In the buildup to every World Cup, soccer fans the world over engage in the great quadrennial pastime of arguing over which teams received the best and worst draws for the group stage. The term “Group of Death,” and its lesser-used counterpart “Group of Life,” have become such frequent objects of debate that they have begun to bleed out of the World Cup lexicon and into other multi-stage tournaments.

But the problem with this debate is that it is so subjective. Statistics can inform the debate, not conclude it. And that’s why the people are crying out for someone, anyone, to answer the question that burns in their hearts: forget about how good the teams are, which teams are going to pay the most tax due to this year’s World Cup?

Oh yes. There’s always a tax angle.

Background: Nonresident Athlete Compensation

Domestic Competition

Every time an athlete plays in a professional sports game in a city they do not live in, a new CPA is born. Professional sports create tax complexity long before national borders get crossed.

In the United States, professional athletes are subject to tax not only in their home state and city, but also in any cities and states in which they play away games. Colloquially known as “jock taxes,” these obligations involve parceling out income taxes to states and cities based on the proportion of “duty days” spent in each.

Duty days include not only days spent playing games or matches, but also days spent training, practicing, or otherwise engaged in the professional activities a player is required to participate in to earn their salary. Prize money earned in tournaments can also be subject to these same obligations.

Jock tax obligations do not just fall upon the LeBrons and Mahomeses of the world. Professional athletes at any level, including minor leagues and sports with low salaries, face the exact same tax filing requirements—as do coaches, trainers, and other logistics staff members. Managing these obligations can be incredibly burdensome for individuals with more modest salaries.

International Competition

But the picture gets many times more complicated at the international level. At the domestic level, the risk of double taxation is near zero—an athlete’s state of residency will grant credits against taxes paid to other states and localities (even if the process is complicated and often imperfect). Federal taxes are, of course, unchanged between locations.

At the international level, athletes need to confront entirely separate and often unfamiliar national tax systems. Interactions between those separate tax systems and an athlete’s home country are governed by bilateral tax treaties that may or may not exist.

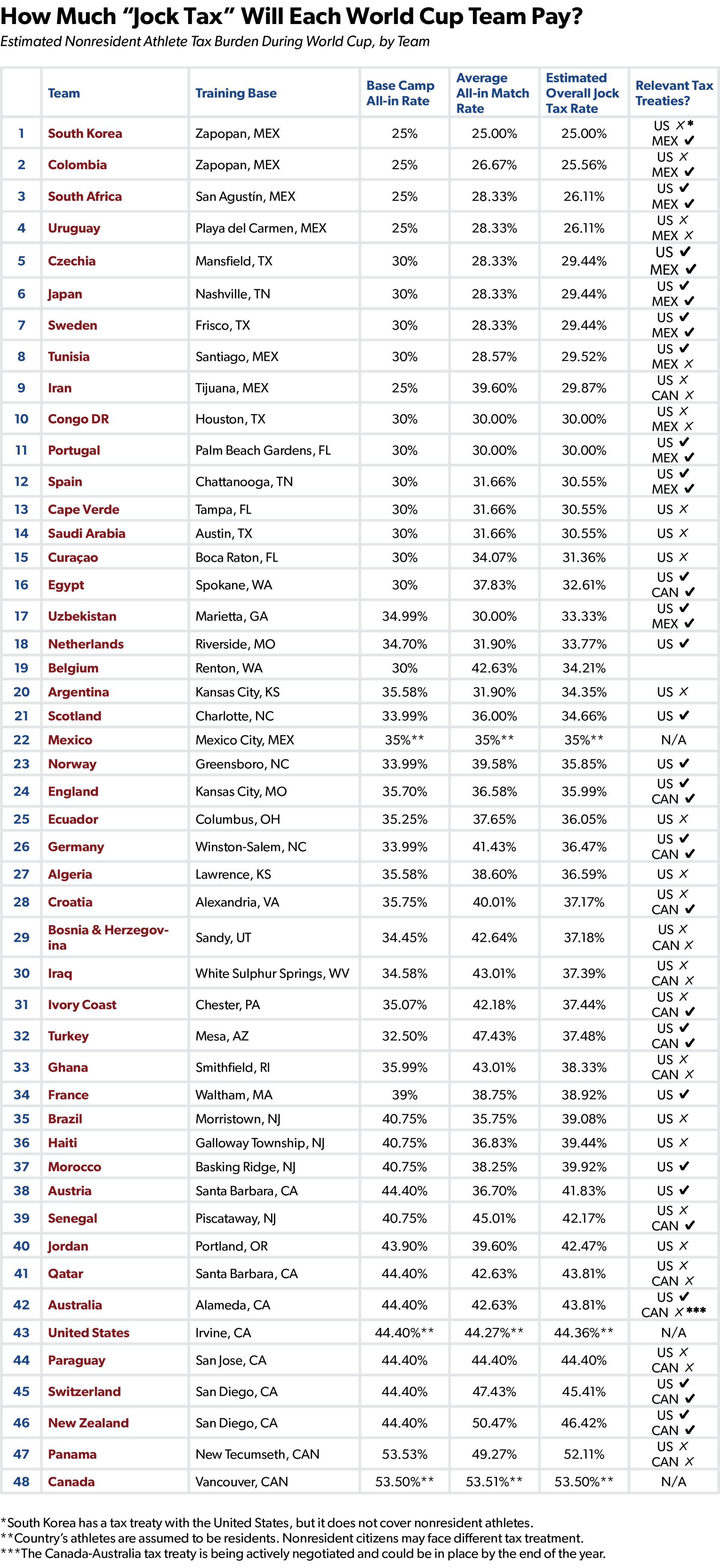

Even where these tax treaties exist, they do not make tax compliance simple. Of the 47 visiting World Cup nations, 22 have a tax treaty with the United States. Generally, these treaties allow for some level of de minimis exemption, where athletes under a certain level of gross earnings within the United States can avoid tax filing obligations. However, these thresholds max out at $20,000 for German and British athletes, which most World Cup soccer players will easily exceed.

Nonresident athletes playing in the United States are subject to a 30% tax rate on gross earnings, which include a proportional amount of the athlete’s overall earnings. For instance, Portugal’s Cristiano Ronaldo earns roughly $300 million. Should he spend 30 out of, say, 240 duty days in the United States, the United States would be entitled to tax around $37.5 million at the 30% rate.1

Tax treaties enable athletes playing in the United States to set up a Central Withholding Agreement (CWA). When properly applied for and set up, a CWA allows an athlete to designate a withholding agent to withhold from the athlete’s income, and more importantly, to allow the athlete to claim deductions for qualified expenses incurred while in the United States against their gross earnings.

Of course, not every World Cup match will be played in the United States this year. Mexico is the most tax-friendly option available to visiting athletes, assessing nonresident athletes at a lower 25% flat rate. Canada requires withholding at a 15% rate, but requires nonresident athletes to subsequently file at its normal (very high) tax rates.

While athletes playing in Mexico do not need to worry about sub-federal income taxes, athletes playing in the United States and Canada do. In the United States, these state and local-level taxes are assessed on gross income even if an athlete has a CWA in place.

While most World Cup athletes from nations with sophisticated international tax systems are generally shielded from double taxation, this is less certain for smaller, developing nations. It is entirely up to the athlete’s home country to provide, or not provide, a credit.

Assuming that an athlete’s home country provides tax credits for taxes paid to other countries, tax rates only result in a net tax increase if they exceed the rate that the athlete is paying to their nation of residence. An athlete paying a 25% tax rate to Mexico will simply have less foreign tax to credit against their resident country’s tax liability if their resident country’s effective tax rate exceeds that amount.

As mentioned above, duty days do not consist only of match days. Each team has also set up a “base camp” that they return to between matches. These were set up and chosen by each team from a list approved by FIFA. Days spent training and practicing at base camps will also incur jock tax obligations.

In a final slap in the face to players, coaches, and trainers, FIFA managed to secure a deal with the IRS for an exemption from federal income tax—for FIFA and national associations. Individual players remain on their own.

The 2026 World Cup Group Stage Tax Draws

The following are each World Cup nation’s tax draws, or their jock tax liabilities across group stage matches. This assumes that each team spends the same number of duty days at each match venue (per match) for simplicity. Also listed are each team’s training base camp and the associated tax burden, as well as each team’s participation in relevant tax treaties.

For simplicity’s sake, we will assume that each team’s players all face the maximum marginal tax rate. For most teams, players’ income will likely be high enough that the impact of lower brackets will be negligible.

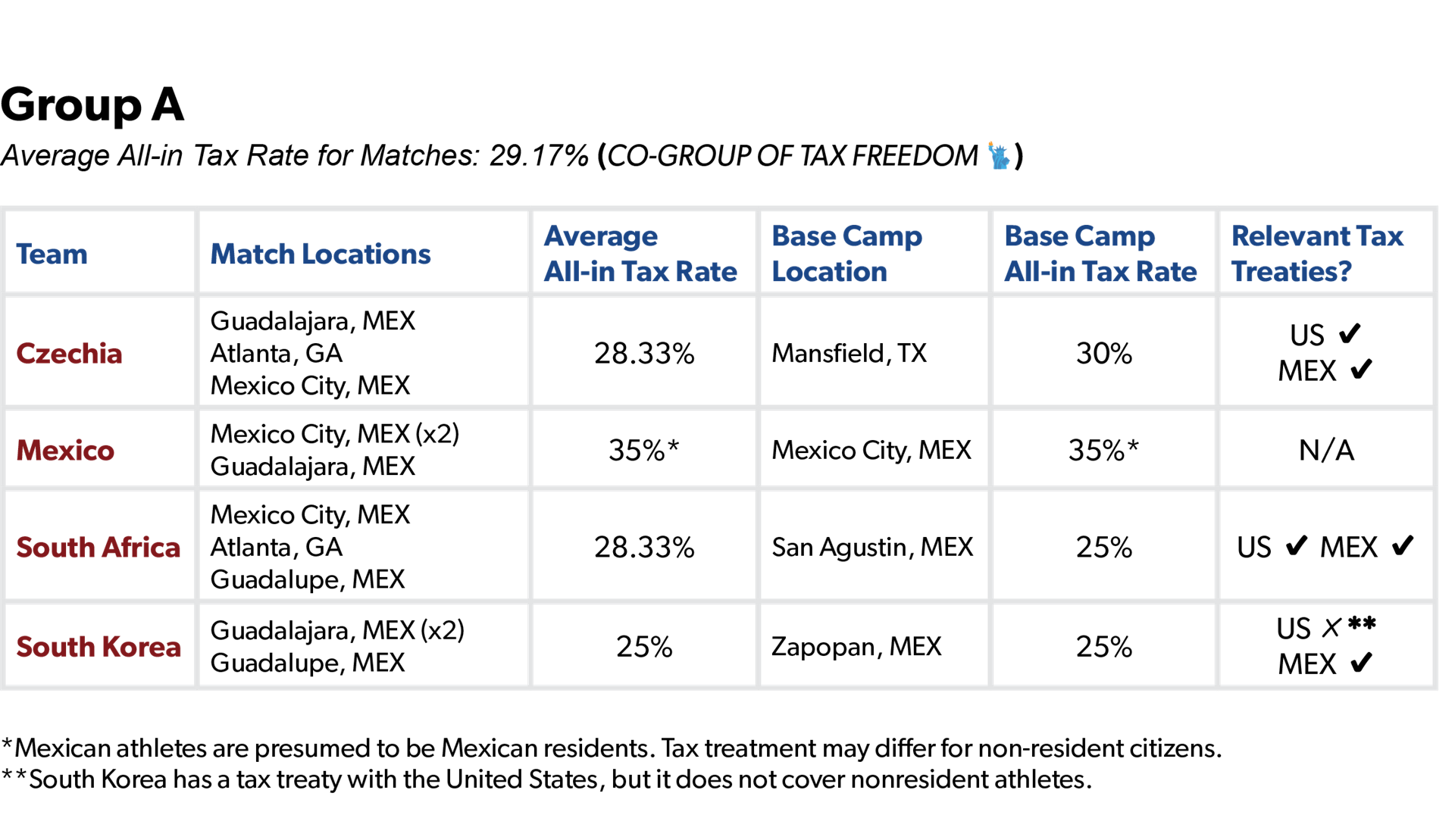

Group A is tied with Group K as our Group of Tax Freedom. With matches and base camps all located in Mexico, Texas, or Georgia, tax obligations are fairly limited. Each team has all relevant tax treaties except for South Korea, which lacks an athletics provision in its tax treaty with the United States.

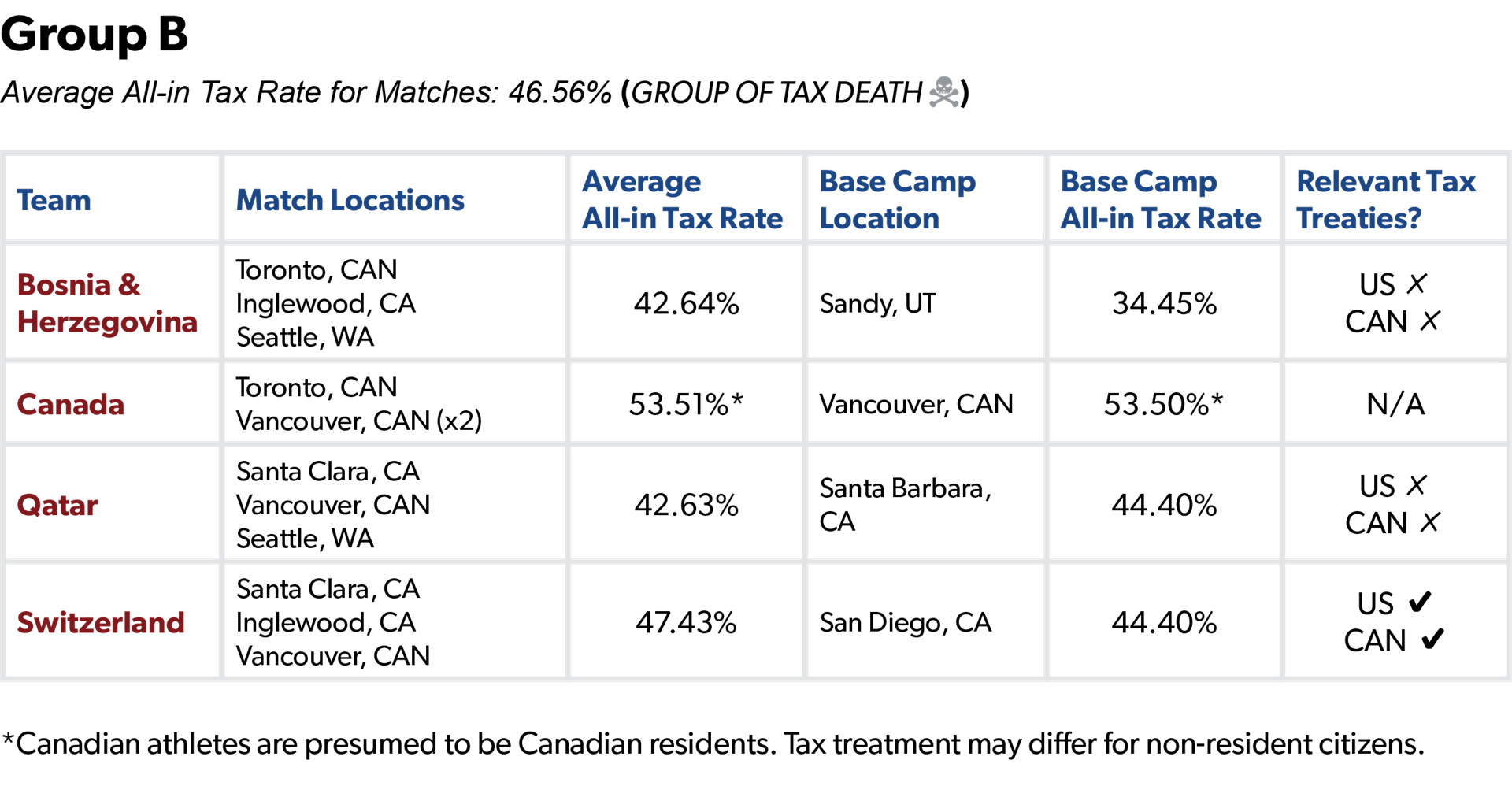

Our unfortunate Group of Tax Death is Group B, which has the bad fortune to play almost all its matches in California or Canada. Bosnia & Herzegovina and Qatar at least get matches in (for now) tax-free Seattle, but neither country has tax treaties with the U.S. or Canada. Bosnia & Herzegovina will hopefully spend most of its time in Utah, which has a state tax rate that is about 1/3rd of California’s and 1/5th of British Columbia’s.

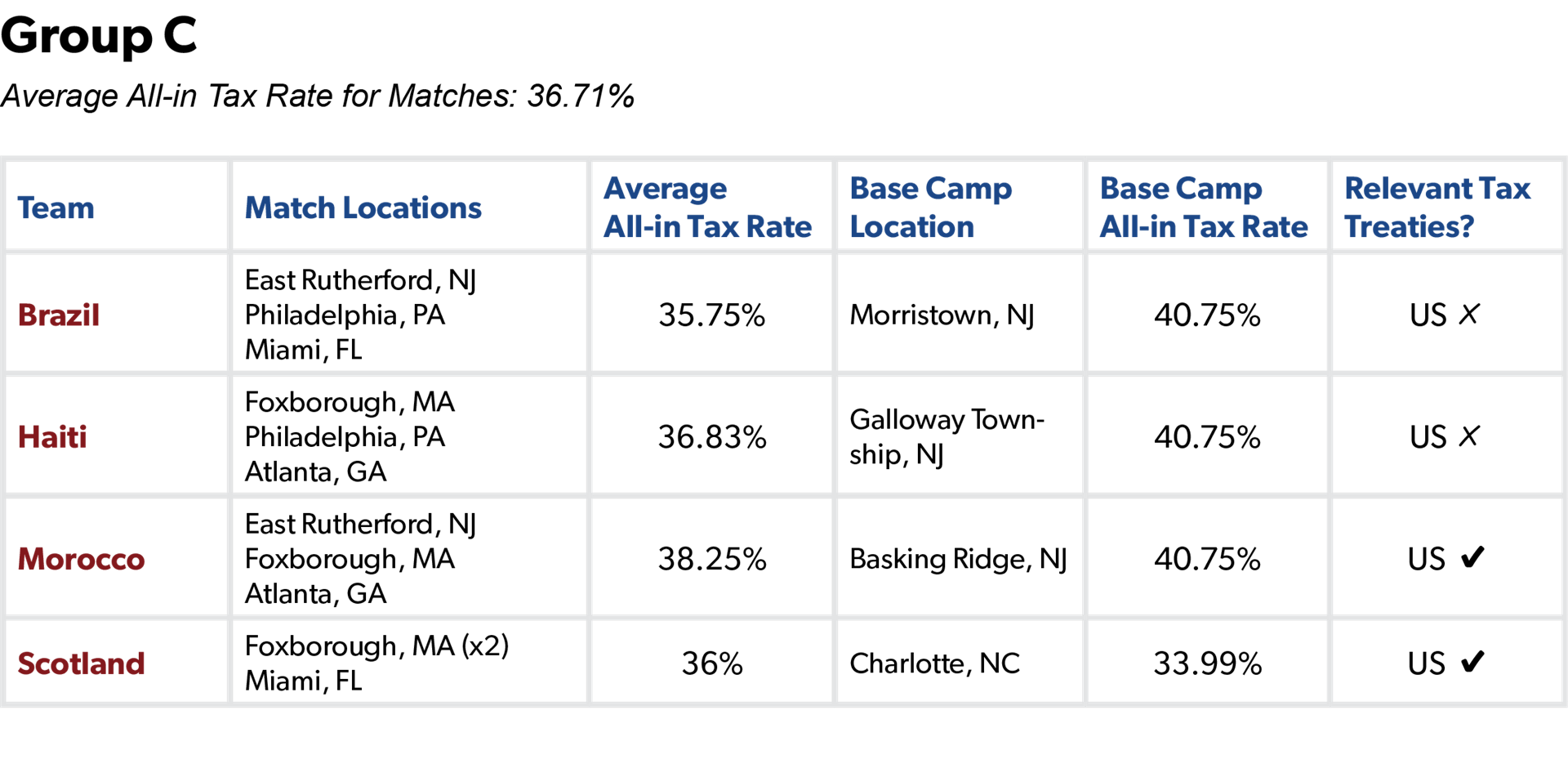

Group C comes in with a fairly middling tax burden. With all matches played in the United States, players will at least enjoy relative simplicity. The choice of New Jersey as a base camp by three of the four teams will hit some players in the wallet, however.

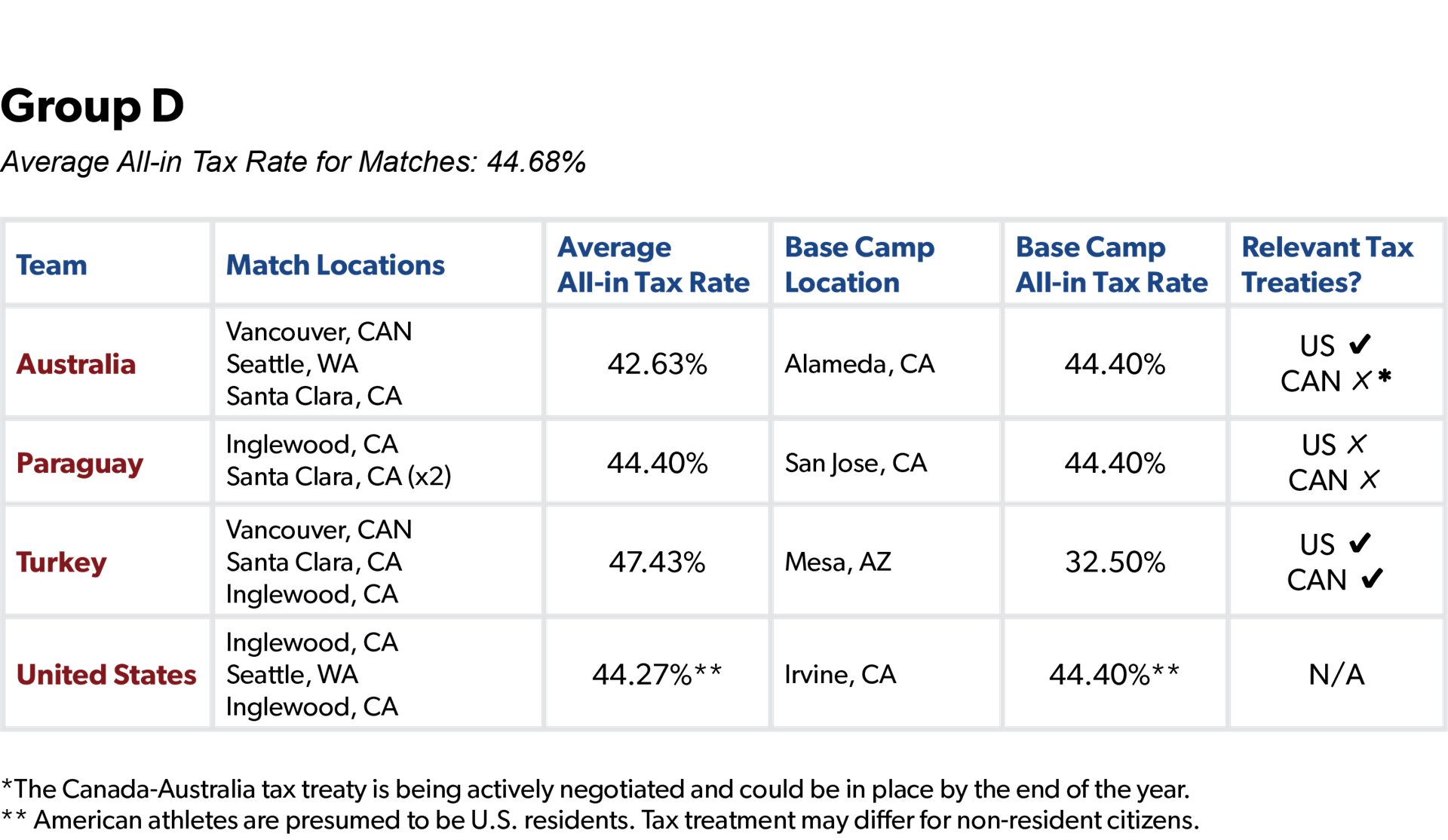

Group D is essentially the California Tax Group, with all but two matches played in the Golden State. With the entire country to pick from, American players won’t thank the United States Soccer Federation for sticking them with California’s taxes. Turkish players, at the very least, benefit from Arizona’s 2.5% state tax rate. Group E, like Group C, comes out with a fairly middling tax burden, with matches in high-tax Canada balanced out by matches in Houston. Base camps were well-selected by each team’s soccer federations, with no teams facing a tax burden over 35.25%.

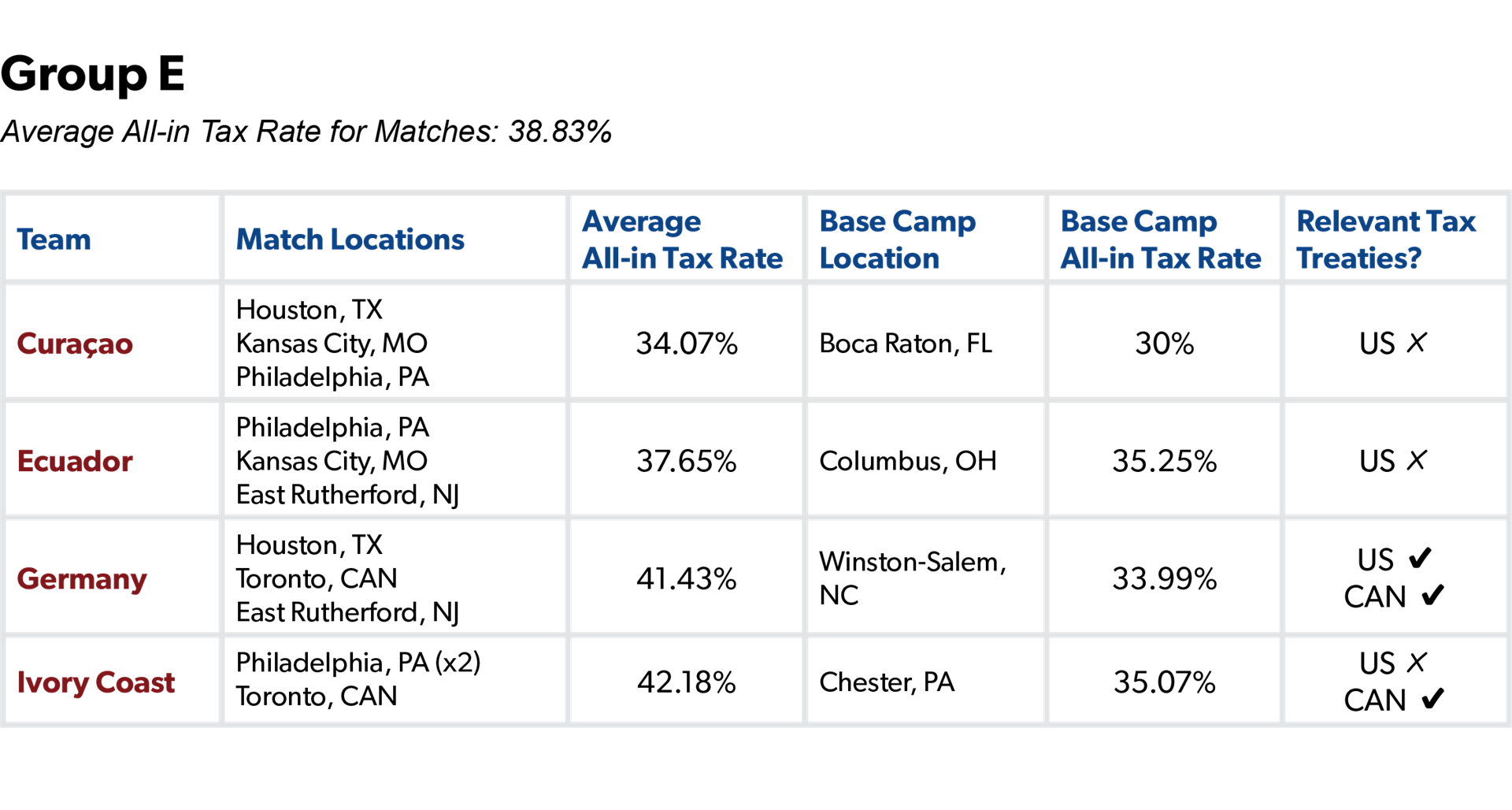

Group E, like Group C, comes out with a fairly middling tax burden, with matches in high-tax Canada balanced out by matches in Houston. Base camps were well-selected by each team’s soccer federations, with no teams facing a tax burden over 35.25%.

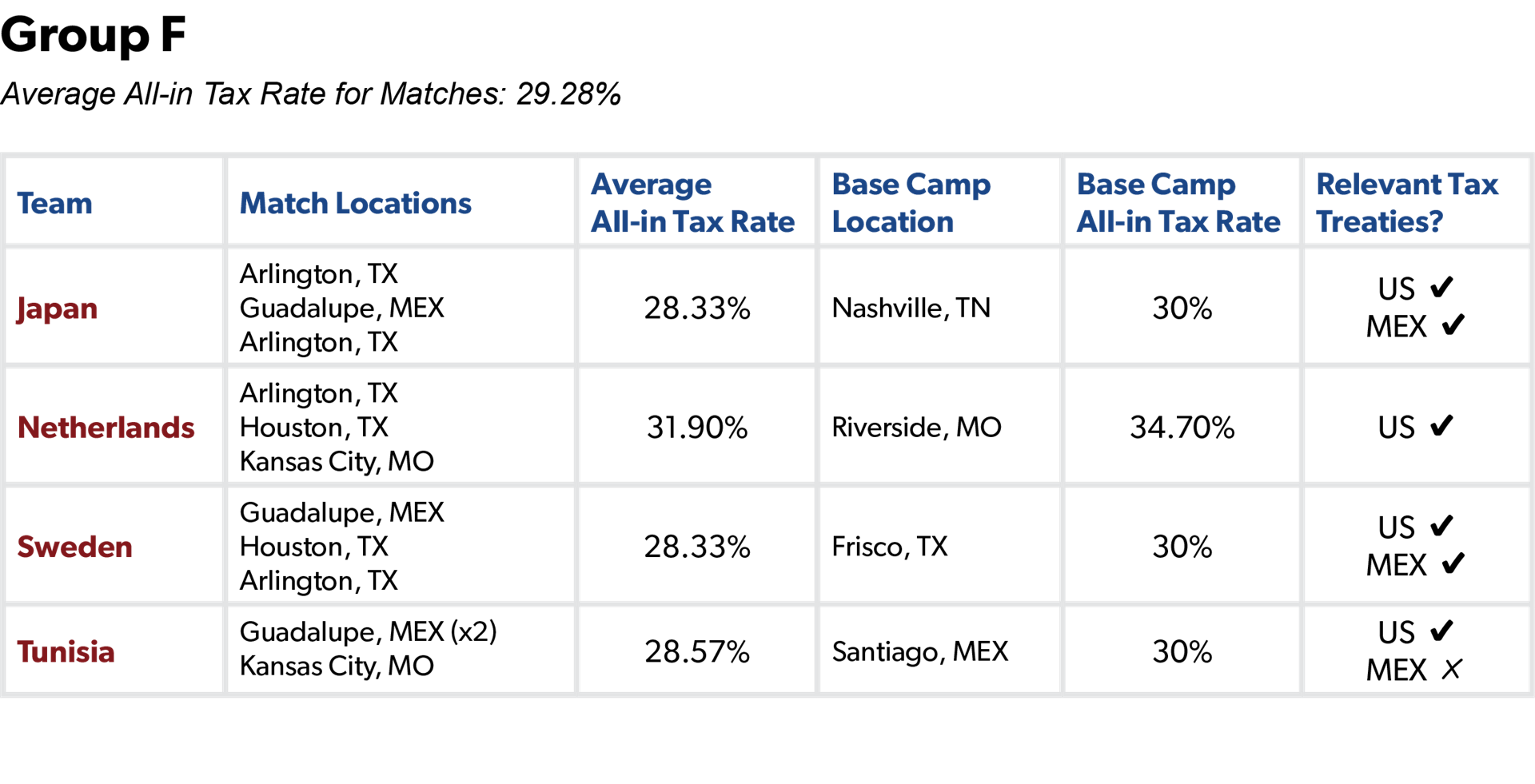

Group F is an honorable mention for the Group of Tax Freedom, having the excellent luck to play all its matches and site all its base camps in Mexico, Texas, or Missouri. Other than Tunisia and Mexico, all teams also have all relevant tax treaties.

Group F is an honorable mention for the Group of Tax Freedom, having the excellent luck to play all its matches and site all its base camps in Mexico, Texas, or Missouri. Other than Tunisia and Mexico, all teams also have all relevant tax treaties.

If the World Cup were taking place in 2029 (when Washington’s 9.9% income tax is set to go into effect), Group G probably would have been the Group of Tax Death. As it is, the two matches being played in Seattle save Group G from that dubious distinction. The Kiwis must have a masochistic streak—not only does New Zealand play all its matches in Vancouver or California, it was also the only team to set up its base camp in California rather than Washington or Mexico.

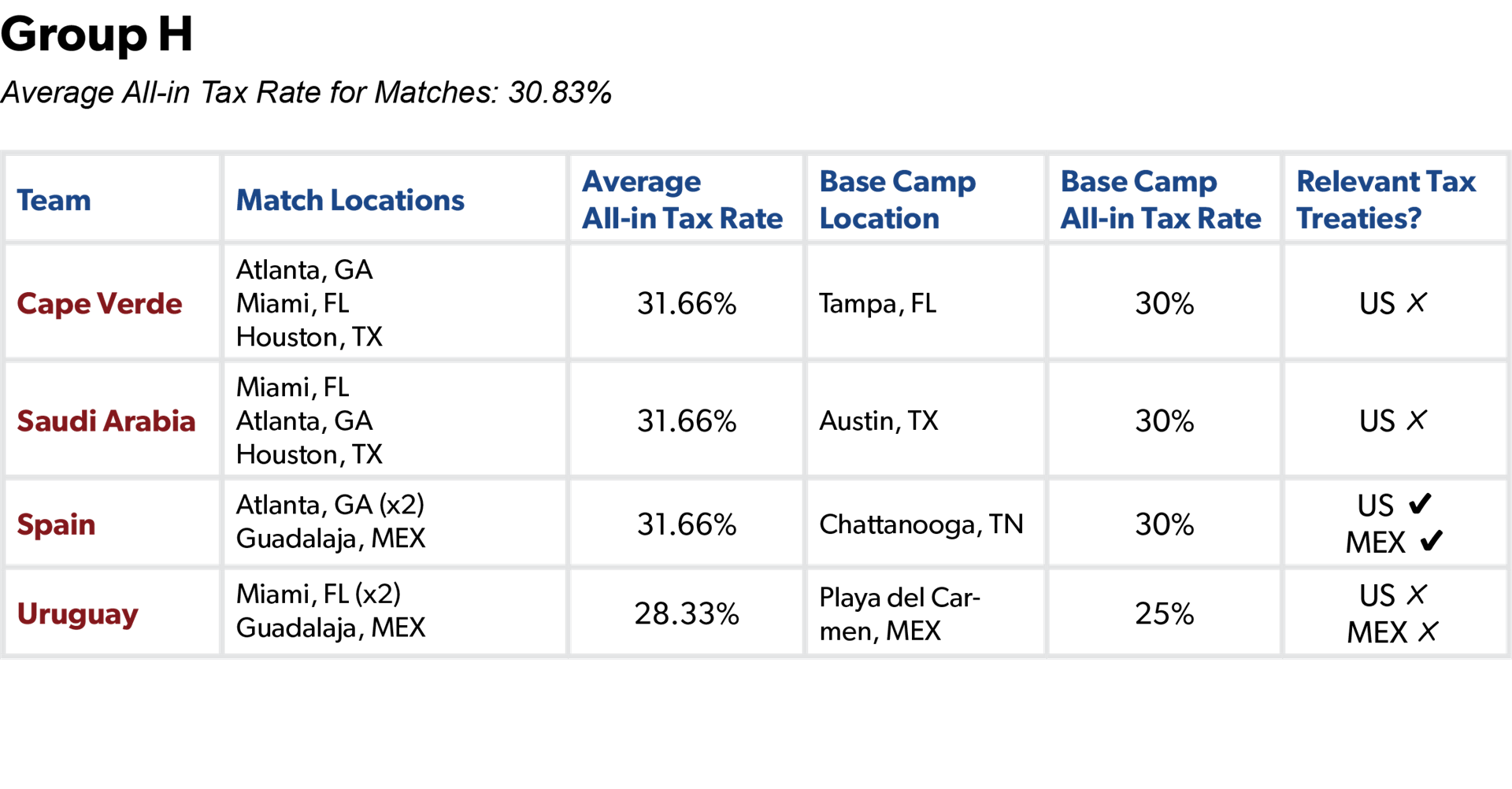

Through two rounds of matches, Group H’s members seem to be big fans of ties. They nearly tied Groups A and K as the Group of Tax Freedom, with the highest-tax location being in Georgia. Nor is there much to separate these teams in terms of the base camps they chose, with each nation in either Mexico or an American state with no income tax.

Through two rounds of matches, Group H’s members seem to be big fans of ties. They nearly tied Groups A and K as the Group of Tax Freedom, with the highest-tax location being in Georgia. Nor is there much to separate these teams in terms of the base camps they chose, with each nation in either Mexico or an American state with no income tax.

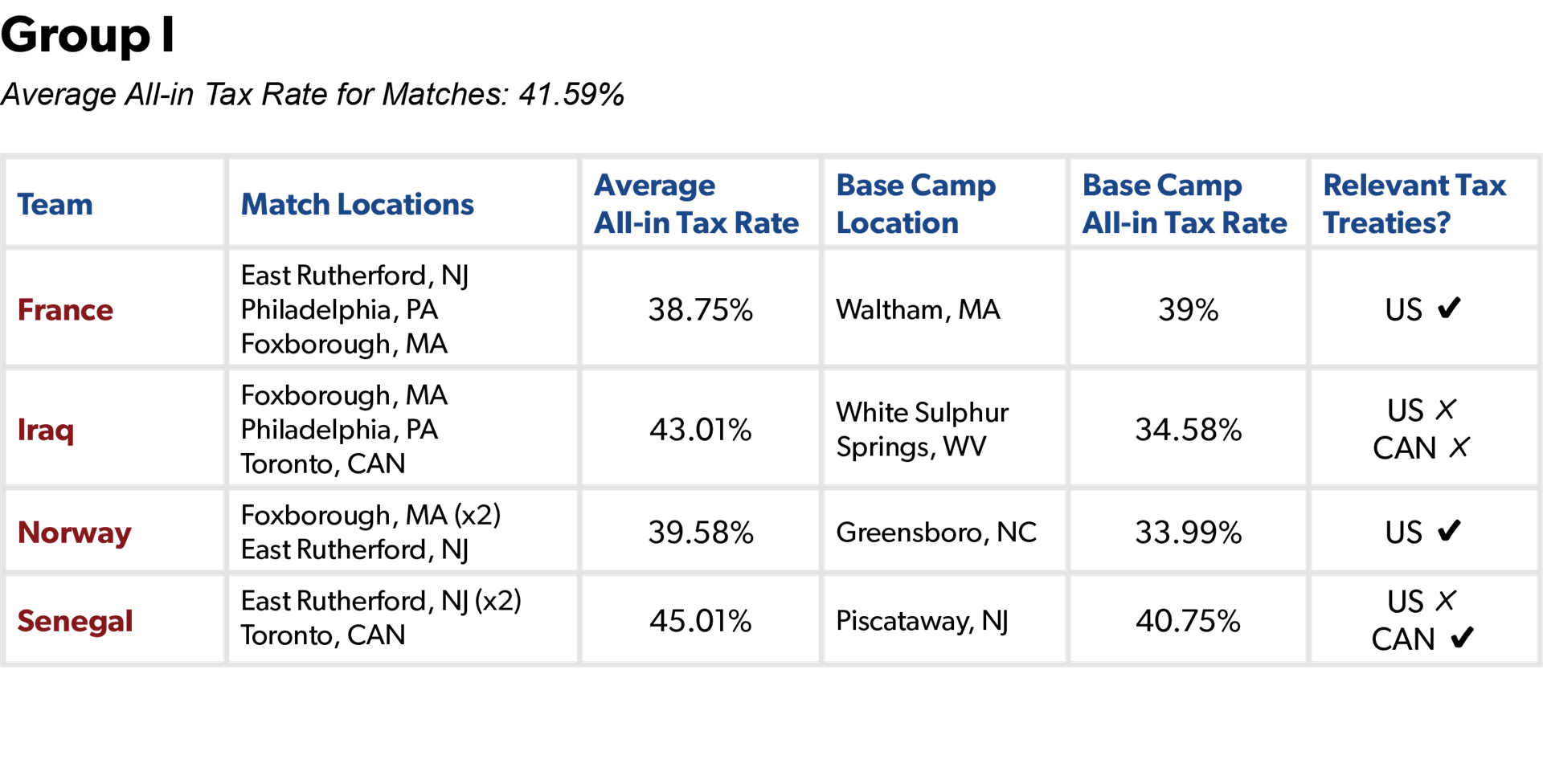

While suffering only one match based in Canada, Group I’s jock tax burden remains fairly high, thanks to all other matches being based in New Jersey, Massachusetts, and Pennsylvania. Iraq and Senegal drew the short stick by having to play in Toronto, where the top combined tax rate reaches 53.53%.

While suffering only one match based in Canada, Group I’s jock tax burden remains fairly high, thanks to all other matches being based in New Jersey, Massachusetts, and Pennsylvania. Iraq and Senegal drew the short stick by having to play in Toronto, where the top combined tax rate reaches 53.53%.

Group J balances moderate Missouri taxes, low Texas taxes, and sky-high California taxes to come out fairly average. The Austrian Football Association presumably chose to base its players out of California to avoid having its players discover how much lower American taxes are than Austria’s, and refuse to board the plane back.

Group J balances moderate Missouri taxes, low Texas taxes, and sky-high California taxes to come out fairly average. The Austrian Football Association presumably chose to base its players out of California to avoid having its players discover how much lower American taxes are than Austria’s, and refuse to board the plane back.

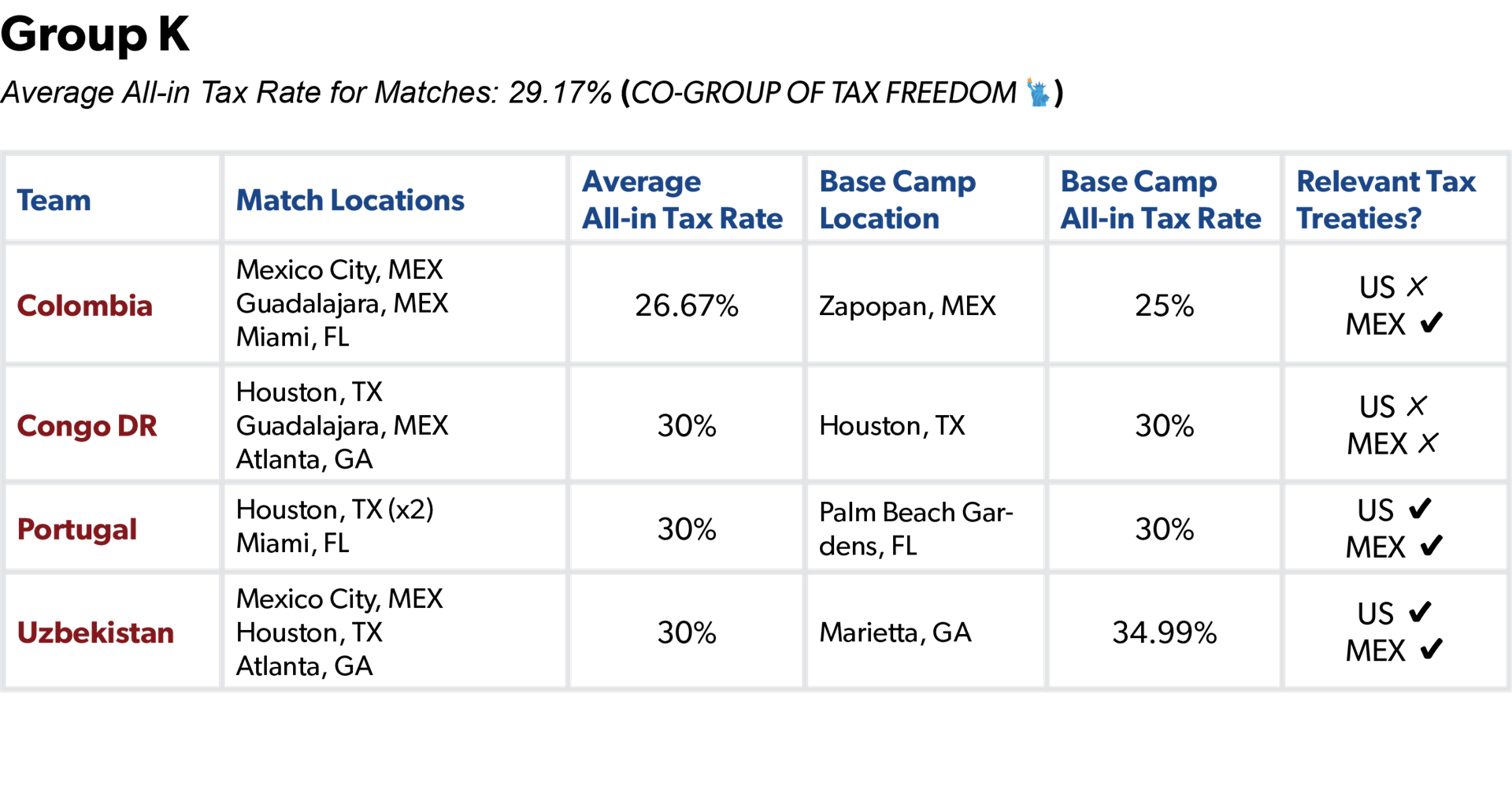

Group K is our Co-Group of Tax Freedom, along with Group A, thanks to a multitude of matches played in either Mexico, Texas, or Florida. Georgia represents the highest-tax location any of the teams will have to deal with, despite the state’s modest 4.99% rate. Portugal and, perhaps somewhat surprisingly, Uzbekistan, have all relevant tax treaties.

Group K is our Co-Group of Tax Freedom, along with Group A, thanks to a multitude of matches played in either Mexico, Texas, or Florida. Georgia represents the highest-tax location any of the teams will have to deal with, despite the state’s modest 4.99% rate. Portugal and, perhaps somewhat surprisingly, Uzbekistan, have all relevant tax treaties.

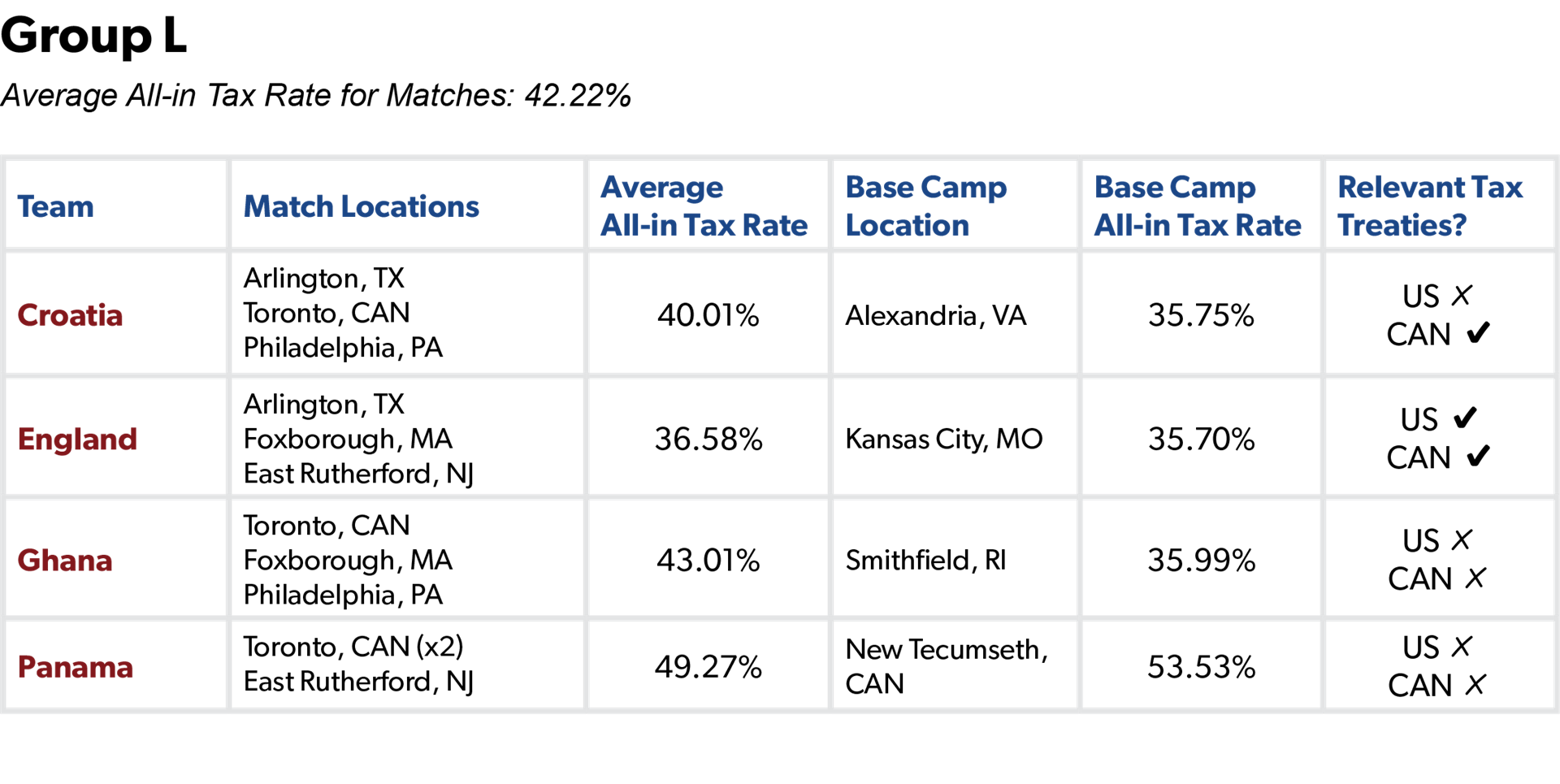

Group L’s saving grace is a single match between Croatia and England in tax-free Texas. Otherwise, it’s nothing but tax pain, with matches in Toronto, Massachusetts, and New Jersey. The Panama soccer team needs to keep a closer eye out for black cats, broken mirrors, and spilled salt, dealing with not only two matches in Toronto and a third in New Jersey, but also a base camp in Ontario.

Group L’s saving grace is a single match between Croatia and England in tax-free Texas. Otherwise, it’s nothing but tax pain, with matches in Toronto, Massachusetts, and New Jersey. The Panama soccer team needs to keep a closer eye out for black cats, broken mirrors, and spilled salt, dealing with not only two matches in Toronto and a third in New Jersey, but also a base camp in Ontario.

Conclusion

Of all teams at this year’s World Cup, the unluckiest are New Zealand and Panama.2 New Zealand faces a higher jock tax rate at matches, though the Panamanian team’s decision to base out of Ontario will mean that the Panamanians will face the highest overall jock tax rate.

Yet, while this has been a somewhat lighthearted exercise, the fact remains that navigating this intricate web of tax rules will be far more manageable for highly-paid soccer stars than it will be for underdog players earning modest salaries, as well as coaches and staffers for smaller teams. Greenback Tax Services estimates that the cost of hiring a professional to handle tax compliance for a player can be between $5,000 and $15,000. Kylian Mbappé and Erling Haaland may accidentally drop that amount of money and judge it not worth the effort to pick up, but for players and coaches on this year’s Cinderella teams, that is a significant expense.

So, as you watch the rest of this year’s matches, remember that everyone is a winner. Especially the tax accountants.

1 The exact amount that would be taxable in the United States is dependent on how much of his endorsement income is dependent upon playing in certain events and competitions. An advertising deal may not be subject to jock taxes if it has no conditions, but his salary, performance bonuses, and tournament bonuses would be.

2 The Canadian team’s tax rate will be even higher, but that’s their own fault.