(PDF) updated April 2026

In 2025, Congress locked in key provisions of the Tax Cuts and Jobs Act through the One Big Beautiful Bill Act. Yet, debates over the tax code rage on. Calls for new wealth taxes and higher rates on top earners have intensified, as the federal government continues to run chronic deficits driven by excessive spending.

Against this backdrop, the latest IRS data provides important context for evaluating claims about who pays taxes. While the federal income tax system remains highly progressive, the share of taxes paid by top earners declined modestly in 2023 from 2022.

The Inflation Reduction Act of 2022 provided the IRS with a ten-year $80 billion infusion to boost enforcement and narrow the tax gap. It does not seem that enhanced enforcement played a factor in the tax share data. The changes from 2022 to 2023 reflect economic conditions rather than structural shifts in the tax code or tax enforcement.

Even with this moderation, higher-income taxpayers continue to shoulder the vast majority of the federal income tax burden, continuing a trend in the data that NTUF has gathered going back to 1980. Even as top marginal tax rates have been reduced, the tax code has become more progressive. This fact should help ground tax policy debates regarding the distribution of income taxes amid concerns that some are not paying their “fair share.”

Tax Shares in Tax Year 2023

The IRS’s Statistics of Income division publishes annual data showing the share of taxes paid by taxpayers across ranges of Adjusted Gross Income (AGI). This information is normally released in the late fall or early winter but was delayed in 2025 because of the extended government shutdown. The newly released report covers Tax Year 2023 (for tax forms filed in 2024).

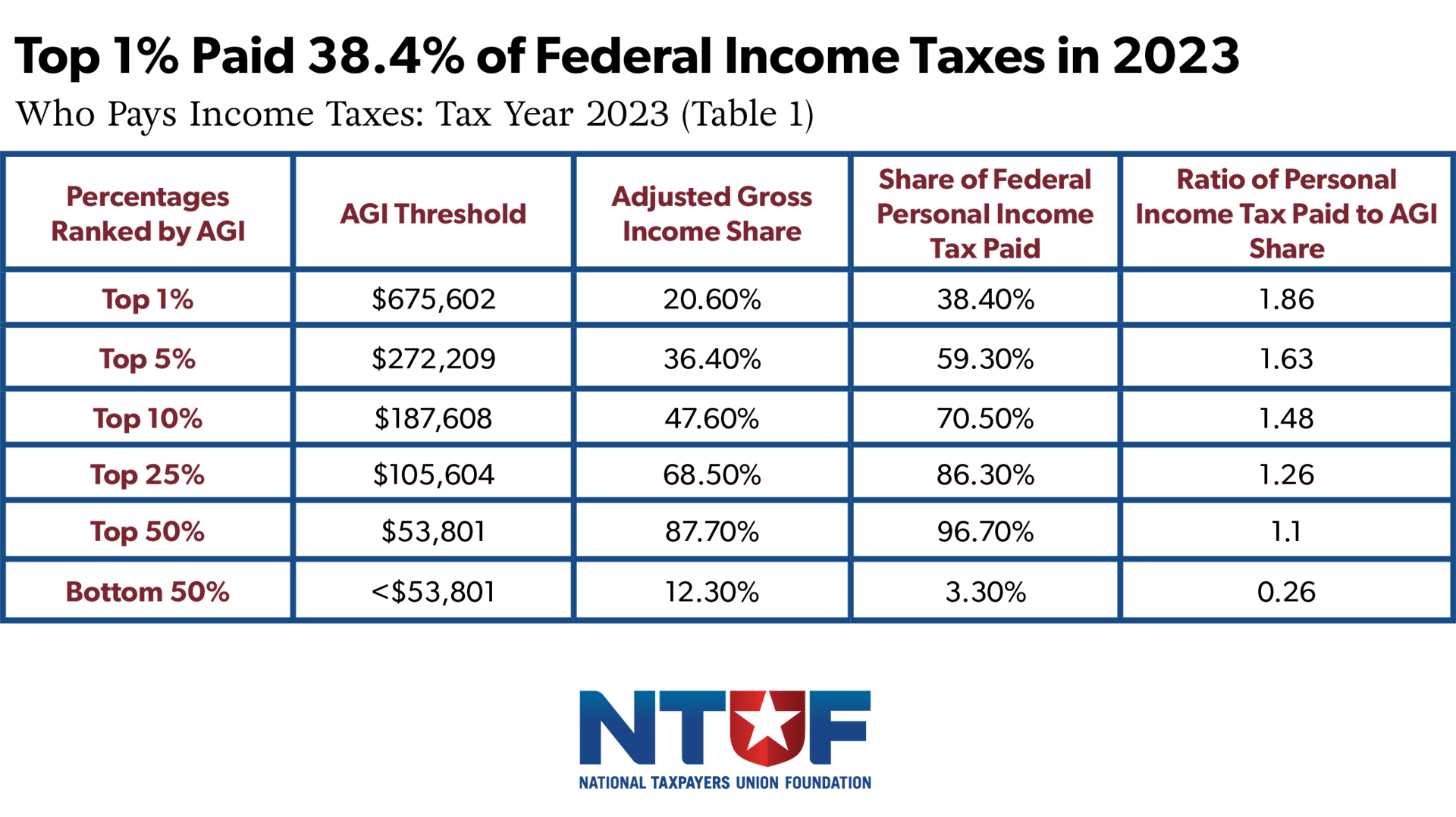

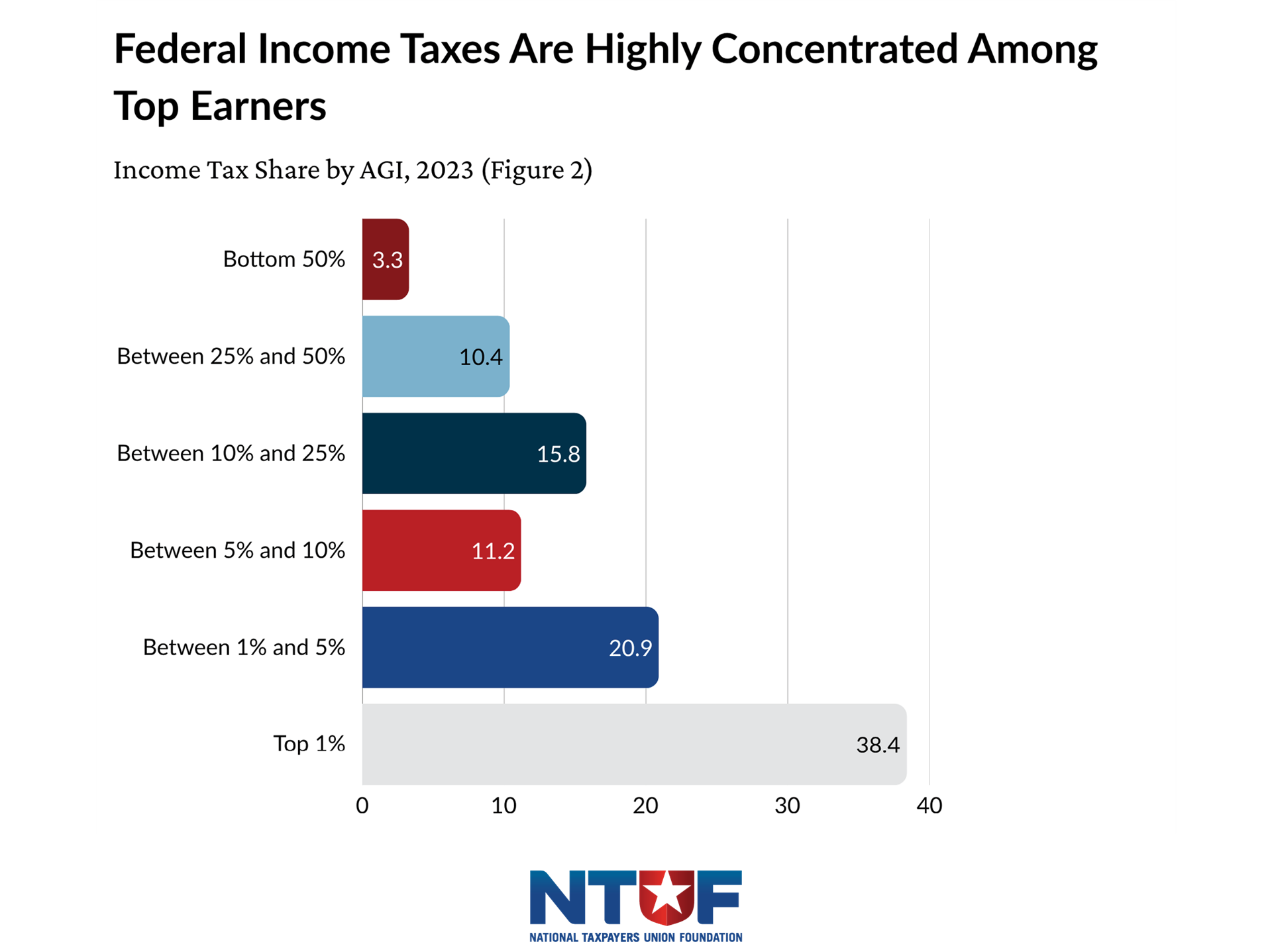

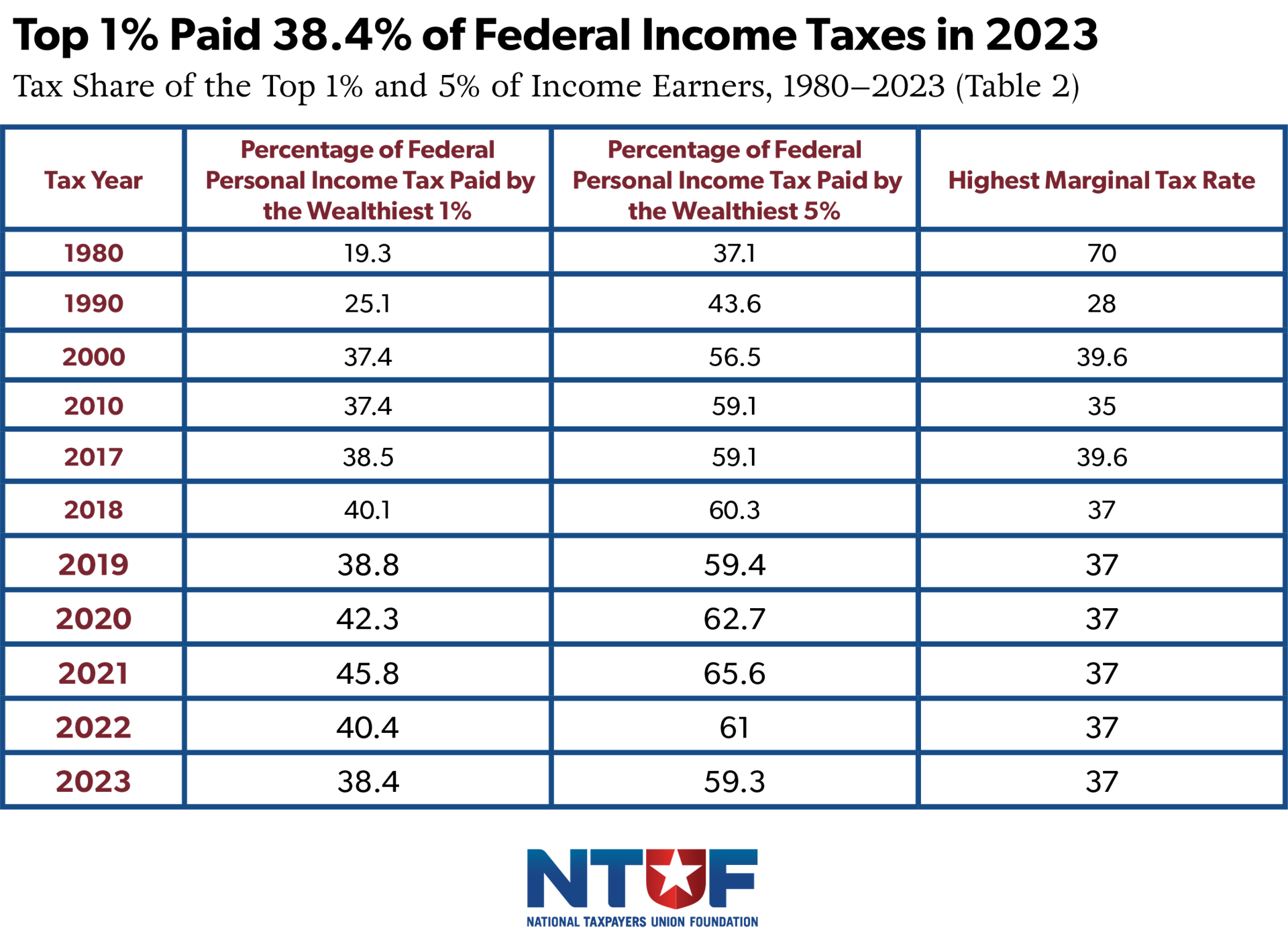

The latest data shows that the top 1% of earners—those with incomes above $675,602—paid 38.4% of all federal income taxes. This represents a modest decline from the prior year and a continued normalization from pandemic-era highs, when the top 1% paid nearly 46% of all income taxes in 2021.

This shift is largely attributable to changes in income composition, particularly, as noted by the Congressional Budget Office, a moderation in capital gains realizations following the post-pandemic surge. As investment income cooled, both the share of income and taxes attributable to top earners declined.

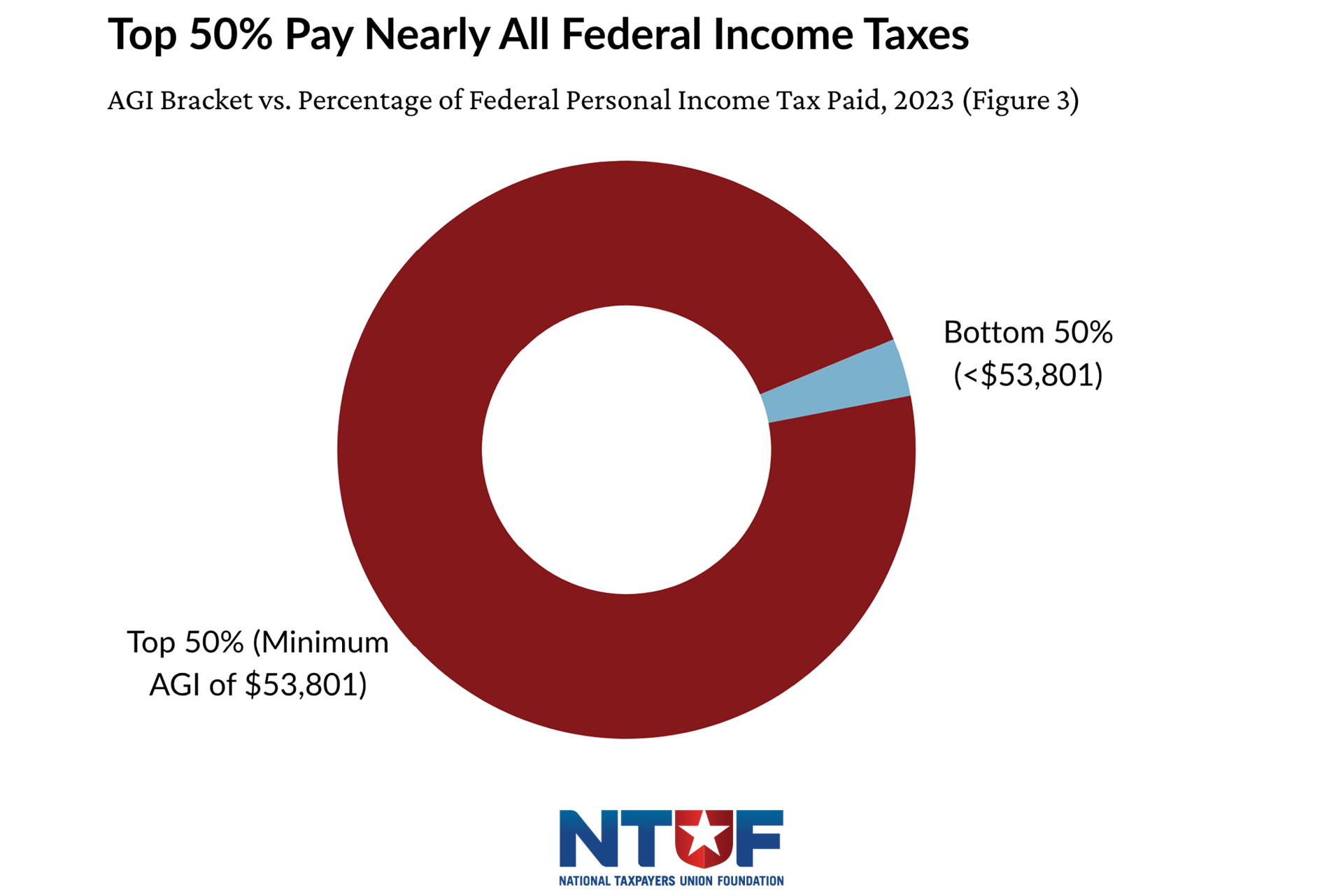

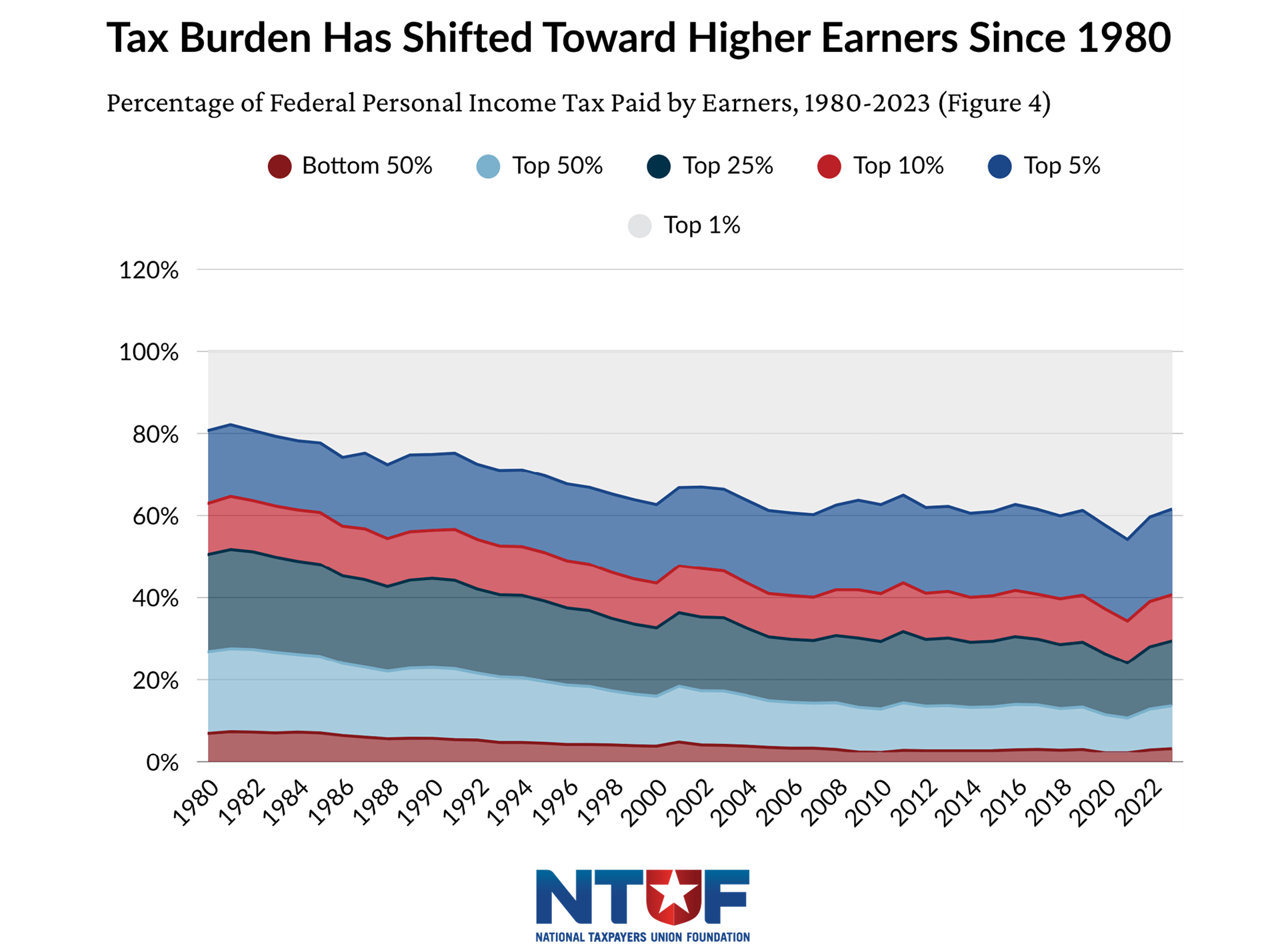

The top 10% of earners accounted for 70.5% of all income taxes paid in 2023, while the top 25% were responsible for 86.3%. Collectively, taxpayers in the top half of income brackets earned 87.7% of all income and paid 96.7% of the federal income tax burden. While these shares declined modestly from 2022, they remain near historic highs.

In contrast, the bottom 50% of earners—those with incomes below $53,801—paid just 3.3% of all federal income taxes. Many in this group owed no income tax due to earnings below the taxable threshold or eligibility for credits that offset their liability.

Separate IRS data highlights that more than 49 million tax returns in 2023 reported no income tax liability—30.5% of all returns—with 70% of these returns filed by individuals with incomes up to $50,000. This underscores the complexity of the tax system and the various factors influencing tax liability across income levels.

The ratio of personal income taxes paid to Adjusted Gross Income (AGI) provides another measure of progressivity. In 2023, the top 1% of earners, with incomes above $675,602, paid 38.4% of all federal income taxes while earning 20.6% of the nation’s AGI, a ratio of 1.86. Similarly, the top 5% earned 36.4% of AGI and paid 59.3% of income taxes, for a ratio of 1.63.

By comparison, the bottom 50% of taxpayers earned 12.3% of total AGI, but paid just 3.3% of income taxes, for a ratio of 0.26. These disparities highlight the extent to which the federal income tax system provides relief for lower income earners and places a disproportionate share of the burden on higher-income taxpayers.

Historical Tax Share Data

While there can be fluctuations from year to year based on broader economic conditions, the historical IRS data shows that the federal income tax burden has become increasingly concentrated among higher-income earners over time, even as top marginal tax rates have declined.

In 1980, the top 1% of earners paid 19.3% of all federal income taxes, while the top marginal income tax rate stood at 70%. Over the following decades, despite significant reductions in marginal rates, the share of income taxes paid by top earners steadily increased. By 2023, the top 1% paid 38.4% of all federal income taxes—twice as much as 56 years ago—while the top 5% paid 59.3%.

At the same time, the share of taxes paid by lower-income households has declined over the long term. The bottom 50% of earners paid roughly 7% of federal income taxes in 1980, compared to just over 3% in recent years. This reflects both changes in the structure of the tax code and the expansion of refundable credits.

Taken together, these trends underscore two key dynamics: the federal income tax system has become more progressive over time, and short-term fluctuations in tax shares, especially among top earners, are often driven by changes in income composition rather than shifts in tax policy.

Conclusion

The latest IRS data confirms a consistent reality: the federal income tax system remains highly progressive, with higher-income taxpayers bearing the vast majority of the burden. The modest decline in top earners’ tax share in 2023 reflects a normalization from pandemic-era highs rather than a significant structural change in the tax system.

As policymakers debate new wealth taxes and higher rates, they should start with the facts. The current system already places a disproportionate share of the burden on top earners—and even significant new taxes on the wealthy would fall far short of funding the government’s growing spending commitments. The nation’s fiscal challenges are driven primarily by decades of excessive spending, not a lack of tax progressivity.The top 10% of earners bore responsibility for 76% of all income taxes paid, and the top 25% paid 89% of all income taxes. Altogether, the top 50% of filers earned 90% of all income and were responsible for 98% of all income taxes paid in 2021.

The other half of earners, those with incomes below $46,637, collectively paid 2.3% of all income taxes in 2021. This group includes many filers with no income tax liability either because their earnings fell below the taxable threshold or due to eligibility for tax credits that effectively reduce or eliminate income tax liability. Separate IRS data highlights that over 56 million tax returns in 2021 reported no income tax liability, with 93% of these returns filed by individuals with incomes less than $50,000. This underscores the complexity of the tax system and the various factors influencing tax liability across income levels.