Key Facts:

Even though our tax code remains highly progressive, four Democratic senators have recently proposed new tax increases that would exclusively target the highest income earners.

Senators Sanders and Warren have proposed updated versions of their proposals to tax net worth, which nevertheless continue to drastically overestimate the potential revenue to be raised, handwave difficult questions of administrability, and portend significant economic consequences.

Senators Booker and Van Hollen propose dramatic expansions of the standard deduction and Child Tax Credit, further narrowing the tax base and adding to the deficit.

With Tax Day approaching, many Americans have taxes on their minds. Senators are evidently no different in that regard, as four of them have already introduced plans to significantly overhaul the tax code in 2026.

Though there are four separate plans between them, they fall into two clear buckets. Senators Bernie Sanders (I-VT) and Elizabeth Warren (D-MA) have reintroduced updated versions of previous wealth tax proposals, while Senators Cory Booker (D-NJ) and Chris Van Hollen (D-MD) have each taken the lead on plans to eliminate income taxes for lower-income taxpayers (many of whom already do not owe any income taxes due to the existing standard deduction and refundable credits).

Sanders and Warren: The Wealth Tax Plans

Senators Sanders and Warren have been proposing competing wealth tax plans since facing off in the 2020 presidential campaign. The revised plans that they have recently released are much the same, and suffer from all the same flaws.

Senator Sanders’s Make Billionaires Pay Their Fair Share Act

Sanders’s first proposed wealth tax back in 2019 involved graduated marginal brackets, with a wealth tax rate starting at 1% on net worth over $32 million and ranging all the way to 8% on net worth over $10 billion. His latest Make Billionaires Pay Their Fair Share Act (hereafter shortened to the Make Billionaires Pay Act or MBPA) is more straightforward in this sense, imposing a 5% wealth tax rate on the net worth of taxpayers with a net worth over $1 billion.

The revenue raised from this proposal would be used to:

- Fund $3,000 direct payments to every individual, including dependents, living in a household earning below $150,000 ($959 billion over a decade)

- Reverse OBBBA’s reforms to Medicaid and the Affordable Care Act ($1.1 trillion over a decade)

- Expand Medicare to cover dental, hearing, and vision expenses ($290 billion over a decade)

- Increase annual appropriations for the Housing Trust Fund from $577 million in FY2025 to $86 billion ($859 billion over a decade)

- Expand childcare funding ($700 billion over a decade)

- Provide grants to states to fund a $60,000 minimum salary for public school teachers ($152 billion over a decade)

- Increase funding for Medicaid’s Home and Community-Based Services program ($300 billion over a decade)

This adds up to $4.35 trillion in additional spending over the course of the next decade, according to the estimates provided by Senator Sanders’s office. Sanders cites an analysis by Emmanuel Saez and Gabriel Zucman, a pair of French economists now at UC Berkeley who are known for putting together questionable analyses to build support for wealth taxes, to claim that the tax would raise $4.4 trillion over the next decade.

The Saez and Zucman analysis relies on the assumption that the tax would only be subject to 10% avoidance, a wildly optimistic assumption given the inherent difficulty of valuing the privately-held, non-liquid assets that billionaires hold substantial portions of their wealth in. The Tax Foundation estimated that the tax could raise $3.3 trillion using the 33% avoidance assumption used by the Sanders and Warren campaigns in 2020, while Kyle Pomerleau of the American Enterprise Institute factors in avoidance for existing taxes to arrive at a revenue estimate of just $2.3 trillion.

Senator Sanders does himself few favors in this regard, with his proposal being silent on exactly how to value these subjective assets beyond directing the Secretary of the Treasury to figure it out. The only tangible enforcement mechanisms included are a requirement to audit no less than 50% of billionaires subject to the tax and an additional appropriation of 1% of revenues collected by the wealth tax to the IRS for enforcement of the wealth tax. This also raises the question of how the IRS is meant to build up the infrastructure to enforce a brand-new tax if the funding it receives is based on a percentage of revenue collected a year after enforcement begins.

Additionally, the decision under the Sanders proposal to subject an individual’s entire net worth to the 5% tax once they exceed the $1 billion threshold creates an extreme tax cliff. A taxpayer judged to have a $975 million net worth would face no wealth tax liability, while an individual at $1 billion would owe $50 million in tax, leaving them with $950 million. “Why is the person worth $1 billion poorer than the person worth $975 million?” is, in this case, not a bad riddle or the lead-up to a philosophical platitude, but the consequence of poorly-designed tax brackets.

Senator Warren’s Ultra-Millionaire Tax Act

Senator Warren’s 2020 proposal involved a 2% wealth tax on net worth between $50 million and $1 billion, and a 6% tax on wealth over $1 billion. Her latest revision, the Ultra-Millionaire Tax Act of 2026 (UMTA), maintains the same brackets with a slightly lower rate on billionaires: 2% on net worth between $50 million and $1 billion, and 3% on net worth over $1 billion.

Senator Warren, like Senator Sanders, turns to the dubious authority of Saez and Zucman to estimate $6.17 trillion in revenue from the tax over the next decade. Five years prior, Saez and Zucman had estimated less than half as much revenue from the same tax.

Senator Warren, like Senator Sanders, leaves much of the administrative difficulties for the Treasury Secretary to resolve. However, she includes a $100 billion increase in the IRS’s budget in the (likely overly optimistic) hopes of increased revenue from tax enforcement, a 30% minimum audit rate on affected taxpayers (compared to 50% for Sanders), and a 40% “exit tax” on the wealth over $50 million of taxpayers who renounce U.S. citizenship. This punitive exit tax violates what has long been held to be a fundamental right both at home and internationally. Warren, unlike Sanders, also includes penalties for “understatement” of the value of assets, defined as not coming up with the same number when valuing an asset that the IRS does.

Other than the additional $100 billion to the IRS, the UMTA does not specify additional spending to accompany the tax. However, Warren asserts that it could be used to pay for universal childcare, building homes, expanding the Child Tax Credit (CTC), lowering Medicare eligibility to 55 years old, providing universal paid family leave, and tuition-free community college.

Analysis

Wealth taxes are often deceptive, since the single-digit percentage rates appear low compared to, for example, the 37% top individual income tax rate. However, since a wealth tax applies to total wealth, they are usually far more burdensome. For instance, Sanders’s 5% top wealth tax rate is effectively a 100% income tax rate on an asset with a 5% annual return.

Even before one can experience the economic consequences of wealth taxes, the IRS and Treasury would be left under both the MBPA and UMTA to untie myriad Gordian knots of asset valuation. Unlike shares in publicly-traded companies, privately-held assets do not carry with them a publicly available and objective market valuation. Valuing these assets in a manner that is both fair and consistent is a major problem.

The most colorful example of how difficult this can prove came about with the estate valuation of Michael Jackson, who died in 2009. For purposes of the estate tax, his heirs submitted a certified appraisal of his name, image, and likeness rights valuing them at $2,105. The IRS disagreed, informing Jackson’s descendants that the rights were worth $434 million. This dispute was eventually resolved after a 12-year court battle, with the judge eventually setting the value of the rights at $4 million.

But imagine if the IRS were expected to go through this type of battle with thousands of public, wealthy personalities on an annual basis, arguing with Taylor Swift every single year about whether her name, image, and likeness rights have increased or decreased in value after each year’s worth of new celebrity gossip. The problem only magnifies the lower the wealth tax threshold is.

Another issue that remains unaddressed in either proposal is the attribution of the assets of private, philanthropic organizations. Saez and Zucman have argued in the past that the assets of private charities would need to be assigned to wealthy individuals in some manner as part of their net worth to prevent charities from being used as wealth tax shelters. Not only would doing so be an administrative nightmare of its own, it would also drastically reduce the scope of private philanthropy, which plays an important charitable role alongside the social safety net. Neither Sanders’s plan nor Warren’s includes any mention of this, passing off such thorny questions to the Treasury Department to tackle.

This combination of administrative infeasibility and economic damage has led the majority of developed nations that once had wealth taxes to eliminate them. Today, only three out of the dozen or so OECD countries that once had a wealth tax maintain one today.

From a purely economic perspective, they are also more harmful than other taxes of a similar magnitude because they are poorly targeted. Specifically, they target the biggest engine of economic growth—investment capital—and leave less of it available to fund the new productive enterprises and productivity improvements that bring prosperity and good-paying jobs.

Supposed targeted taxes on the wealthy often, in practice, turn out to be taxes on investment and businesses, harming their ability to create more jobs and bring more value to consumers. New products, new inventions, and new stores physically nearer to your location all come from investment. Investment also increases productivity, or the value that a business’s employees can return to the business for the same labor. When an employee can return more value for their labor, their continued employment is worth more to the business—which, in turn, must either reflect that increased value through salary increases or risk losing the employee to a competitor willing to more fairly compensate them.

The smaller the pool of investment capital, the harder and more costly it is for businesses to make these kinds of long-run improvements. The wealth of billionaires does not sit idly in a vault—it is constantly being moved around the economy and adding to that pool of investment capital. Wealth taxes forcibly yank this capital out of the economy and drop it down the bottomless pit of the federal government’s debt.

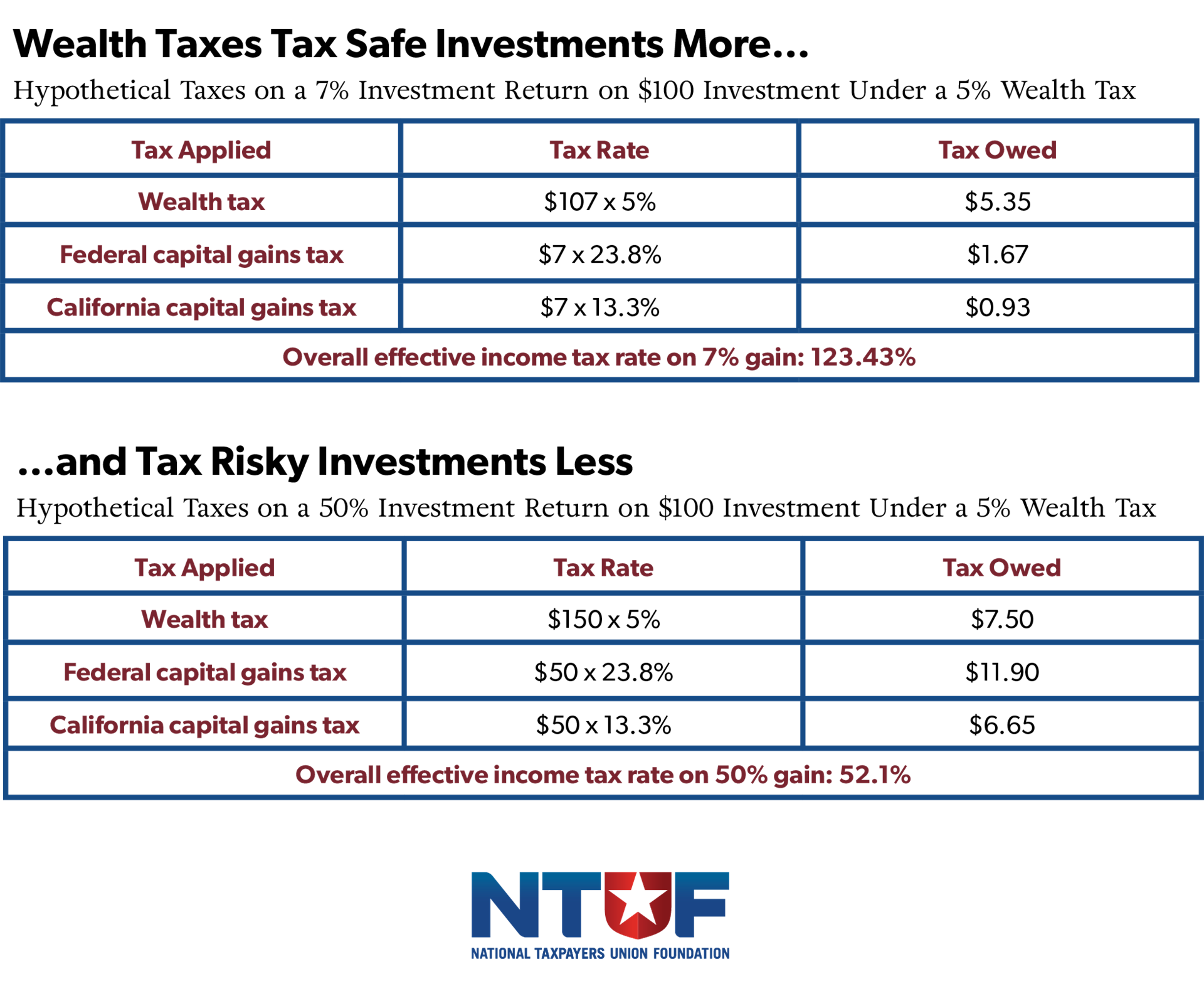

And wealth taxes manage to be harmful in a way that sets them apart from normal income or capital gains rate increases. Ideally, taxes on investments should aim to exempt normal returns, or returns that represent the baseline of what the investor expected to receive on their investment. For instance, if an individual invests in the stock market, they may expect a historical return of 7 or 8%. Wealth taxes, on the other hand, fall heavily on normal returns. Take an asset subject to Sanders’s 5% wealth tax—any appreciation to that asset’s value is now facing what is effectively a 100% income tax on the first 5% that it appreciates by. Meanwhile, an asset that sees a large return and increases by 20% is subject to a far lower effective tax rate.

Consider an example asset worth $100 with a steady 7% return—normally a fairly healthy investment. That asset, at the end of the year, is now worth $107, all of which is subject to a 5% wealth tax (or $5.35 in tax). Then, imagine the investor sells the $107 asset, with the $7 return taxed at the 23.8% top long-term capital gains rate including the net investment income tax ($1.67 in tax). In total, this investor is left owing $7.02 in tax on a $7 capital gain.

And were they unfortunate enough to be a resident of California, the state with the highest capital gains tax rate, they would owe a further $0.93 in state capital gains tax. In fact, the investor would need to receive an 8.64% return on any investment just to break even.

As can be seen, the wealth tax liability changes only slightly in this scenario, and the overall effective tax rate is less than half of what it was with a more modest gain. Consequently, wealthy individuals lose a great deal of the incentive to try and grow their wealth once they hit the wealth tax threshold, or are pushed toward riskier investments.

The result would be that investment dollars are sucked away from profitable, stable enterprises and pushed towards investments with a much higher probability of going bust. Not only would this mean more economic turmoil and unpredictability, it means that the businesses that are currently producing goods and services that Americans value would have less capital available to finance productive investments.

Another economic issue is that wealth taxes drive corporate consolidation. Successful entrepreneurs whose start-ups grow rapidly in value often remain relatively cash-poor, with most of their wealth lodged in the value of their company. Wealth taxes force these founders into a position where they are forced to sell shares in their businesses to pay their wealth tax bills, enabling them to be gobbled up by larger companies seeking to defang a disruptive competitor.

Lastly, the suggestions by Senators Sanders and Warren that wealth tax revenue could be used to fund vast new social programs ignores the fact that the federal government is incapable of funding the programs that currently exist. The latest budget projections estimate that the federal government will run a deficit of over $23 trillion between 2026 and 2035, on top of the existing national debt which recently exceeded $39 trillion. Even the senators’ likely overoptimistic projections of $4–6 trillion dollars in additional revenue from their plans fail to raise enough money to cover more than a quarter of the deficit taxpayers are already faced with, let alone new spending ideas.

Booker and Van Hollen: The Standard Deduction Multiplier Plans

Senator Booker’s Keep Your Pay Act (KYPA) and Senator Van Hollen’s Working Americans Tax Cut Act (WATCA) each aim to allow lower-income Americans to benefit from a far higher standard deduction. Tax changes passed under the 2017 Tax Cuts and Jobs Act (TCJA) and extended under the One Big Beautiful Bill Act (OBBBA) have already raised the standard deduction from $6,350 single/$12,700 married filing jointly in tax year 2017 to $15,730 single/$31,500 married filing jointly this year (tax year 2025).

Senator Booker’s proposal also implements the American Family Act (AFA) and the Tax Cut for Workers Act (TCWA), which expand the CTC and Earned Income Tax Credit (EITC), respectively. Senator Van Hollen has cosponsored both the AFA and the TCWA as well.

Shared Plans - Expanding the CTC and EITC

The AFA would increase and bifurcate the current CTC, which is currently worth $2,200 for 2026. The AFA would raise the annual credit to $4,320 for children under the age of 6, while children aged 6–17 would provide a credit of $3,600. Additionally, the phase-out threshold would be raised from $200,000 to $300,000 for single filers, though married filers would remain subject to the same $400,000 phase-out.

The AFA would also create a new “baby bonus” for newborns in the year of birth worth $2,400. Eligibility for this bonus would begin to phase out at $112,500 for single filers and $150,000 for married filers. The entire CTC, including the “baby bonus,” would become fully refundable—currently, only $1,700 of the $2,200 credit is refundable.

These changes to the CTC represent a more costly version of reforms NTUF has recommended. NTUF’s recommendations for CTC reform include raising the base credit amount to $2,500, establishing a $400 “baby bonus,” and making the credit fully refundable. However, NTUF also recommends lowering, not raising, the phase-out levels to $100,000 for single filers and $200,000 for married filers.

The TCWA would lower the eligibility age for childless workers from 25 to 19, while removing the current maximum eligibility age of 64 years old. Additionally, the phase-out and phase-in rates would be doubled, significantly increasing the maximum available benefit. Phase-out and phase-in levels would be increased only slightly.

Senator Booker’s Keep Your Pay Act

The KYPA would more than double the standard deduction for single filers from $16,100 next year to $37,500, and from $32,200 to $75,000 for married filers filing jointly. This would primarily benefit middle- and upper-middle income taxpayers, as most low-income taxpayers are already paying zero or negative tax rates after the existing standard deduction and refundable tax credits. The highest-income taxpayers would also benefit from this change, though proportionately less, as even this supersized standard deduction would represent a relatively small percentage of their taxable income.

To compensate for these tax cuts, the KYPA would raise the marginal tax rate for the two highest income brackets, from 35% and 37% to 41% and 43%.

In total, these tax increases would not come close to offsetting the revenue loss. The Tax Foundation estimates that Booker’s plan would raise $650 billion in additional revenue against tax cuts of about $7.6 trillion between 2026–2035, for a total deficit impact of $6.9 trillion. The Penn-Wharton Budget Model is slightly rosier, estimating $6.4 trillion in tax cuts, $1.4 trillion in tax increases, and a deficit impact of around $5 trillion.

Senator Van Hollen’s Working Americans Tax Cut Act

In contrast to Senator Booker’s simple increase to the standard deduction, Senator Van Hollen’s changes to the standard deduction would take the form of a new “Alternative Maximum Tax” modeled along similar lines to the Alternative Minimum Tax.

Like with the Alternative Minimum Tax, the Alternative Maximum Tax would complicate the tax code by creating another parallel tax code that overrides the traditional tax code for eligible taxpayers. However, unlike the Alternative Minimum Tax, which applies if it would result in a tax increase, Van Hollen’s Alternative Maximum Tax would apply if it results in a tax decrease.

The WATCA would create a new “cost of living exemption,” worth $46,000 for single filers and $92,000 for married filers in 2026 (adjusted annually for inflation). Taxpayers with incomes of 175% of this level or below ($80,500 for single filers and $161,000 for married filers in 2026) would calculate their tax liability with all income below the cost of living exemption excluded and all additional income taxed at a 25.5% rate. Exemptions for foreign earned income (including American overseas territories and Puerto Rico), as well as social security benefits, would be added back to the taxpayer’s gross income calculation as well. The taxpayer would then compare the result to their traditional tax liability and use whichever amount was lower.

The WATCA would then create new surtaxes for taxpayers exceeding certain income thresholds: an additional 5% on income over $1 million single/$1.5 million married, 10% on income over $2 million single/$3 million married, and 12% on income over $5 million single/$7.5 million married. All told, it would result in a 49% top individual income tax rate.

Compared to Sen. Booker’s income tax proposal, the WATCA’s proposed changes to the standard deduction would have a significantly lower impact on revenue, since they do not apply to all taxpayers. Where the Tax Foundation estimates that Sen. Booker’s standard deduction changes would reduce revenue by $5.59 trillion over a ten-year period, Sen. Van Hollen’s proposal would reduce revenue by $1.36 trillion over that same time period.

Revenue from Sen. Van Hollen’s proposed new surtaxes on high-income taxpayers would nearly offset the loss, raising an additional $1.18 trillion. EITC and CTC changes would have an additional deficit impact of around $2 trillion over a decade, however, leaving the plan still far into the red.

Analysis

While targeted at providing tax relief, the tax cuts proposed by Sens. Booker and Van Hollen both take ideas implemented successfully under the TCJA and OBBBA and inflate them to the point that they are no longer good policy. Increasing the standard deduction was an important part of the TCJA and OBBBA because it both provided tax relief and simplified deductions for taxpayers who used to itemize, with about 90% of Americans now taking the standard deduction.

Our income tax code is already very progressive and relieves most low-income taxpayers from any tax liability. Extending the deduction to the levels proposed by Sens. Booker and Van Hollen would exempt a large percentage of middle-income taxpayers from federal income taxes as well, leaving the tax base completely reliant on the higher-income taxpayers that are simultaneously being subjected to higher tax rates.

Sen. Van Hollen’s proposal for an Alternative Maximum Tax may be more limited, but it carries problems of its own. One of the key goals—and successes—of both the TCJA and OBBBA was simplifying the tax code by reducing the number of taxpayers who itemize and the number of taxpayers forced to deal with the complicated Alternative Minimum Tax. Sen. Van Hollen’s proposal would undermine these achievements by subjecting taxpayers with lower income levels to a different parallel tax code. The Alternative Minimum Tax is the kind of confusing mechanism that legislators should be working to excise from the tax code, not duplicate.

The same theme of overdoing a successful TCJA/OBBBA reform holds true with proposed changes to the CTC. The TCJA first doubled the CTC beginning in 2018, while OBBBA increased the CTC from the $1,000 level, to which it was scheduled to revert, to $2,200 (adjusted for inflation moving forward). Increasing the credit to a maximum of $4,320 would excessively increase a credit that NTUF generally supports, resulting in a deficit impact of nearly $2 trillion over the next decade.

Conclusion

The latest wealth tax proposals by Senators Warren and Sanders remain heavy on ideas and exceedingly light on substance, failing once again to come up with realistic solutions to address or even mitigate wealth taxes’ inherent drawbacks. Though they may at first appear attractive to Americans eager to “tax the rich,” taxpayers should be aware that the consequences of an enacted wealth tax would crash down harder on the heads of the average person than on those of billionaires.

And while the proposals by Senators Booker and Van Hollen are relatively measured and aimed at providing tax relief, they remain impractical and rash. Modest increases to the standard deduction or the CTC and EITC are far from unreasonable proposals to help lower-income taxpayers, but the expansions proposed by the senators are not feasible in view of the state of the budget.