(pdf)

Introduction

Some lawmakers are seeking to repeal the $10,000 cap (for single and married couples jointly filing) on state and local tax (SALT) deductions put in place under the Tax Cuts and Jobs Act (TCJA). The debate over whether to include SALT cap repeal in the budget resolution has proven contentious as the benefits of the proposed tax cuts flow overwhelmingly to wealthy Americans which both undermines Democrats’ middle class messaging and decreases federal revenue.

What is the SALT deduction?

The SALT deduction allows filers who itemize to deduct certain state and local taxes from federal income when calculating their taxable income. This essentially allows some taxpayers to shift the burden of their high state and local government taxes to the federal government. The taxes eligible for the SALT deduction are certain real property taxes, income taxes, sales taxes (in lieu of income taxes), and personal property taxes.

Under TCJA, the SALT deduction was capped at $10,000 for single filers and married couples filing jointly. It is $5,000 for married taxpayers filing separately. The increase to the standard deduction under TCJA resulted in more taxpayers claiming the standard deduction rather than itemizing. The Joint Committee on Taxation (JCT) projects that 16.4 million taxpayers will claim a SALT deduction for tax year 2019, compared to 46.6 million taxpayers who claimed the deduction in 2017, according to the Internal Revenue Service (IRS). The SALT cap is temporary and scheduled to expire in 2025.

Who benefits from the SALT deduction?

The deduction primarily benefits wealthy taxpayers in high-tax states. There is widespread recognition across the political spectrum that the vast majority of the SALT deduction benefits the wealthy, and a repeal of the cap on the SALT deduction would amount to a tax break for the wealthiest Americans.

Tax Policy Center: “Only about 9 percent of households would benefit from repeal of the Tax Cuts and Jobs Act’s (TCJA) $10,000 cap on the state and local property tax (SALT) deduction, and more than 96 percent of the tax cut would go to the highest-income 20 percent of households”

Tax Foundation: “The SALT deduction tends to benefit states with many higher-earners and higher state taxes.”

Joint Committee on Taxation: “The repeal [of the cap] is estimated to result in a decrease in tax liability for 13.1 million taxpayers, 94 percent of which have $100,000 or more of economic income. Additionally, approximately 99 percent of the decrease in tax liability accrues to taxpayers with $100,000 or more of economic income.”

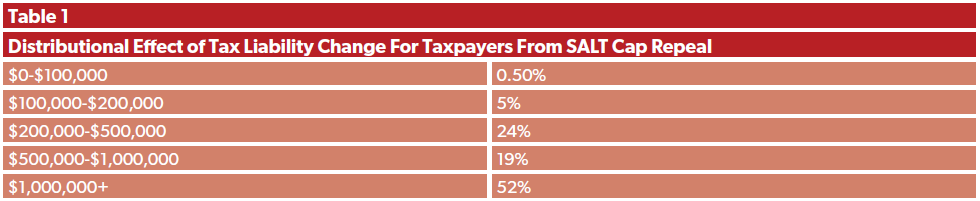

Source: Joint Committee on Taxation

- As Table 1 shows, the benefits of the SALT deduction are claimed largely by wealthy Americans. This is due in part to the way in which the SALT deduction is calculated. SALT deductions are dependent on taxable income, and in a progressive tax system, a deduction is more valuable for higher income taxpayers. Additionally, higher income usually corresponds to a higher consumption rate, meaning higher income individuals likely have higher sales and property tax payments. In other words, the value of the SALT deduction is proportional to the taxpayer’s income.

However, the other beneficiaries of the SALT deduction are high tax states, such as New York, California, New Jersey, and Illinois. With a SALT deduction in place, as states and localities increase taxes, the deduction becomes more valuable for itemizers. For example, in 2017 the average SALT deduction in New York was $23,804 compared to just $5,451 on average in Alaska.

The SALT deduction allows states and localities to shield certain taxpayers from the full force of the tax increases, essentially encouraging state and local governments to increase taxes. However, only taxpayers who itemize receive this federal reprieve from high state taxes. Those claiming the standard deduction, the vast majority of taxpayers, do not benefit from the deduction. NTU Foundation writes how Illinois presents a useful case study of the SALT deduction encouraging tax-and-spend policies.

How Does a SALT Cap Repeal Impact Federal Revenue?

The SALT Caucus, made up exclusively of Members from California, New York, New Jersey, Illinois, Connecticut, and the District of Columbia, are pushing to repeal the $10,000 SALT deduction cap. The benefits of the repeal of this cap would largely flow to their states.

While this vocal group of lawmakers say “no SALT, no deal,” a repeal of the SALT cap could endanger the prospects for the massive $3.5 trillion resolution. Concerns on both sides of the aisles have surfaced on the size of the package along with how to pay for it. Repealing the $10,000 cap would not only be a tax break for a minority of wealthy Americans, it would also decrease federal revenue.

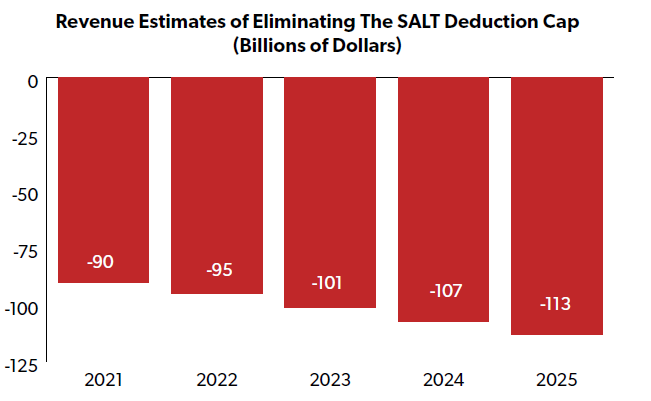

Table 2

Souce: Tax Foundation

- As Table 2 shows, the estimated decreases in yearly federal revenue would be over $500 billion over the next five years. The $3.5 trillion bill is unlikely to be fully paid for, and Democrats are already having to get creative to try to find ways to pay for this behemoth of a spending bill. The repeal of the SALT deduction would leave them further in the hole. This would likely add to the federal deficit that is already rapidly approaching $30 trillion.

Debunking Myths Around the SALT Debate

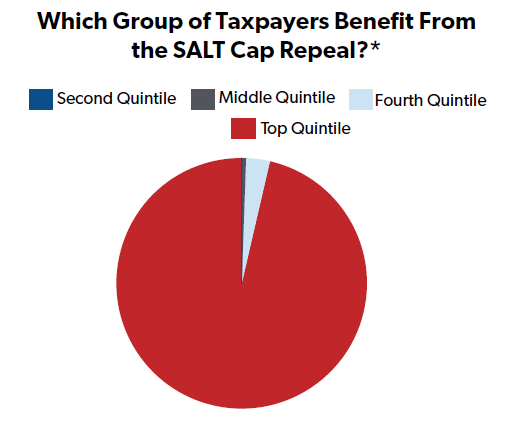

Myth: “It’s a tax break for the middle class”: One lawmaker pushing for the cap repeal called it an “assault on hardworking men and women of labor” and another invoked Gandhi, calling the fight over the tax cut a “SALT march.” As President Biden would say, “c’mon man.” While middle class Americans may live in the states that benefit from the SALT deduction, they are by no means the beneficiaries of it. Repealing the SALT deduction cap makes the tax code more regressive. Less than four percent of the benefits of cap repeal would go to the bottom 80 percent of taxpayers. Progressives like Rep. Alexandria Ocasio-Cortez (D-NY) appropriately called the repeal of the SALT deduction cap “a gift to billionaires.” With the growth of remote work, it’s understandable that high tax states are concerned about higher income individuals relocating to states with a more hospitable tax code. As Table 3 shows, the benefits of the SALT cap repeal overwhelmingly benefit the wealthy. However, simply calling something a “middle class tax cut” does not make it true.

Source: Tax Policy Center

Myth: “It’s double taxation”: Some claim that the SALT deduction protects against “double taxation.” As NTU Foundation notes, this argument does not hold water. Taxes collected at the federal and state levels are not for the same purpose. Taxpayers are paying two different governments for two different sets of programs. As NTUF notes, “Therefore, the solution to local and state taxes being high, either on their own or in combination, is not a poorly-structured federal deduction that spreads the pain out to taxpayers in lower-tax areas, it is instead to lower taxes in places where they’re too high.”

Myth: “Republicans should support the deduction”: Some have argued that Republicans should support the deduction because it shifts resources from the federal government to cities and states. While conservatives have generally supported the power of local governments over the federal government, this argument does not apply for the SALT deduction. The SALT deduction insulates high tax states from their harmful policies by providing a federal tax benefit. Conservatives have generally supported local and state governments because they are more accountable to their constituents. However, the SALT deductions make them less accountable by rewarding high-tax state policies. The SALT deduction allows states and localities to give their high income earners a discount on their taxes. Preserving the deduction cap, or better yet, a full repeal of the SALT deduction would result in wealthy residents feeling the full effect of the policies passed by their state and local governments.

Myth: “It raises taxes”: Some conservatives are concerned that the repeal of the SALT deduction is tantamount to a tax hike. NTU has long supported a simpler, fairer, and broader tax code, and the repeal of the SALT deduction is not at odds with this philosophy. The impacts of the deduction cap would have almost no impact on 80 percent of taxpayers. While some high-income taxpayers may face increased tax liability under the cap, this is because of the tax policies passed by their state and local representatives. Again, the cap on deductions at the state and local levels makes a fraction of taxpayers feel a larger l effect from high state tax rates. There are plenty of reforms lawmakers at all levels of government should consider to reduce tax complexities and burdens for taxpayers. However, repealing the SALT deduction cap would make the tax code more regressive and invite higher state taxes for many taxpayers.

Conclusion

Ideally, Congress would repeal the SALT deduction entirely. However, given the political environment, the best case scenario would be preserving the $10,000 cap. The argument that repealing the cap would benefit the majority of Americans is wholly at odds with the data. The SALT deduction cap does not harm the middle class. Analysis from the left and right of center, along with nonpartisan research from the Joint Committee on Taxation, confirms that a repeal of the SALT deduction cap is simply a tax break for the wealthiest taxpayers. Further, the SALT deduction creates tax code complexity and economic distortions that invite higher taxes at the state and local level.

Additional Resources:

- Tax Foundation: Benefits of SALT deduction by county and by state.

- NTUF: Illinois Case Study on Effect of SALT Deduction

- NTUF: Repealing SALT would unnecessarily benefit the wealthy