business Income Tax Compliance Burden

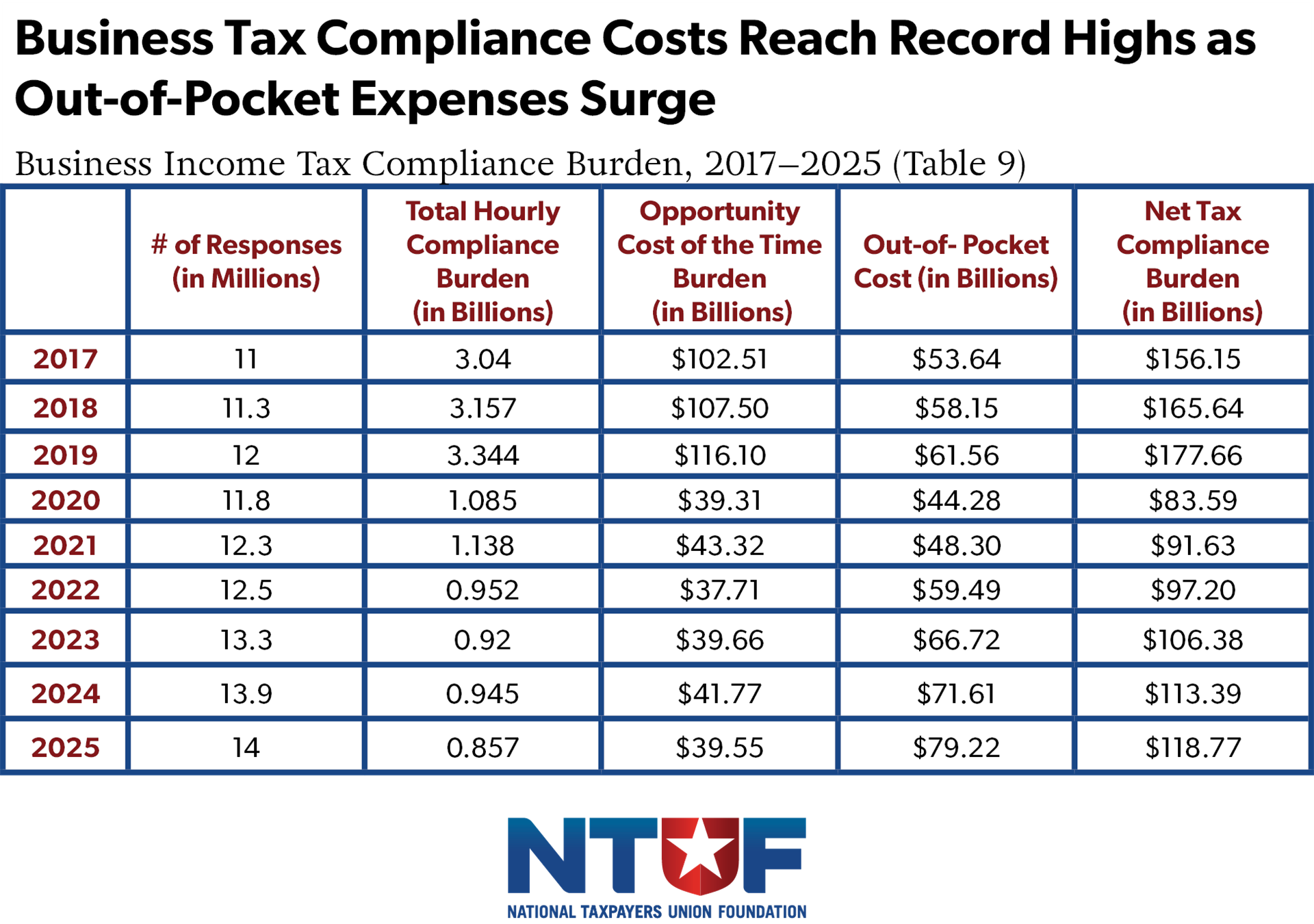

Corporations and certain partnerships are required to file business income tax returns, and the compliance burden for these filers remains substantial. As shown in Table 9, the number of business tax return respondents continues to grow, reaching approximately 14.0 million in 2025, up from 13.3 million in 2023. While this increase is consistent with a growing economy, it also reflects changes in filing patterns, expanded reporting requirements, and updates to IRS modeling assumptions.

Despite this increase in filers, the total time burden has declined in recent years, falling to 0.857 billion hours in 2025. This reduction is largely driven by updates to the IRS’s Business Taxpayer Burden Model, including revised survey data, updated filing patterns, and technical adjustments to how compliance activities are measured.

At the same time, the cost of compliance continues to rise, reaching nearly $119 billion in 2025, the highest level in the period shown. This increase is driven primarily by rising out-of-pocket costs, which have grown to more than $79 billion. The supporting statement for the business income tax indicates that IRS burden estimates show a shift from time to out-of-pocket costs, reflecting greater reliance on paid preparers, software, and specialized tax expertise.

Compliance burdens also vary significantly depending on the size of the business. IRS estimates show that, while most corporate returns are filed by smaller firms, the complexity of compliance increases sharply with firm size. Small corporations average about 40 hours and $3,900 in out-of-pocket costs per return, compared to 610 hours and more than $69,000 for large corporations with over $10 million in annual revenue.

Elements of Complexity

Length of the Tax Code and Regulations

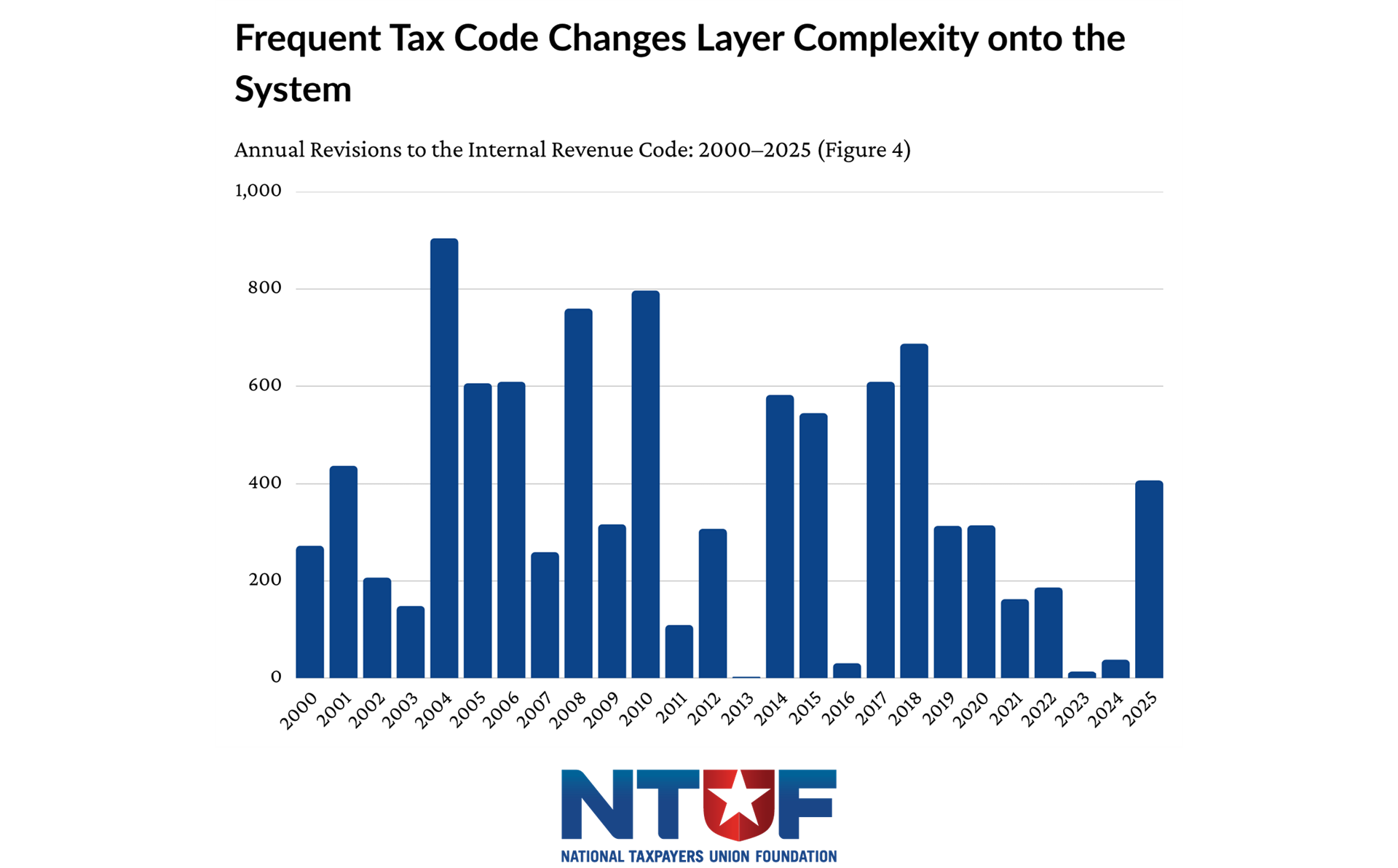

Between 2000 and 2025, Congress enacted 9,630 changes to the tax code—an average of 370 per year (see Figure 4). While many of these changes are technical or narrowly targeted, their cumulative effect can be significant. Even relatively minor revisions often introduce new definitions, thresholds, phaseouts, or reporting requirements that must be interpreted and applied by taxpayers. Over time, these incremental additions layer complexity onto the existing system, making compliance ever more time-consuming and costly.

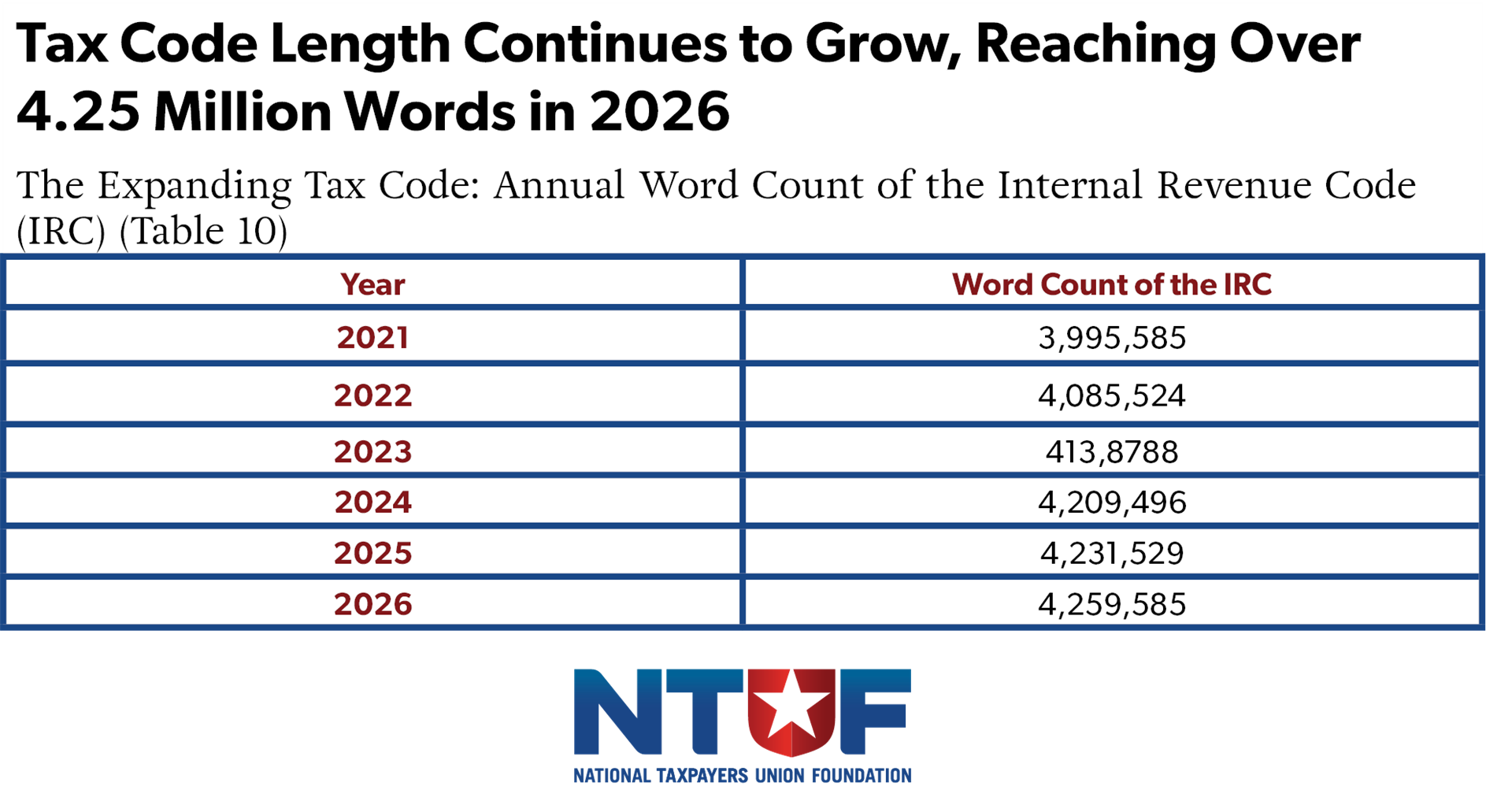

Comparing the length of the tax code over time is complicated by differences in formatting—such as layout, font, column width, and margins—which can significantly affect page counts. To ensure consistent year-to-year comparisons, NTUF uses a standardized method: the full text of the tax code is copied into Microsoft Word, and the word count tool is used to measure its length. While this method isn’t perfect—especially given the code’s numerous cross-references—it provides a consistent benchmark. This approach was also used by the Office of the Taxpayer Advocate, which estimated that, in 2017, the tax code contained 4 million words.

The TCJA temporarily reduced the tax code’s length to 3.96 million words by 2020, but that progress was short-lived. Pandemic-era tax provisions and new deductions enacted under the OBBBA pushed the total back up to roughly 4.26 million words today.

Audiobooks typically run at about 150 to 160 words per minute. At that pace, it would take roughly 19 days of continuous, 24/7 listening to get through all 4.26 million words of the Tax Code.

For the record, estimating the length of the Tax Code is no simple task. Title 26 of the U.S. Code spans more than 7,500 pages in PDF form. To convert this into Microsoft Word for a count that is consistent with previous methodology, the text is copied and pasted 500 pages at a time. Even after this process is complete, Word requires several hours to process the full document and generate a total word count.

To interpret and implement these statutes, the Department of the Treasury publishes regulations that span 22 volumes of the Code of Federal Regulations (CFR). The most recent complete edition, incorporating revisions through April 2025, includes 16,618 pages, further illustrating the scale of the tax system. Combined, the number of words in the tax code and the number of words in regulations is more than twice as high as it was in 1994.

Substandard Taxpayer Services

Complexity in the tax code is compounded by ongoing challenges in taxpayer services. While the IRS has made incremental improvements in certain areas, taxpayers continue to face uneven access to assistance across different service channels.

Telephone assistance remains the primary method of support, accounting for roughly 80% of taxpayer interactions. The IRS reported an 87% Level of Service during the 2025 filing season for its main Accounts Management line. However, this metric reflects only a subset of calls routed to the main Accounts Management line and does not include calls handled by automated systems, routed elsewhere, or dropped. As a result, it does not capture the full scope of taxpayer demand. Other lines remain significantly less accessible, with some key services answering fewer than half of incoming calls.

Even when taxpayers reach a live IRS agent, they may not receive the assistance they need. The IRS has deemed broad areas of the tax code as “out-of-scope” for assistance over the phone and at in-person clinics. This increases out-of-pocket burdens as taxpayers have few options other than turning to paid preparers or advisors.

The IRS continues to struggle with basic taxpayer correspondence, compounding its longstanding service problems. A recent Government Accountability Office report found the Service ended the 2025 filing season with a backlog inventory of 7.6 million—up from 6.8 million the year prior and far above pre-pandemic levels of around 2 million. Many involve time-sensitive issues like amended returns and identity theft claims, delaying refunds for taxpayers. Despite a 30-day response goal, nearly 4.9 million cases (64%) were late, remaining unresolved for more than 45 days.

Taken together, these challenges highlight a persistent gap between the complexity of the tax code and the IRS’s capacity to support taxpayers in navigating it. As filing requirements become more detailed and specialized, limitations in taxpayer services can increase both the time and cost required to comply.

Policy Considerations and Reform Options

Recent data show modest improvements in reported compliance burdens, but these changes are largely driven by updates to IRS modeling rather than meaningful simplification of the tax code. Policymakers therefore have an opportunity to pursue reforms that reduce both the time and financial costs of compliance.

To build momentum for simplification, lawmakers should prioritize reforms that simplify the tax code and improve transparency in tax administration. Key areas for reform include:

- Differentiate between zero and unknown costs. The Paperwork Reduction Act requires agencies to estimate compliance costs, yet many IRS forms are still reported as having zero cost when estimates are incomplete. Improving these distinctions would help identify areas in need of simplification.

- Improve accounting of out-of-pocket costs. A more complete accounting would provide a clearer picture of where compliance burdens are most significant. Greater transparency in IRS modeling similar to proposals like the Congressional Budget Office Show Your Work Act would help the IRS fulfill its PRA obligations, making it easier for policymakers to identify and address problem areas of the tax code to review for simplification.

- Improve taxpayer services and administrative capacity. The IRS must be equipped to support taxpayers effectively. Continued progress on modernization, clearer communication, fewer out-of-scope limitations on assistance, and adoption of more comprehensive service metrics would help reduce compliance burdens and improve voluntary compliance.

- Restore reporting on sources of tax complexity. Congress previously required the IRS to produce annual reports identifying sources of complexity in the tax system under the IRS Restructuring and Reform Act of 1998. Although the IRS issued only a limited number of these reports, they proved effective in prompting both legislative and administrative changes to address identified issues. Congress should require the IRS to resume regular reporting on sources of tax complexity to better inform oversight and reform efforts[19]. The recently-introduced Taxpayer Assistance and Service Act includes a provision to require the resumption of this reporting.

Conclusion

Federal tax compliance imposes substantial costs on American households and businesses, requiring billions of hours and hundreds of billions of dollars each year. While recent data show a modest decline in time burdens, these improvements are largely attributable to changes in IRS modeling and taxpayer behavior rather than a fundamental simplification of the tax code. At the same time, out-of-pocket costs continue to rise, reflecting a growing reliance on paid assistance to navigate an increasingly complex system.

However, taxpayers would have seen a large increase in compliance burdens if changes from the Tax Cuts and Jobs Act were not extended in the One Big Beautiful Bill Act of 2025. One major simplification was the near doubling of the standard deduction from $6,500 to $12,000 for single filers and from $13,000 to $24,000 for married filers. Around 30 million Americans now see a dramatically simpler tax filing experience due to this change: in 2024, 150.3 million taxpayers (90.1%) took the standard deduction while 16.4 million taxpayers itemized; prior to the TCJA, 46.5 million taxpayers (30%) itemized.

By exposing the hidden burdens of the tax code, policymakers can better target reforms that simplify filing, reduce compliance costs, and improve taxpayer services. Doing so would improve voluntary compliance by making the tax laws easier to understand and would save taxpayers a significant amount of time and money currently squandered on compliance.