(pdf)

Who Pays International Corporate Taxes?

U.S. corporations with foreign subsidiaries they control (controlled foreign corporations, or CFCs) pay taxes on 1) subpart F income and 2) Global Intangible Low-Taxed Income (GILTI)

More on the difference between the two below

- The IRS lacks public, post-TCJA data on the total number of U.S. CFCs, but in tax year 2016 reported there were 16,225 U.S. corporation returns with 95,374 CFCs

There were 6.6 million total U.S. corporations in the same year (2016; note the vast majority of those were S corporations), so only a tiny fraction (0.2%) of U.S. corporations have CFCs

An even smaller portion of U.S. corporations paid taxes on GILTI in 2018, the first year GILTI was in effect; according to IRS data from tax year 2018, there were 9,127 U.S. parent corporations with 83,632 CFCs that had GILTI

What’s Subpart F Income, What’s GILTI Income, and What’s the Difference?

Joshua Ashman and Nathan Mintz of Expat Tax Professionals LLC wrote a helpful shorthand on the main difference between subpart F and GILTI in The Tax Adviser:

“The most fundamental distinction between the definitions of Subpart F income and GILTI is this — Subpart F income is defined initially by what it includes, while GILTI is defined initially by what it excludes.”

Subpart F income is mostly passive income earned by a U.S. CFC, including (but not limited to):

- Dividend, interest, royalty, rent, and annuity income

- Commodities transaction income

- Foreign currency gains

- Income from issuing or reinsuring insurance contracts

- Certain foreign base company sales and service income, if the income is derived from sales or services made to a related party (i.e., parties controlled by the same business)

GILTI is intended to represent U.S. CFC earnings from highly-mobile, highly-profitable intangible assets (such as “goodwill, contracts, formulas, licenses, patents, registered trademarks, franchises, covenants not to compete”); GILTI does so by:

- Having corporations calculate net CFC income across all foreign subsidiaries, after excluding 1) income “effectively connected” to the conduct of a trade or business, 2) subpart F income, 3) certain highly-taxed income, 4) dividends from related persons, and 5) foreign oil and gas extraction income (FOGEI); and then

- Subjecting any remaining net CFC income to GILTI taxation, after exempting 10% of the value of the CFC’s share of tangible property (the qualified business asset investment, or QBAI, substance-based carveout)

For more, see this JCT explainer

What is the Tax Rate?

Subpart F income is taxed at regular U.S. rates (21% for C corporations, and up to 37% for S corporation shareholders passing through business income to their individual return), after accounting for foreign tax credits

GILTI is taxed at preferential U.S. rates (between 10.5% and 13.125%) until 2025, and will be taxed at higher, but still preferential, U.S. rates (between 13.125% and 16.4%) after 2025

This preferential rate is achieved by allowing a 50% deduction on GILTI relative to the statutory U.S. corporate tax rate (21%)

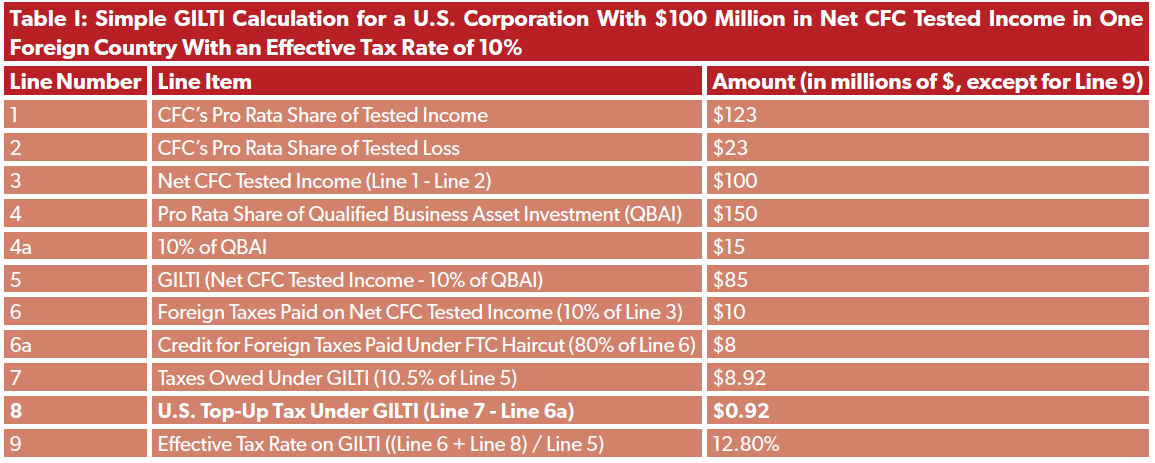

The below chart demonstrates how GILTI might work for a U.S. corporation with a subsidiary in one country with a 10% effective tax rate (below GILTI minimum); we assume the corporation has $100 million in net CFC tested income:

Under this simple calculation, a U.S. CFC with $100 million in net income (in a foreign country with a 10% corporate tax rate) would pay an additional $920,000 to the U.S. in top-up taxes

Because the U.S. only credits 80% of foreign taxes paid under GILTI (the so-called foreign tax credit, or FTC, haircut), the effective tax rate of the U.S. CFC actually ends up being 2.3 percentage points higher than the GILTI minimum - 12.8%

In other words, this corporation with $85 million in GILTI is paying $2.3 million more in taxes as a result of the FTC haircut

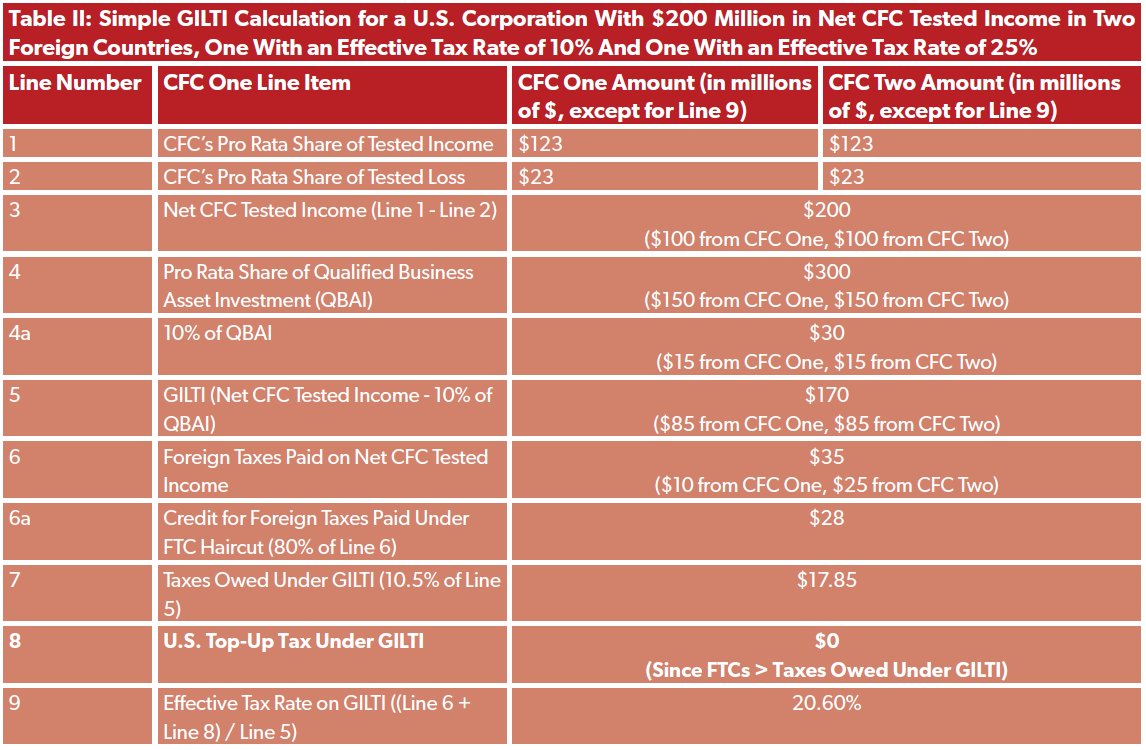

In practice, U.S. corporations with multiple CFCs across the world have the opportunity to blend their foreign taxes paid, meaning obligations in a high-tax country can offset GILTI liabilities in a low-tax country

Table II illustrates this dynamic with a simple calculation, for a U.S. corporation with two CFCs, each with $100 million in net CFC tested income; one CFC pays an effective tax rate of 10% on their $100 million in net income, but the other CFC pays an effective tax rate of 25% on their $100 million in net income:

- This corporation would not owe any top-up U.S. tax on GILTI, since the combined foreign tax obligations of the corporation on its two controlled subsidiaries exceeds the 10.5% GITLI minimum (even after accounting for the FTC haircut)

For simplicity’s sake, the above tables omit additional calculations a corporation must make relative to complex expense allocation rules; in practice, this limits the use of FTCs even further and raises GILTI liability; see a helpful explainer from Tax Foundation here

What is the FDII Deduction?

TCJA also provided a 37.5% deduction for U.S. companies’ income derived from exports but attributable to U.S.-based intangible assets (the foreign-derived intangible income, or FDII, deduction)

- The 37.5% deduction means, in practice, that companies pay an effective tax rate of 13.125% on FDII (21% - (37.5% * 21%))

- The 37.5% deduction is reduced to 21.875% starting in 2026, meaning the effective tax rate on FDII will rise from 13.125% to 16.4%

JCT estimated in December 2017 that the deduction would reduce tax revenues by $63.8 billion over a decade

In tax year 2018, 4,018 corporate tax returns reported $143.3 billion in FDII

3,909 of those corporations (97.2%) took FDII deductions, totaling $52.5 billion

How Much Does the Government Collect in International Corporate Taxes?

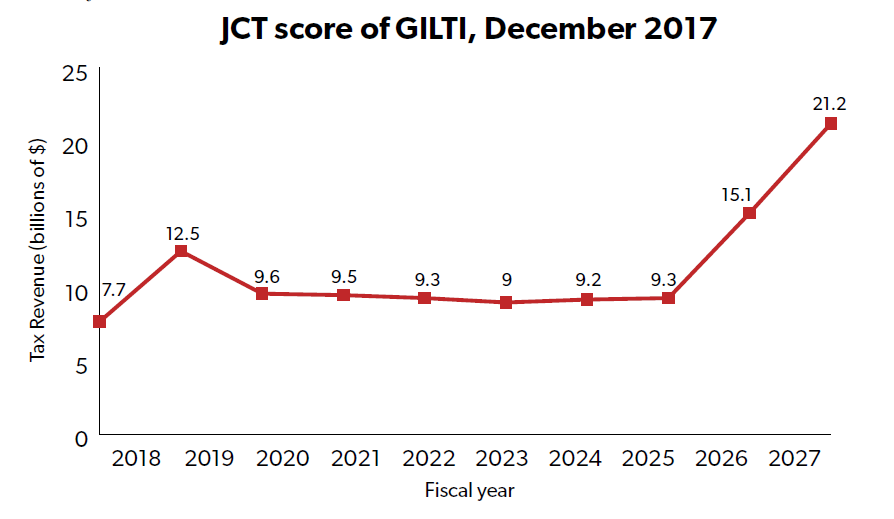

When TCJA passed in 2017, the Joint Committee on Taxation estimated that GILTI would raise tax revenues by $112.4 billion over a decade, since GILTI was a new tax being introduced

The chart below demonstrates the year-by-year impact; the annual impact begins to rise sharply in fiscal year (FY) 2026 in part because, after calendar year 2025, the GILTI rate is effectively raised (from 10.5%-13.125% to 13.125%-16.4%)

What Are the Biden Administration Proposals Affecting International Taxes?

President Biden has proposed major changes to the international tax regime in the Treasury Department’s FY 2022 Green Book, including:

- Doubling the GILTI rate, from 10.5%-13.125% to 21%-26.25%

- Repealing the QBAI substance-based carve-out

- Requiring companies to calculate GILTI liability on a country-by-country basis, rather than allowing them to blend foreign taxes owed and paid on a global basis

- Repealing FDII

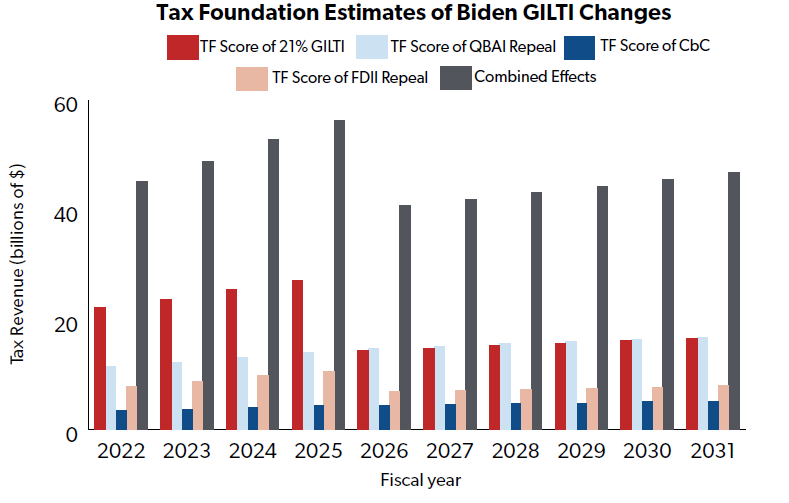

Tax Foundation modeled these proposals and found they would increase taxes on GILTI significantly, by $466.4 billion over a decade

The below chart shows Tax Foundation’s scores for President Biden’s GILTI and FDII changes

Note: Tax Foundation estimates revenue increases relative to a baseline; i.e., a $37.4 billion tax increase in FY 2022 means GILTI taxes are $37.4 billion higher than they are relative to a baseline (not $37.4 billion total)

What Are the Wyden Proposals Affecting International Taxes?

Senate Finance Committee Chair Ron Wyden has proposed several changes to the international tax regime, including:

- Raising the GILTI rate to an unspecified amount

- Repealing the QBAI substance-based carve-out

- Requiring companies to calculate GILTI liability on a country-by-country basis, rather than allowing them to blend foreign taxes owed and paid on a global basis, but excluding highly-taxed income from GILTI

- Possibly repealing the FTC haircut, but possibly maintaining an FTC haircut up to 20% (the current law amount)

- Replacing FDII with a new deduction, foreign derived innovation income, which shifts the focus of FDII from the returns on U.S.-based intangible income to the returns on U.S.-based R&D and working training expenses

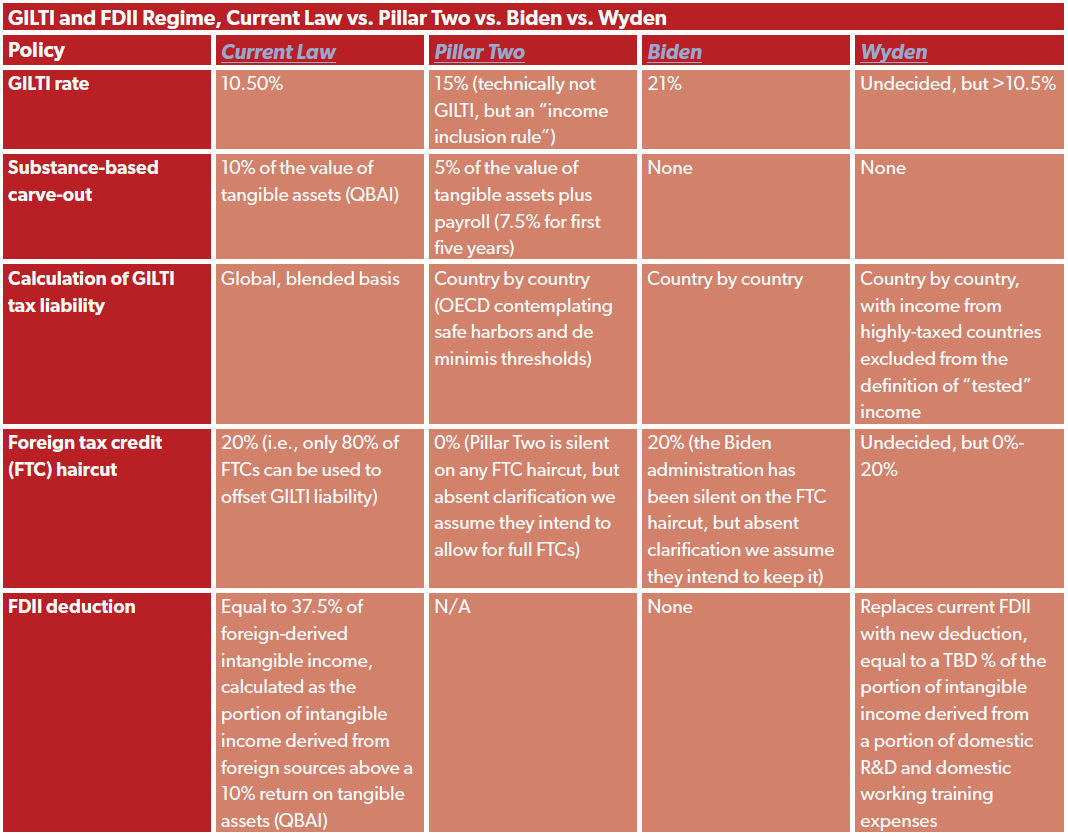

A chart below summarizes the differences between the Biden and Wyden proposals, along with a current-law summary of various provisions and what the global tax agreement (“Pillar Two”) has envisioned for certain policies