Energy policy is increasingly becoming one of the most important drivers of economic competitiveness in the United States. As artificial intelligence, cloud computing, and digital infrastructure expand, the demand for reliable electricity is rising rapidly. Data centers, which power much of the modern digital economy, require consistent energy supplies. The states that can provide reliable, affordable electricity while maintaining competitive tax and regulatory environments will be best positioned to attract investment in this growing sector.

For Nebraska, this reality presents both a challenge and an opportunity. The state is already beginning to see the effects of this transformation. Electricity demand is rising, and projections show that electricity consumption will increase further in the coming years. Meeting this demand will require careful planning, reliable generation resources, and policies that encourage investment in both energy infrastructure and the broader economy.

At the same time, Nebraska faces broader economic pressures that make these decisions even more important. The state is losing population, particularly among college graduates and young professionals who are choosing to pursue opportunities elsewhere. Retirees are increasingly priced out by rising property taxes. Businesses evaluating where to invest often look for locations with strong labor markets, competitive tax environments, and reliable infrastructure. When those conditions are lacking, investment flows elsewhere.

These trends create a difficult cycle. With fewer people contributing to the tax base, the cost of maintaining roads, bridges, and other infrastructure must be spread across a smaller population. Government services cannot easily scale down alongside population declines, placing upward pressure on taxes and accelerating outmigration.

Breaking this cycle requires policies that empower economic growth through investment, innovation, and opportunity. Nebraska must create an environment that attracts businesses, expands employment opportunities, and encourages workers to build their careers in the state.

The Platte Institute works to support that transformation. As Nebraska’s leading free-market policy organization, the Platte Institute provides rigorous research, strategic communications, coalition building, and legislative expertise to equip policymakers with solutions that strengthen the state’s economic competitiveness. In recent years, these efforts have helped support major policy reforms, including the largest income tax reduction in state history, property tax reform measures, and regulatory reforms designed to improve the state’s economic climate.

These reforms mark an important step forward, but reversing the state’s population and workforce challenges will require continued policy leadership. Nebraska’s regional competitors are already making decisions designed to attract both talent and capital.

The growth of data centers and digital infrastructure represents one of the most promising opportunities for economic expansion. These facilities bring significant capital investment, support high-paying jobs, and generate substantial local tax revenue. At the same time, their expansion reinforces the importance of energy policy. The electricity required to power the digital economy will shape economic development decisions for years to come.

Nebraska’s policy choices today will determine whether the state captures these opportunities or falls behind competitors that are moving quickly to support the infrastructure needed for the next generation of economic growth.

The Midwest’s Emerging Role in the Data Center Economy

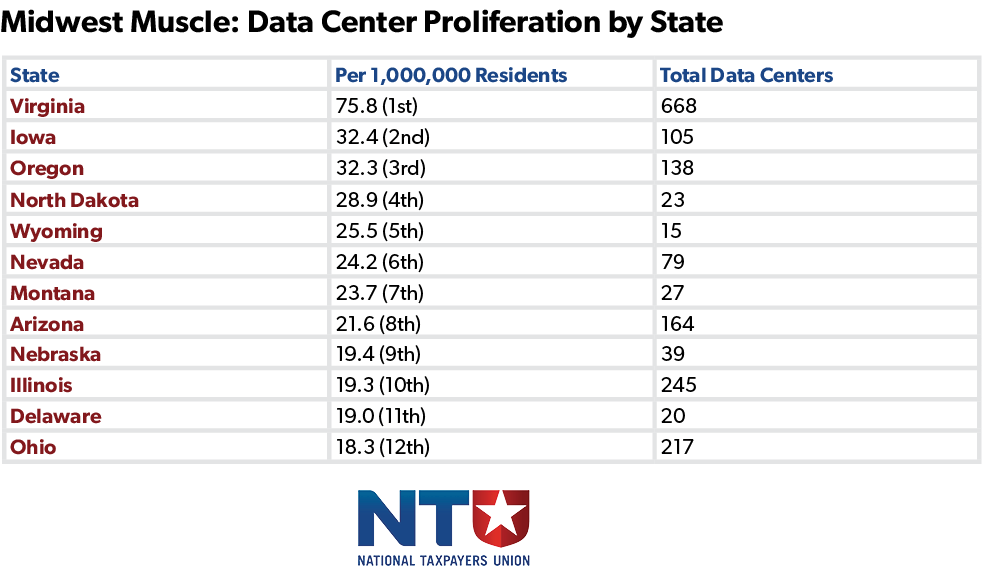

The Midwest grows many things—including, increasingly, data centers. That’s good news, generating substantial local tax revenue, creating high-paying jobs, and expanding economic opportunities.

With 39 data centers (about 19 per 1 million people), Nebraska punches above its weight nationally, while trailing neighboring Iowa, which boasts the second-highest number of data centers per capita at 32 per 1 million people (105 total data centers). Illinois and Ohio have also emerged as competitive markets for data center projects, with these four midwestern states all ranking among the top twelve for data centers per capita.

Economic Benefits of Data Center Development

Data center jobs pay quite well, but the real impact is in indirect employment. Data centers are constantly reinvesting due to the industry’s rapid pace of change, and that capital investment creates jobs for local contractors, suppliers, and construction workers. Data centers can also serve as anchors for broader tech ecosystems, with tech companies expanding operations near large “hyperscale” operations. Colocation facilities, meanwhile, build out the capacity necessary to support local technology businesses.

A 2022 NetChoice study concluded that a single $750 million hyperscale data center would support 1,290 jobs and generate $269 million in economic output during construction, with ongoing direct employment of 100 people and indirect employment of 200 more, driving $82 million a year in additional economic output. Nebraska’s 39 data centers include $4.4 billion in capital investment by Alphabet (Google) alone, and another $1.5 billion or more from Meta (Facebook). The NetChoice study projected that, by 2035, data centers could contribute $4.8 billion to Nebraska’s economy, supporting over 14,000 jobs with $1.1 billion in compensation. These data center investments also contribute substantially to local tax revenues, while the additional economic activity they create boosts both state and local coffers.

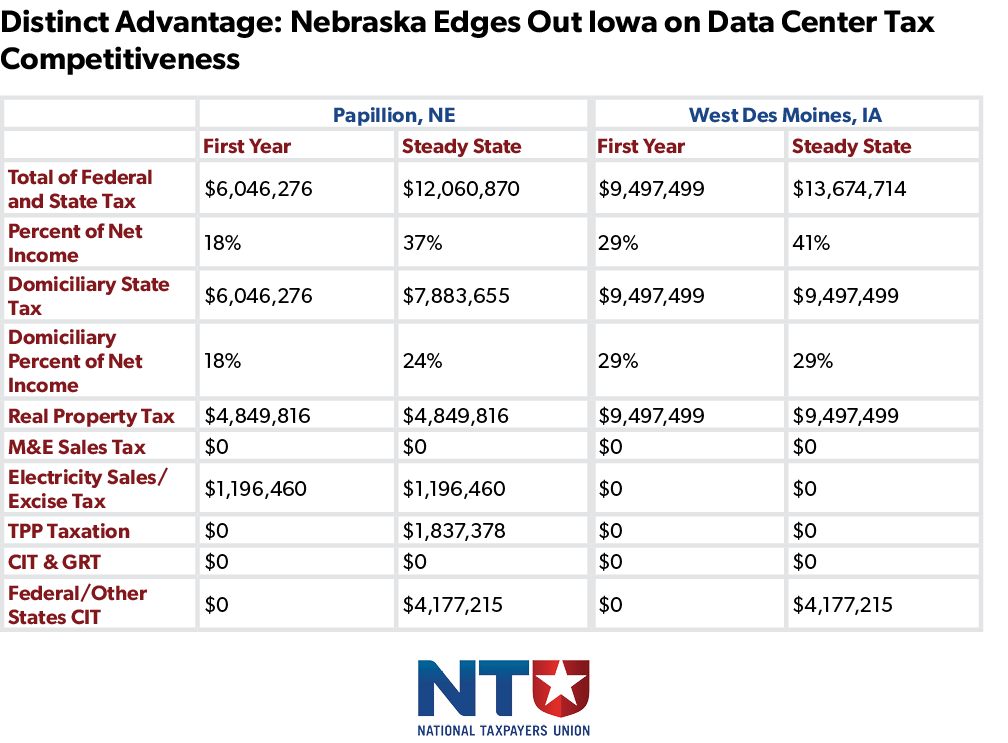

But the continued growth of Nebraska’s burgeoning tech sector is not guaranteed. A recent Tax Foundation analysis calculated state and local tax liability for data centers in twelve jurisdictions across the country, including Papillion, Nebraska. A $1 billion data center in Papillion faces about $7.9 million in state and local tax liability on about $33 million in net revenue, for an effective tax rate of 24%. This is among the lowest burdens in the study, after Charlotte, North Carolina (12%) and Cheyenne, Wyoming (21%). Neighboring Iowa was not included in the Tax Foundation analysis, but a data center in West Des Moines would face an estimated $9.5 million in state and local tax liability (29%), higher than Nebraska’s rates, but still sufficiently competitive to attract substantial investment, particularly from Microsoft. One reason for West Des Moines’ possible allure is that there is no tax on tangible personal property.

Maintaining a Competitive and Principled Tax Environment

The proper tax treatment of data centers is no different from that of any other type of business. Property taxes should be limited to real property (land and structures), not business tangible personal property (machinery and equipment). Sales tax should only apply to final transactions, not intermediate purchases (business inputs).

Nebraska, like most states, (including neighboring Iowa) exempts purchases of servers and other data center equipment from its sales tax. Nebraska’s exemption is available through the quality jobs investment and mega-project tracks under the ImagiNENebraska incentives program. The incentives program can also provide investment and wage tax credits. Nebraska initially exempts servers and other machinery and equipment from tangible personal property (TPP) tax as a further ImagiNE incentive, but taxes such equipment for mature operations. Iowa, by contrast, exempts TPP from tax in perpetuity. However, Iowa classifies certain fixtures as real property whereas Nebraska treats them as tangible property, somewhat eroding the benefit of Iowa’s policy.

Iowa also exempts data centers’ electricity purchases from its sales tax, saving a $1 billion data center an estimated $1.3 million per year, while Nebraska subjects data center utilities to sales taxation. Lower property values and lower property tax rates, however, yield lower overall tax burdens in Papillion, Nebraska compared to West Des Moines, Iowa.

With cool weather, low utility costs, a central location along the I-80 fiber corridor, and low tax burdens, both Nebraska and Iowa are poised to attract more data centers in the future. Nebraska has chipped away at Iowa’s head start with a competitive tax environment that has proven a boon not only to the state’s economy but also to local revenues. According to Tax Foundation estimates, $1 billion in data center capital investment in Papillion yields about $7 million in local tax revenue each year on $33 million in profits, an impressive local return.

With the right tax choices, Nebraska can continue attracting data centers, creating new jobs, expanding the local tech sector, and providing a valuable new source of local tax revenue. Maintaining Nebraska’s competitive edge deserves to be a policy priority.

Energy Demand and the Digital Economy

While tax competitiveness plays an important role in attracting data centers, energy policy is increasingly becoming the defining issue for future growth. The rapid expansion of artificial intelligence and digital services is driving a dramatic increase in electricity demand across the country.

In Nebraska, data centers already represent a growing share of electricity consumption. For the Omaha Public Power District, data centers accounted for approximately 1% of electricity demand in 2018. By 2035, that share is projected to increase to approximately 41%.

This surge in electricity demand is not limited to data centers alone. Other industries are also increasing energy consumption, including agricultural processing facilities, fertilizer production, ethanol plants, and sustainable aviation fuel manufacturing. Cryptocurrency operations have also emerged as significant electricity consumers.

Taken together, these developments are creating unprecedented expansion prospects for electricity supply systems.

Rising Energy Costs and Infrastructure Pressures

At the same time that electricity demand is increasing, energy costs are also rising.

Nebraska residents are already experiencing rate increases from major utilities. Omaha Public Power District customers are expected to face approximately 6% increases in electricity rates in 2026, while Nebraska Public Power District customers may see increases of up to 3%.

However, these increases are largely driven by rising costs for critical infrastructure inputs, including steel, copper, and labor.

Policymakers have begun exploring legislation aimed at addressing these cost pressures and ensuring that large electricity consumers contribute appropriately to infrastructure investments.

Legislation such as LB1111 and LB1064 seeks to ensure that major electricity users cover the infrastructure costs associated with their demand rather than shifting those costs onto residential ratepayers.

These policy discussions reflect broader concerns about fairness, affordability, and the sustainability of Nebraska’s energy system.

Grid Reliability and Generation Policy

Ensuring reliable electricity supply is another major policy challenge. Several legislative proposals introduced during Nebraska’s 2026 session address concerns about the availability of dispatchable generation resources.

Dispatchable generation refers to power sources that can be turned on and off as needed to meet demand.

LB1026 seeks to prevent utilities from closing functional power generation facilities during periods of high demand. The bill is particularly focused on delaying the retirement of coal-fired generation plants until sufficient replacement capacity is available.

Another proposal, LB1172, would require minimum portfolio standards for dispatchable generation to ensure adequate system reliability.

These proposals reflect growing concerns about maintaining reliable electricity supply as demand increases.

Nebraska’s Unique Public Power Structure

Nebraska’s electricity system operates under a unique governance model. Unlike every other state in the country, Nebraska relies entirely on public power utilities.

This means that most energy solutions are driven by local control and non-profit mandates rather than statewide regulatory commissions. This structure has several key impacts on how energy is developed and managed.

First, Nebraska does not have a statewide renewable portfolio standard or mandatory energy efficiency goals. Instead, decisions about energy generation and efficiency programs are made by individual utility boards. Three of Nebraska’s largest utilities (Nebraska Public Power District, Omaha Public Power District, and Lincoln Electrical System) have voluntarily adopted long-term carbon reduction goals, including net-zero emissions targets between 2040 and 2050.

Second, regulatory authority is delegated to locally elected or appointed boards rather than a state-level Public Service Commission. This structure can create challenges when long-term planning decisions are influenced by political considerations.

Third, by law, public power districts must practice Integrated Resource Planning, which requires evaluating the “least-cost” options for reliable service. Utilities must file these plans with the Nebraska Power Review Board, but the Board has no power to deny or amend them. This results in a diverse energy mix, but can lead to inconsistent adoption of new technologies across the state.

Policy Pathways for Reliable and Affordable Energy

Meaningful and lasting solutions to Nebraska’s energy availability and affordability challenges must recognize the uniqueness of the state’s public power model but also be willing to make the bold changes necessary to protect our economic future.

First, standards must be set to ensure that dispatchable generation remains an adequate portion of Nebraska’s electricity portfolio. Maintaining reliable baseload generation capacity will be critical as electricity demand increases.

Second, utilities should reconsider efforts to retire dispatchable, baseload power plants that were based on self-imposed net-zero emission standards adopted by public power boards. Such action could include adoption of LB1026-type legislation.

Third, restrictions on privately-owned power generation, including both behind-the-meter and front-of-the-meter generation projects, should be relaxed. Expanding these options could encourage new investments in energy supply.

Fourth, considering that utilities do not unilaterally decide which of their power plants to run—rather relying on a centralized Southwest Power Pool (SPP) market system that determines the most efficient and reliable mix of generation—further study and action is needed to ensure that the need for greater dispatchable generation is reflected in the collaborative relationship between SPP and Nebraska’s public power utilities.

Fifth, there should be a review of decision-making policies of the state’s regulatory agencies and public utilities, along with recommended changes that ensure experienced and informed regulators engage in critical decisions affecting the long-term reliability of Nebraska’s power grid.

Lastly, Nebraska must create greater transparency in the operational decision-making process that drives power-supply and price-setting practices.

Conclusion

Nebraska stands at an important crossroads. The growth of the digital economy presents a major opportunity for the state. Data centers and technology infrastructure investments can support economic growth, generate tax revenue, and create jobs.

At the same time, these opportunities bring new policy challenges related to electricity demand, infrastructure investment, and energy reliability. Nebraska’s unique public power system adds additional complexity to these policy discussions.

Meeting these challenges will require thoughtful policymaking that empowers economic growth through reliable and affordable energy for residents and businesses.

If Nebraska maintains competitive tax policies, supports responsible energy development, and strengthens the reliability of its electricity system, the state can position itself as a leading destination for data center investment.

Doing so will help attract new businesses, create new jobs, and expand the state’s economic base.

Ultimately, these policies are not just about technology infrastructure or energy generation. They are about creating the conditions necessary for Nebraska to compete, grow, and retain the people and businesses that will shape its future.

Acting now to support investment and innovation will help ensure that Nebraska preserves what makes the state special while building a stronger economic future.

Jim Smith is Chief Strategy Officer and Jared Walczak is Senior Tax Policy Advisor for the Platte Institute.