(pdf)

American agriculture is one of the most subsidized industries in the world, and these subsidies are frequently subject to criticism from deficit hawks, free trade advocates, and environmentalists. The network of government programs to support farmers is complex, and this primer will work to explain the Farm Safety Net in detail, analyze its effectiveness, and propose reforms to make the program more effective at supporting family farms. NTU concludes that government subsidies for crop insurance are the most worrisome aspect of current farm policy, and that the current structure of commodity subsidies are, at best, ambivalently effective at keeping the traditional family farm secure. Perhaps most importantly, we call for a goals-oriented discussion of the objectives of the Farm Safety Net, so that debates over policy details are in service of the same end goal.

Part I: Understanding the Farm Safety Net

The Farm Safety Net refers to a collection of federal programs designed to keep agricultural producers from experiencing economic hardship. It has three primary legs: 1) the perennial Farm Bill, 2) ad hoc legislative action, and 3) emergency executive action. We discuss each of these in detail below.

The Farm Bill

The Farm Bill is by far the most important of the three legs in the safety net. It is the authorizing piece of legislation for most of the activities of the U.S. Department of Agriculture (USDA), and it typically is renewed every five years (although Congress sometimes fails to meet that deadline). By and large, federal farm policy is set by the Farm Bill, and it can change drastically between two consecutive Farm Bill packages. The Farm Bill also sets nutrition policy (including the Supplemental Nutrition Access Program, or SNAP), which is fulfilled by the USDA. The most recent Farm Bill, passed in 2018, was officially titled the “Agriculture Improvement Act of 2018.” Billions of dollars are directed to help farmers through Farm Bill programs, but unfortunately, these programs are far from effective at spending taxpayer dollars wisely to help small family farms.

Title I of the Farm Bill authorizes direct subsidies for certain commodities. There are usually more than a dozen “Title I commodities”, but the largest recipients are the “big five”: corn, soybeans, wheat, rice, and cotton (cotton is separated into two categories, short staple and extra long staple). Title I includes disaster payments for crops and livestock as well. The Farm Bill also authorizes subsidies for crop insurance for over 100 types of crops in Title XI. The insurance subsidy is significant, often over 60 percent of the premium. The title also authorizes conservation programs, which provide financial incentives for farmers to adopt specific conservation practices. These three titles, along with the Nutrition title, account for the vast majority of Farm Bill spending. Other farm programs in the bill include favorable-interest rate loans for producers, rural development programs, and research support.

Emergency Actions

On top of disaster payments, guaranteed direct subsidies, and subsidized insurance, Congress also regularly uses emergency legislative action to send money to farmers when natural disasters occur. Most recently, Congress approved $13 billion in support for agriculture in the 2021 Consolidated Appropriations Act, and a total of $23.5 billion for agricultural support in the CARES Act.[1] For context, the total value of USDA farm subsidies is usually around $15 billion.

The executive branch will also approve ad hoc aid for agricultural producers. The most recent example of this is the Market Facilitation Program (MFP), which sent $28 billion directly to farmers impacted by Chinese tariffs. MFP will be discussed in more detail below.

Part II: Digging into the Data

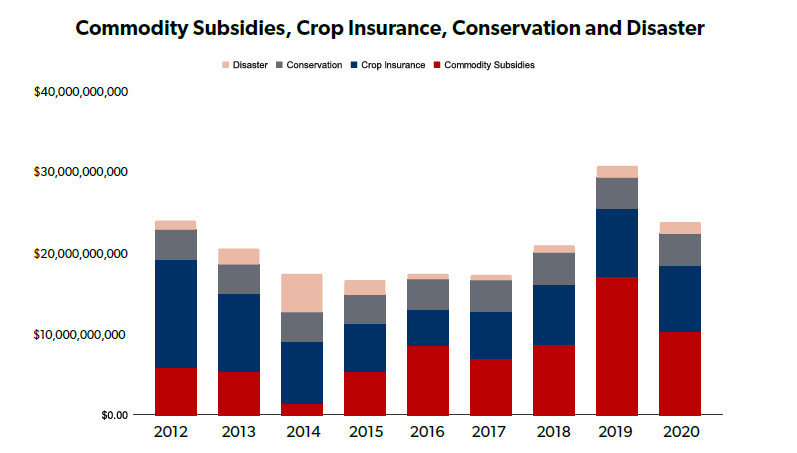

This graphic visualizes the relative size of Farm Bill producer support vehicles:[2]

The 2008 Farm Bill made crop insurance subsidies a more central component of the farm safety net, whereas commodity subsidies had previously been the centerpiece. The sharp rise in commodity subsidies in 2019 is a result of the Trump administration’s temporary Market Facilitation Program (more on MFP below). Each of these four pieces are important, but the focus of this primer will be on commodity subsidies and the crop insurance subsidy.

Commodity Subsidies

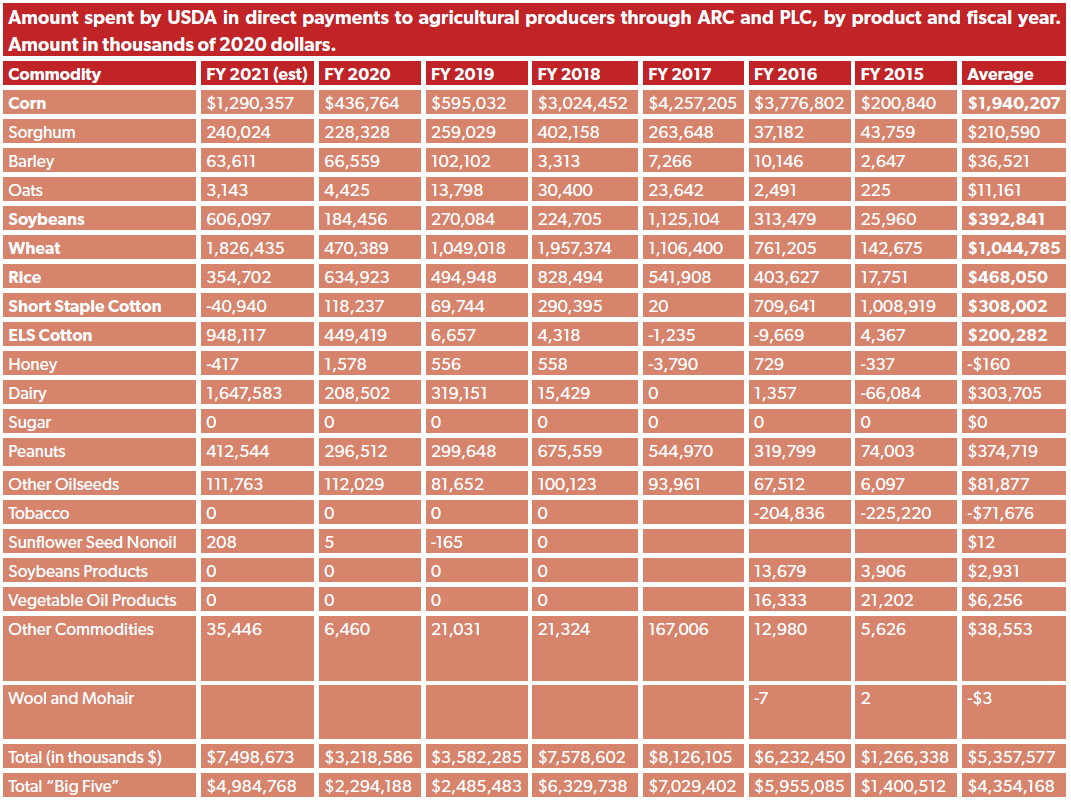

Under Title I direct subsidies, USDA has spent between $1 billion and $9 billion per year since FY 2015, which averages to more than $5 billion annually. (Title I does not include MFP). On average, over 80 percent of that sum is directed towards the “big five” program commodities (corn, soybeans, wheat, rice, and cotton). These direct subsidies are provided through twin programs, Agricultural Risk Coverage (ARC) and Price Loss Coverage (PLC). ARC is a “shallow loss” program, designed to pay out in low-income years where crop insurance indemnities are not triggered. PLC pays out when the price of a commodity falls below a certain target, so as to guarantee a minimum price for the producer.

Information obtained from Commodity Credit Corporation (CCC) Budget explanatory notes for FY2015-FY2022, available on USDA website.[3]

Disaster Subsidies and Conservation Programs

Title I Disaster spending is largely directed at livestock and dairy farmers. CBO estimates that for FYs 2021-2031, disaster spending will be between $400 million and $600 million per year, for a total of $5 billion over the next ten years.[4]

Conservation programs are generally subject to less criticism and scrutiny than other components of the Farm Safety Net. Even pundits who are generally skeptical of Farm Bill initiatives are generally supportive of its conservation efforts, especially with a growing body of evidence that conservation efforts make farmers more financially resilient.[5] In fact, the largest criticism of USDA conservation programs is that other USDA spending programs (namely crop insurance) work counter to conservation goals. Total conservation spending is usually about $5 billion annually.[6] For the purpose of this primer, environmental initiatives are outside the scope of our examination of market-based farm policy.

Crop Insurance

The single largest Farm Bill program to help producers is Title XI Crop Insurance. Before diving into the numbers, a word on the structure of this program. The Federal Crop Insurance Corporation (FCIC), which is wholly a subsidiary of the USDA, does not sell crop insurance outright. Rather, it manages the marketplace for crop insurance policies, which are sold by approved private companies (of which there are 13, including the American Farm Bureau, AIG, and AgriSompo).[7] Crop insurance policies indemnify the policyholder in the event of low revenue, which could be a result of low yields, low prices, or both. Low yields can happen after disasters, years of soil degradation, poor decision making during planting season, or sheer bad luck.

How does a revenue insurance policy work? Agriculture is the only industry with such a product, so it is worth investigating. In order for revenue insurance to be profitable for the insurance company, premiums must be very steep. The market price of revenue insurance would be so steep, in fact, that almost no farmer would be willing to buy it. This is why the federal government offers such generous subsidies for crop insurance. Without the federal subsidy, the crop insurance industry would be unrecognizably different. The crop insurance subsidy has three components to keep crop insurance companies viable.

The first component is the premium subsidy. Farmers do not pay anywhere close to the full premium for crop insurance. In fact, the government usually pays close to 66 percent of the premium.[8] Crop insurance companies also receive overhead subsidies from the government: much of their payroll and operating expenses are paid for by the taxpayers. On top of that, if a specific crop’s policy causes significant losses for the insurance company, the government will underwrite it to ensure the company’s bottom line isn’t too heavily impacted.[9]

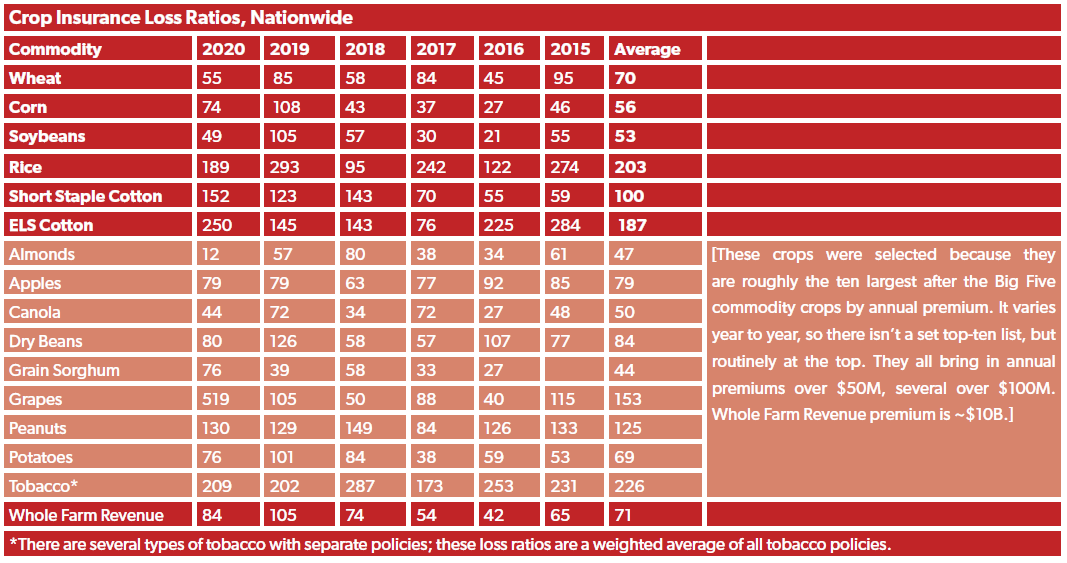

At first, it is hard to comprehend how such a set up could even exist: crop insurance companies sell a miracle product (guaranteed revenue for their policyholders) that the government ensures their customers can afford, the government pays for the majority of their operating expenses, and if they ever experience major losses, the government will pick up the tab. It sounds incredibly advantageous to be a crop insurance company. However, a look at the insurance loss ratios for crop insurance will make the picture a bit clearer:[10

Crop insurance policies simply are not profitable. Insurance loss ratios are a measure of total indemnification over total premiums collected. Private insurance companies can usually sustain a maximum loss ratio of 60 percent to stay profitable; 40 percent is usually considered a good target. Most crop insurance policies have loss ratios well over 60 percent, some regularly breaking 100 percent or even 200 percent.[11] For example, rice policies have had an average loss ratio of 203 percent over the past five years. That means insurance companies pay out twice as much in rice indemnities than they bring in from rice premiums (including the subsidized portion of the premium). In a free marketplace this simply would not stand and premiums would rise or the policy would be dropped entirely. However, the federal government ensures that these policies stay available by propping up crop insurance companies with $9 billion a year in Title XI subsidies.

A note on sugar and dairy: These two commodities receive special treatment in the Farm Bill. Dairy is supported with Dairy Margin Coverage, which pays producers when the difference between the price of milk and the price of feed gets too small. Producers are entitled to the minimum “catastrophic” coverage, but can pay a higher premium for more coverage.[12] Dairy producers also benefit from import quotas that restrict the amount of foreign dairy in U.S. markets. Sugar producers do not receive direct payments from the government, but are supported indirectly through import quotas, processor price guarantees, and domestic marketing allotments. This results in essentially $0 in federal outlays for sugar producers, because domestic consumers bear the cost. The U.S. reports sugar protection to the WTO at a value of $1.4 billion[13] and multiple candy manufacturers have cited high U.S. sugar prices as the primary reason for moving their factories overseas.[14] Though they are not included in the larger subsidy programs in the Farm Bill, dairy and sugar are two of the most subsidized industries in the United States.

Commodity Credit Corporation (CCC)

In addition to Farm Bill spending, the Commodity Credit Corporation (CCC) has access to funding. The CCC is authorized to borrow up to $30 billion per year from the Treasury, and the Farm Bill ensures that they will be reimbursed for their “net realized losses” every year; effectively, the CCC is granted $30 billion per year they do not have to repay.[15] The CCC has no staff, and is wholly controlled by the USDA as a financing institution. They must pay ARC and PLC recipients from their $30 billion pool, but after those are paid out (almost always less than $10 billion), they are authorized to spend the remaining $30 billion as they see fit. This makes the CCC a brazen USDA slush fund that has been taken advantage of by the Obama administration to help a Senate campaign[16] and to skillfully avoid spending restrictions from Congress,[17] and by the Trump administration’s Market Facilitation Program (MFP).

MFP, known colloquially as Trade Aid, was an ad hoc executive program to send money to farmers. When American agricultural producers were experiencing significant decreases in demand as a result of the trade dispute with China, USDA Secretary Sonny Perdue used CCC funding to send money directly to farmers in both 2018 and 2019. The first round impacted only corn, soybeans, wheat, cotton, sorghum, hogs, dairy, almonds, and cherries; the second round added rice, peanuts, lentils, peas, alfalfa, dried beans, chickpeas, tree nuts, grapes, cranberries, and ginseng. Soybeans and cotton were the most heavily subsidized crops, accounting for roughly 75% of MFP payments.[18] The total cost of the program was $28 billion.

All of this “emergency” CCC spending was on top of ARC and PLC payments, crop insurance payouts, and disaster protections. As the Congressional Research Service identified, “MFP payments do not count against other 2018 farm bill payment limitations. There are no criteria in place to calculate whether MFP might duplicate losses covered under revenue support programs such as the Agricultural Risk Coverage (ARC) and Price Loss Coverage (PLC) programs of the 2018 farm bill. As a result, the same program acres that are eligible for ARC or PLC payments may be eligible for MFP payments.”[19]

Congress will also routinely pass emergency legislation to provide financial assistance to farmers, especially after a natural disaster. In response to hurricanes from 2017-2019, Congress sent out $5.4 billion over three bills. This is odd because those impacted were already covered by crop insurance and Farm Bill disaster relief, and it is concerning because it sets the precedent that Congress is supposed to appropriate emergency funds after every natural disaster -- a bad budgetary habit Farm Bill disaster relief was supposed to prevent. The most recent bout of ad hoc legislative aid came from the CARES Act and the 2021 Consolidated Appropriations Act, with a total of $36 billion between the two.

Part III: Analyzing Farm Aid

ARC and PLC

Exploring the effects of this farm aid leads to some surprising results. Let’s first cover commodity subsidies, ARC and PLC. PLC is a fairly standard price support. When the price producers receive is below a reference price, producers are paid 85 percent of the difference between the two. ARC is a bit more complicated. It is a revenue guarantee tied to historical revenue. ARC creates a benchmark revenue for a farm (determined by the five-year Olympic Average[20] yield times the five-year Olympic Average price for the county) and guarantees producers 86 percent of that benchmark. When a producer’s revenue is below the guarantee, they are paid the difference -- ARC guarantees a minimum revenue based on historic revenue.[21]

But where is this money flowing to? Politicians tend to sell Farm Bill subsidies as support for the idyllic, small family farm. Data on actual recipients, however, would paint a different picture. There are 2.1 million farms in the United States, and only 39 percent of them receive commodity or insurance subsidies.[22] Specific to commodity subsidies (ARC and PLC, and their predecessors), the top 10 percent of payment recipients were paid 78 percent of commodity payments from 1995 to 2020, and the top 1 percent of recipients collected 26 percent of payments.[23] That means the top 1 percent received an average of $2.6 billion per year from ARC and PLC, or $1.9 million apiece. The federal government is directly funnelling billions of dollars every year to the largest farms in the country, under the guise of protecting small farmers.

Some of the recipients of agricultural subsidies are particularly eyebrow-raising. EWG’s Robert Coleman identified fifty members of the Forbes 400 list who received farm subsidies.[24] OpenTheBooks reported that 6,618 entities received more than $1 million in federal farm subsidies from 2008-2018, with the highest earner (Concordia Allied Producers of Georgia) bringing home $23.8 million in federal subsidies.[25]

An excellent report from AEI analyzed subsidy recipients by farm sales decile.[26] They found that the top 20 percent of farms (by total sales revenue) received 82 percent of total ARC, PLC, and crop insurance subsidy payments. Fewer than 15 percent of farms in the bottom 40 percent and fewer than half of farms in the bottom 70 percent were recipients of any subsidy. In short, they concluded that “the data indicate that producers who receive the majority of total ARC and PLC programs and crop insurance subsidy payments also own the largest farms, generate the highest crop sales revenues, and have the highest amounts of wealth.”

ARC and PLC subsidies largely do not even flow to small producers. Large farms are more strategically organized to cash in on these subsidies, and repeatedly do. This has an adverse effect on the longevity of small producers. As extra money is funnelled to large farms, they are bolstered and grow even larger. The extra cash they receive from the government supports large farmers as they outbid small farmers when land comes up for rent or for sale. That slows the ability of small farms to thrive, consolidates agriculture in fewer and fewer hands, and leaves fewer people in the rural communities these subsidies purport to protect.[27] The way farm subsidies are currently structured may actually hurt the idyllic family farm more than they help it.

What is the market impact of these subsidies? Let’s start with the basics. Large subsidies for the “Big Five” commodities lead to more farmers choosing to grow one of those commodities than the market would otherwise demand. And this makes economic sense for a typical farmer -- why would you not take advantage of guaranteed price minimums? This trend is perhaps most evident with corn: even as we mandate the use of ethanol in gasoline so as to force a market for corn, corn acreage has been steadily rising since 1990.[28] More farmers growing corn means there is a larger supply of corn on the market -- which helps keep prices low. This makes the subsidy appear even more necessary as farmers become more reliant on federal dollars to make ends meet.

Crop Insurance Subsidies

In addition to ARC and PLC, which are dominated by the Big Five commodities, almost every crop is eligible for crop insurance subsidies. Sen. Debbie Stabenow, Chair of the Senate Agriculture Committee, liked to say of crop insurance that farmers receive “a bill, not a check”[29], embodying the pervasive idea that the Farm Safety Net is just a little bit of well-deserved support for a hard-pressed, humble family farm. An investigation into crop insurance cash flows, however, will demonstrate the extent to which large farms truly benefit from the program.

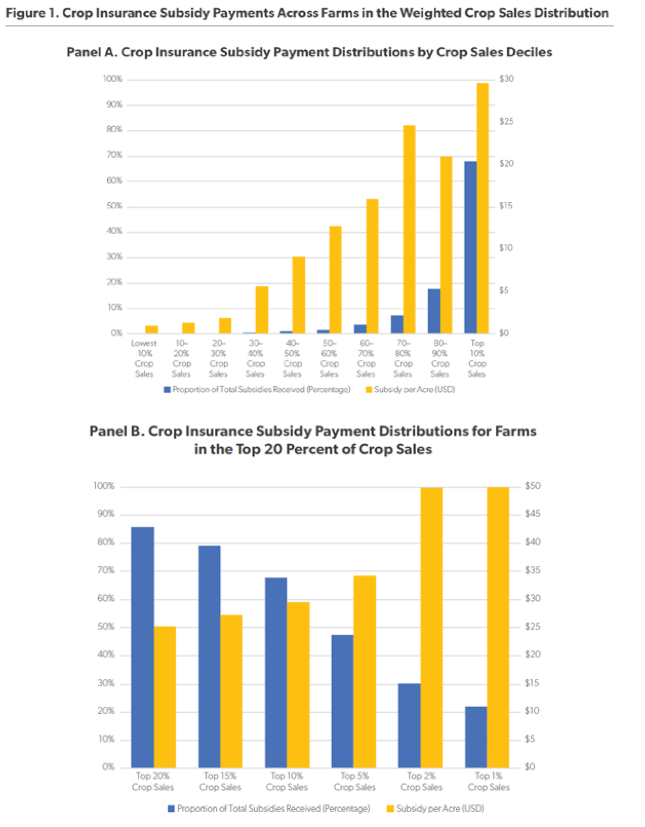

Here is a chart from the AEI article cited above:

The chart sorts farmers into deciles by total crop sales revenue, and then shows the average crop insurance subsidy per acre for each of these deciles. It is clear that farms with higher sales are more subsidized than smaller farms with lower sales. The bottom 90 percent of farms receive roughly 20 percent of the value of crop insurance subsidies. Whereas farms with the lowest 50 percent of sales save on average less than $10 per acre, farms with the highest 2 percent of sales save roughly five times as much. This is no coincidence. Large farms know how to game the system to squeeze every penny out of the federal government, and there are not currently caps on how much an individual farmer can benefit from the program. There aren’t eligibility requirements either. Crop insurance subsidy recipients are anonymous; however, GAO was able to identify at least four recipients with a net worth over $1.5 billion.[30]

What is the impact of crop insurance? It encourages farmers to plant as much as possible. Even if the planted crop fails, as long as it was covered by insurance, the farmer will get paid for it. Farmers thus have an increased incentive to plant as much as possible, by planting in or near wetlands or tilling an area that was previously forested. This creates an increase in demand for seed, which pushes up seed prices, an extra expense for all farmers. Crop insurance is effectively revenue insurance. It eliminates built-in incentives to reduce risk and therefore, encourages very risky behavior.

There is a significant negative environmental impact associated with the current crop insurance structure. It disincentivizes sustainable farming practices, like letting a field lie fallow, and encourages farmers to plant in areas that aren’t likely to succeed, like wetlands.[31] Crop insurance pays farmers to degrade wetlands by planting crops that aren’t even likely to make it to market. Why lawmakers who claim to support the environment or free markets continue to support this program is baffling. Crop insurance policies don’t even regularly give discounts to farmers who adopt policies that make crop failure less likely, like planting cover crops.[32] This system leads to soil degradation, overproduction, and government deficit spending.

Part IV: Proposals for Reform

Crop Insurance

How well has the Federal Crop Insurance Program worked? Quite frankly, it is a blatant failure. It sucks billions of dollars per year from the federal budget to create a backwards incentive structure for farmers. It is bad for the environment and sends large sums of money to massive farms.

Farm policy is shielded from much of the typical Republican vs. Democrat fighting that other issue areas are subject to. Instead, farm policy tends to be a regional battle, especially between the corn- and soybean-heavy Midwest and the rice- and cotton-heavy South. ARC and PLC were created as twin programs so that one could be designed with Southern farmers in mind (PLC), and the other with Midwestern farmers in mind (ARC). As for crop insurance, the clear victor is the South.

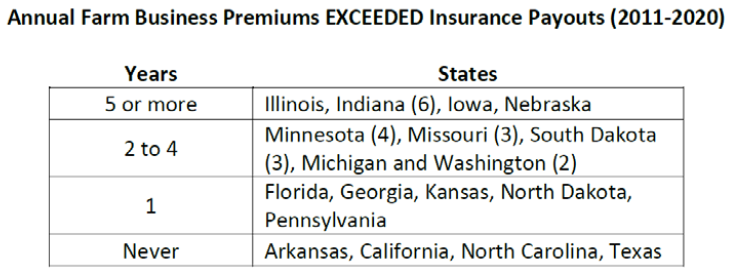

The largest Midwestern crops, corn and soybeans, have average insurance loss ratios of 56 and 53 percent,[33] respectively, whereas the primarily southern crops of rice, upland cotton, and pima cotton have average loss ratios of 203, 100, and 187 percent. This means that corn and soybeans policies are fairly profitable for crop insurance companies (they pay out 53-56 cents in indemnities for every $1 they bring in in premiums), but rice and cotton policies trigger more in indemnities than they collect in premiums. Here is a chart made by Taxpayers for Common Sense that illustrates this point:[34]

The disparity between Corn Belt states and Southern states is remarkable. Far from being an efficient and effective safety net, the Federal Crop Insurance Program is a nonsensical web that favors producers in one region of the country (the South) over others.

Thinking about the future of crop insurance, then, two questions stand out. 1) Should the program be reformed or simply repealed? 2) If the former, what reforms should lawmakers pursue? Let’s discuss both of these broad options:

Outright Repeal. It is conceivable that if the federal government simply eliminated the crop insurance subsidy, a completely private crop insurance market would appear -- one with discounts for sustainable practices, online sales, and coverage for yields, not revenues. This would be ideal. If the goal of farm policy is to help small farmers, the federal government could provide a subsidy to low-income producers to make crop insurance more affordable, without subsidizing the industry writ large. This would be a much smaller burden on the taxpayer and make for a much more efficient insurance market.

One wonders why crop insurance and disaster relief packages exist simultaneously -- the need for disaster bailouts seems to imply that the insurance coverage is ineffective.[35] Perhaps the best way to support agricultural producers is largely outside of the crop insurance market -- as was done before 2008. To arrive at a solid conclusion about the best structure of the Farm Safety Net, we first need to arrive at an agreement about its goals -- more on that below.

If lawmakers aren’t bold enough to repeal the crop insurance program outright, they should at least reform it. Here are our best proposals for reform:

Insuring Yields, not Revenues. As it stands, crop insurance policies do not insure crops -- they insure revenue for the policyholder. That is unheard of outside of the agricultural industry, because it is less of an insurance policy than it is a welfare program. If the federal government is going to pay billions of dollars to ensure that farm revenue doesn’t tank, then that should be the sum total of the Farm Safety Net, not a partial component. To make crop insurance a sensible program, it should be the total yield that is insured, completely separate from the market price of the crop.

Rewards for Sustainable Practices. Earlier, we discussed the notable lack of incentives for sustainable farming. This is perhaps the most obvious fix to the crop insurance program, because not only does it accomplish the sustainability goal, it mirrors structures that are common in many non-crop insurance policies. If you quit smoking, you can get a discount on your life insurance, because you are less likely to file a claim. In the same way, if you plant cover crops, you are less likely to file a crop insurance claim. Crop insurance companies should be encouraging cover crops with financial incentives. It makes sense for them from a business strategy standpoint, and it is environmentally friendly. The same should be true for letting fields lie fallow, avoiding planting in wetlands, maintaining forested areas, and much more. These practices are good for the soil, the farmer, and crop insurance companies[36] -- why crop insurance policies continue to disincentivize them is baffling. The Risk Management Agency manages the marketplace and exerts significant control over crop insurance companies, and it should loosen the restrictions on crop insurance policy structures, so that crop insurance companies are able to offer smart, sustainable policies with better incentives.

Indemnity Caps. If the goal of crop insurance is to support small farmers specifically, then it is worth considering limits on how much a policyholder can be indemnified. For example, a cotton farmer in Texas was indemnified over $4 million dollars -- and the premium for that policy was $250,000 paid by the farmer and $834,000 paid by the government.[37] That is an incredible indemnity, more than the total annual revenue of the vast majority of farms. If the government is going to gift billions of dollars annually to support small farmers, then it ought to ensure that those dollars actually go to small farmers.

The authors of the AEI article cited above recommend a cap of $40,000 on the value of the insurance subsidy any individual farmer receives. They find that this would save the federal government $2 billion annually (around 40 percent of the cost of the program), and would only impact five percent of recipients.

Online Sale of Crop Insurance. It is currently impossible to purchase crop insurance online; you must speak to an insurance agent to purchase crop insurance. USDA tried to implement an online purchasing tool, but the pilot program was scrapped under pressure from stakeholders.[38] The removal of the pilot was an example of unnecessary protectionism, and lawmakers should consider requiring the USDA to follow through on a new version of the pilot.

Commodity Credit Corporation

Crop insurance is not the only USDA program in need of reform. The Commodity Credit Corporation (CCC) is a brazen slush fund that has repeatedly been taken advantage of. It is guaranteed access to $30 billion per year that it does not have to repay. Worse yet, this funding is mandatory, not discretionary. The CCC funding mechanism was established in 1948 and remains unchanged, with permanent indefinite authority to borrow from the Treasury, which Congress reimburses them for in the annual USDA appropriations bill. This should be radically restructured. CCC spending should certainly not be mandatory, and its permanent borrowing authority should be repealed outright. Rather than paying off CCC’s tab on the back end, Congress should appropriate the CCC funds for the upcoming fiscal year, the same way it does for nearly every other federal program. This will push lawmakers to discuss why the CCC needs access to such a large amount of Treasury funds, rather than simply accepting the amount they’ve already spent. In other words, the CCC should be asking for permission to spend, not forgiveness. This will make the CCC more accountable and hopefully more financially responsible.

As an example of the unaccountability of the CCC, let’s evaluate the Trump Administration’s Market Facilitation Program (MFP). This program was conceived to make the trade war easier to swallow -- not to do what was right for producers and the agricultural industry overall. ARC and PLC already existed and were designed to help producers when prices fall, and crop insurance guaranteed that those producers would receive indemnities if their revenue was still too low. Nonetheless, USDA approved $28 billion in direct checks -- $28 billion that Congress was unable to exercise oversight on. This is not how a government of checks and balances is supposed to work, and Congress needs to take back its power of the purse by reforming CCC funding.

Commodity Subsidies

ARC and PLC are not as dysfunctional as crop insurance. However, they still have their flaws, most notably the way they are taken advantage of by wealthy individuals. These subsidies are meant to provide stability for farmers without significant liquid assets, but many massive farms with owners who reside in big cities are able to receive funding. To combat this problem, ARC and PLC recipients should be more thoroughly means-tested. Here are some strategies:

Realign AGI Requirements. To be eligible for ARC and PLC payments, recipients must currently have an AGI below $900,000 annually, or double that amount for married couples.[39] That is an extraordinarily high number. These programs are supposed to help farms stay afloat in rough years; families with a $1.8 million AGI do not typically need government help to stay afloat. The current system also neglects the source of income; the 2008 Farm Bill divided its AGI maximum into “farm income” and “nonfarm income” categories, while the 2014 and 2018 Farm Bills did not do so. We recommend bringing this distinction back, with a $100,000 AGI limit for each category, double that amount for married couples. This would tailor ARC and PLC payments to farmers who do not have high enough liquid incomes to stay afloat over a few bad years.

Tighten Actively Engaged in Farming (AEF) Requirements. According to the nonpartisan Congressional Research Service (CRS):

“To be eligible for ARC and PLC under the 2018 farm bill, An individual producer must meet three AEF criteria:

- The person, independently and separately, makes a significant contribution to the farming operation of (a) capital, equipment, or land; and (b) active personal labor, active personal management, or a combination of active personal labor and management.

- The person’s share of profits or losses is commensurate with his/her contribution to the farming operation.

- The person shares in the risk of loss from the farming operation

In general, family farms receive special treatment whereby every adult member (i.e., 18 years or older) is deemed to meet the AEF requirements. Family membership is based on lineal ascendants or descendants but is also extended to siblings and spouses. Furthermore, under the 2018 farm bill (§1703), for purposes of assessing the availability of individual payment limits, the definition of family member has been extended to include first cousins, nieces, and nephews.” [40]

This is one way folks can take advantage of ARC and PLC. Payment limits are pushed way above a reasonable limit as numerous family members are counted as “actively engaged in farming,” even if they only visit the farm once per year. These restrictions should be tightened. Specifically, the cousins, nieces, and nephews clause should be removed (and never should have been added to the 2018 bill). Active physical engagement in farm labor for at least three months should be required, not just “personal management”.[41] To prevent folks who live in New York City or Washington, DC full-time from receiving farm subsidies, a near-the-farm residency requirement should be considered.[42] With tighter AEF requirements, ARC and PLC payment limits will hopefully only be raised when another person is genuinely actively involved in farming.

Means-testing is effective at targeting eligibility, but it doesn’t impact the structure of the program itself. The question remains whether the federal government should offer direct subsidies at all, or switch to a different safety net structure. Price supports just incentivize more production, which keeps prices down and makes producers dependent on subsidies. However, without any Farm Safety Net, many small producers would be forced to close their doors concurrently after one or two bad years. To have a productive discussion about structural changes, we need to first decide on the goals of the Farm Safety Net writ large.

Conclusion

The Farm Safety Net is a complex web of poorly designed subsidies and ad hoc aid. The Federal Crop Insurance Program is a blatant failure, the CCC Fund is a much-abused slush fund, and USDA commodity subsidies disproportionately help the largest farms. These programs would benefit greatly from reform. At a minimum, the crop insurance program should be wholly restructured, the CCC Fund should undergo the normal appropriations process, and commodity subsidies should have tighter eligibility requirements.

Before an effective replacement for the safety net can be conceived, the ultimate goal of the safety net must be established. If policymakers’ goal is to preserve the idyllic “family” farm, then subsidies are not the correct approach. Simply instituting price supports is swimming against the economic current, without doing anything to change the structural forces that have made it difficult for small farmers in the first place. Negotiations over the next Farm Bill ought to begin with a goals-oriented discussion among policymakers, and their conclusions should be explicitly stated. This will provide a platform against which to measure the success of the Farm Bill, and will inform the process of coordinating the program to be as effective as possible.

Special Thanks to Josh Sewell at Taxpayers for Common Sense and Nan Swift at R Street Institute for their research assistance.

[1] Newton, John. “What’s in the CARES Act for Food and Agriculture.” American Farm Bureau, March 26, 2020. Retrieved from:

https://www.fb.org/market-intel/whats-in-the-cares-act-for-food-and-agriculture; and Newton, John et. al. “What’s in the COVID-19 Relief Package for Agriculture?” American Farm Bureau, December 22, 2020. Retrieved from: https://www.fb.org/market-intel/whats-in-the-new-covid-19-relief-package-for-agriculture. It is worth noting that the $23.5B is the sum of $9.5B for the Office of the Secretary and $14B supplemental for the CCC Fund.

[2] Data on commodity subsidies, disaster, and conservation aid retrieved from: https://data.ers.usda.gov/reports.aspx?ID=17833; data on crop insurance retrieved from https://www.rma.usda.gov/-/media/RMA/AboutRMA/Program-Budget/19cygovcost.ashx?la=en and https://www.usda.gov/sites/default/files/documents/usda-fy20-agency-financial-report.pdf

[3] To access CCC Budget Explanatory Notes, visit https://www.usda.gov/our-agency/about-usda/budget and navigate to the appropriate fiscal year’s Explanatory Notes. Under “Farm Production and Conservation” find the pdf titled “Commodity Credit Corporation”.

[4] Congressional Budget Office. (2021.) “Supplemental Data for The Budget and Economic Outlook: 2021 to 2031.” Retrieved from: https://www.cbo.gov/system/files/2021-02/51317-2021-02-usda.pdf

[5] Perez, Michelle, Ph.D. “Quantifying Economic and Environmental Benefits of Soil Health.” American Farmland Trust, 2020. Retrieved from: https://farmland.org/project/quantifying-economic-and-environmental-benefits-of-soil-health/; and Friedman, Suzy, and Sands, Laura. “How Conservation Makes Dairy Farms More Resilient, Especially in a Lean Agricultural Economy.” Environmental Defense Fund, November 2019. Retrieved from:

[6] United States Department of Agriculture. (2021.) “FY 2021 Budget Summary.” Retrieved from: https://www.usda.gov/sites/default/files/documents/usda-fy2021-budget-summary.pdf

[7] Crop Insurance. “Insurance Providers.” Retrieved from: https://cropinsuranceinamerica.org/insurance-providers-list/ (Accessed August 2021.)

[8] United States Department of Agriculture. (2021.) “Federal Crop Insurance Corp: Summary of Business Report For 2008 thru 2017.” Retrieved from: https://www3.rma.usda.gov/apps/sob/current_week/sobrpt2008-2017.pdf (Accessed August 2021.)

[9] Congressional Budget Office. (2021.) “Supplemental Data for The Budget and Economic Outlook: 2021 to 2031.” Retrieved from: https://www.cbo.gov/system/files/2021-02/51317-2021-02-usda.pdf

[10] Information obtained from USDA Risk Management Agency’s Summary of Business Reports. Retrieved from: https://www.rma.usda.gov/SummaryOfBusiness (Accessed August 2021.)

[11] One of the repeat “worst offenders” is Dark Air Tobacco, which usually has a loss ratio over 600 percent!

[12] United States Department of Agriculture Farm Service Agency. (2019.) ”Dairy Margin Coverage Program Fact Sheet.” Retrieved from: https://www.fsa.usda.gov/Assets/USDA-FSA-Public/usdafiles/FactSheets/2019/dairy_margin_coverage_program-june_2019_fact_sheet.pdf

[13] Congressional Research Service. (2019.) “Farm Commodity Provisions in the 2018 Farm Bill.” Retrieved from: https://fas.org/sgp/crs/misc/R45730.pdf

[14] Dewey, Caitlin. “Why Americans Pay More For Sugar.” The Washington Post, June 8, 2017. Retrieved from: https://www.washingtonpost.com/news/wonk/wp/2017/06/08/why-americans-pay-more-for-sugar/

[15] Congressional Research Service. (2021.) “The Commodity Credit Corporation (CCC).” Retrieved from: https://fas.org/sgp/crs/misc/R44606.pdf

[16] Morgan, Dan. “Bogus Promise on Deficit Undercuts Lincoln.” The Fiscal Times, October 29, 2010. Retrieved from: https://www.thefiscaltimes.com/Articles/2010/10/29/Senator-Lincoln-Farm-Aid-Boosts-Deficit

[17] Done by both the Obama administration (Taxpayers for Common Sense (2015): https://www.taxpayer.net/agriculture/golden-fleece-blinders-for-blender-pumps/) and the Trump administration (Taxpayers For Common Sense, 2020, retrieved from: https://www.taxpayer.net/energy-natural-resources/another-taxpayer-subsidy-for-the-biofuels-industry/)

[18] Widmar, David. “The $4.7 Billion Farm Aid Package: Winners, Losers and Questions.” Forbes, August 28,2018. Retrieved from: https://www.forbes.com/sites/davidwidmar/2018/08/28/details-on-farm-trade-aid-released-unknowns-remain/?sh=36c9115e626e

[19] Congressional Research Service. (2021.) “Farm Policy: USDA’s 2019 Trade Aid Package.” Retrieved from: https://fas.org/sgp/crs/misc/R45865.pdf

[20] The five-year Olympic Average is calculated by taking the last five years’ data, removing the highest and the lowest data points, and averaging the remaining three. However, there is a yield floor that allows producers to remove extra low-yield years.

[21] Congressional Research Service. (2019.) “2018 Farm Bill Primer: ARC and PLC Support Programs.” Retrieved from: https://fas.org/sgp/crs/misc/IF11161.pdf

[22] Edwards, Chris. “Agricultural Subsidies.” Downsizing Government, April 16, 2018. Retrieved from: https://www.downsizinggovernment.org/agriculture/subsidies#_edn1

[23] The Environmental Working Group. (2021.) “Commodity subsidies in the U.S. totaled 240.5 billion from 1995 - 2020.” Retrieved from: https://farm.ewg.org/progdetail.php?fips=00000&progcode=totalfarm&page=conc®ionname=theUnitedStates

[24] Coleman, Robert. “The Rich Get Richer: 50 Billionaires Got Federal Farm Subsidies.” Environmental Working Group, April 18, 2016. Retrieved from: https://www.ewg.org/news-insights/news/rich-get-richer-50-billionaires-got-federal-farm-subsidies

[25] Andrzejewski, Adam. “Mapping the U.S. Farm Subsidy $1M Club.” Forbes, April 14, 2018. Retrieved from: https://www.forbes.com/sites/adamandrzejewski/2018/08/14/mapping-the-u-s-farm-subsidy-1-million-club/?sh=164bf4643efc

[26] We highly recommend reading AEI’s report, which can be accessessed here: https://www.aei.org/research-products/report/where-the-money-goes-the-distribution-of-crop-insurance-and-other-farm-subsidy-payments/

[27] Charles, Dan. “Farmers Got A Government Bailout in 2020, Even Those Who Didn’t Need It.” NPR Morning Edition, December 30, 2020. Retrieved from: https://www.npr.org/2020/12/30/949329557/farmers-got-a-government-bailout-in-2020-even-those-who-didnt-need-it

[28] Economic Research Service. (2021.) “Corn and soybean acreage have risen since 1990, while cotton is relatively flat, and wheat is down.” Retrieved from: https://www.ers.usda.gov/data-products/chart-gallery/gallery/chart-detail/?chartId=76955

[29] Rogers, David. “Crop insurance debate grows.” Politico, May 23, 2013. Retrieved from: https://www.politico.com/story/2013/05/crop-insurance-debate-grows-in-senate-091851

[30] Government Accountability Office. (2015.) “Crop Insurance: Reducing Subsidies for Highest Income Participants Could Save Federal Dollars with Minimal Effect on the Program.” Retrieved from:

[31] DeLay, Nathan. “The Impact of Federal Crop Insurance on the Conservation Reserve Program.” Cambridge University Press, August 22, 2019. Retrieved from: https://www.cambridge.org/core/journals/agricultural-and-resource-economics-review/article/impact-offederal-crop-insurance-on-the-conservation-reserve-program/AD977CB2835FD10E803438FD13EFF2AC

[32] As of June 2021, a Pandemic Cover Crop Program was introduced to give a $5 per acre crop insurance premium discount to farmers who plant cover crops, but this program is part of USDA’s pandemic assistance, not a permanent program. Via: https://www.rma.usda.gov/en/News-Room/Press/Press-Releases/2021-News/Producers-with-Crop-Insurance-to-Receive-Premium-Benefit-for-Cover-Crops

[33] Refer to the Crop Insurance Loss Ratios table on page 5 of this primer.

[34] “Cashing in on Federal Crop Insurance.” Taxpayers for Common Sense, June 16, 2021. Retrieved from: https://www.taxpayer.net/agriculture/cashing-in-on-federal-crop-insurance/

[35] To be clear, one of the largest legs of the Farm Bill’s disaster section is for livestock, which are not covered by crop insurance. This is not the section to which I am referring. I am referring to crop-specific disaster relief, including ad hoc legislative action separate from the Farm Bill.

[36] Peterson, Chris and Bailey, Jon. “Credit, crop insurance and sustainable agriculture.” Iowa State University, 2012. Retrieved from: https://lib.dr.iastate.edu/cgi/viewcontent.cgi?referer=https://www.google.com/&httpsredir=1&article=1407&context=leopold_grantreports

[37] Environmental Working Group. (2021.) Policy holder information. Retrieved from: https://farm.ewg.org/ci_premsubdetail.php?prod_id=359974970

[38] “IIABA Applauds Apparent Demise of Crop Insurance PDP Pilot Program.” Independent Agent, June 18, 2003. Retrieved from: https://www.independentagent.com/media/Pages/2003/NA20030620172116.aspx

[39] Congressional Research Service. (2019.) “U.S. Farm Program Eligibility and Payment Limits Under the 2018 Farm Bill.” Retrieved from: https://fas.org/sgp/crs/misc/R45659.pdf

[40] ibid.

[41] Participating in conference calls about what to plant, where to sell crops, securing financing, even filling out USDA subsidy program paperwork all qualify as “active personal management”. When this amendment was originally written, the Senate version included a requirement for a minimum of 500 hours (three months) of work to qualify; the House dropped this requirement. We recommend reinstating the 500 hour minimum alongside tightening the criteria to require active personal labor.

[42] Nearly 20,000 residents of the nation’s 50 largest cities received federal farm subsidies in 2017, according to the Environmental Working Group: https://www.ewg.org/news-insights/news/nearly-20000-city-slickers-received-farm-subsidies-2017