Just three years ago, Washington legislators passed a new 7% tax on capital gains income, despite courts and voters long holding that the state constitution bans income taxes. Calling it an “excise tax on capital gains,” proponents managed to hoodwink the state Supreme Court into overturning a lower court decision striking down the tax. Now, emboldened by this piece of legislative legerdemain, state legislators are trying to deal with the latest consequences of rampant overspending by dropping all pretense and simply enacting an income tax.

Background: S.B. 6346 and the Washington Constitution

As of this writing, S.B. 6346 has passed the state Senate by a narrow 27-21 margin, and now must pass the state House before going to the governor. Democratic Governor Bob Ferguson is a strong supporter of the new tax and has indicated that he will sign it if it makes it to his desk.

S.B. 6346 would institute a new 9.9% tax on income, with a $1 million standard deduction, regardless of the taxpayer’s filing status, serving to restrict the tax to millionaires. This new standard deduction would be indexed to inflation. Nonresidents would multiply the standard deduction by a percentage equal to the ratio of Washington income to federal income. If passed, the tax would go into effect in 2029.

The key obstacle to implementation of the new tax, assuming it passes the House, is the prohibition in the state’s constitution against non-uniform taxes. The relevant portion of the state constitution reads: “All taxes shall be uniform upon the same class of property . . .”. As if to forestall an interpretation of this provision that excludes income, it goes on to state:

“The word ‘property’ as used herein shall mean and include everything, whether tangible or intangible, subject to ownership.”

These provisions have been consistently interpreted to forestall the imposition of a tax on income in the state of Washington, most notably in Culliton v. Chase (1933). Due to Culliton, Washington law treats income as property. (Technically Culliton allows for Washington to impose a flat, 1% tax, as this would be uniform and not exceed the state’s constitutional prohibition against property tax rates in excess of 1%).

Voters have rejected income tax proposals at the ballot in 1934, 1936, 1938, 1942, 1944, 1970, 1972, 1975, and 2010.

An odd wrinkle is that Democrats in Washington’s legislature signed into law a ban on income taxes back in 2024. This, however, was done to forestall a ballot initiative that had a high likelihood of earning voter approval and would be difficult to circumvent. S.B. 6246 simply exempts this new millionaire tax from that ban.

A Further Nail in Washington’s Coffin

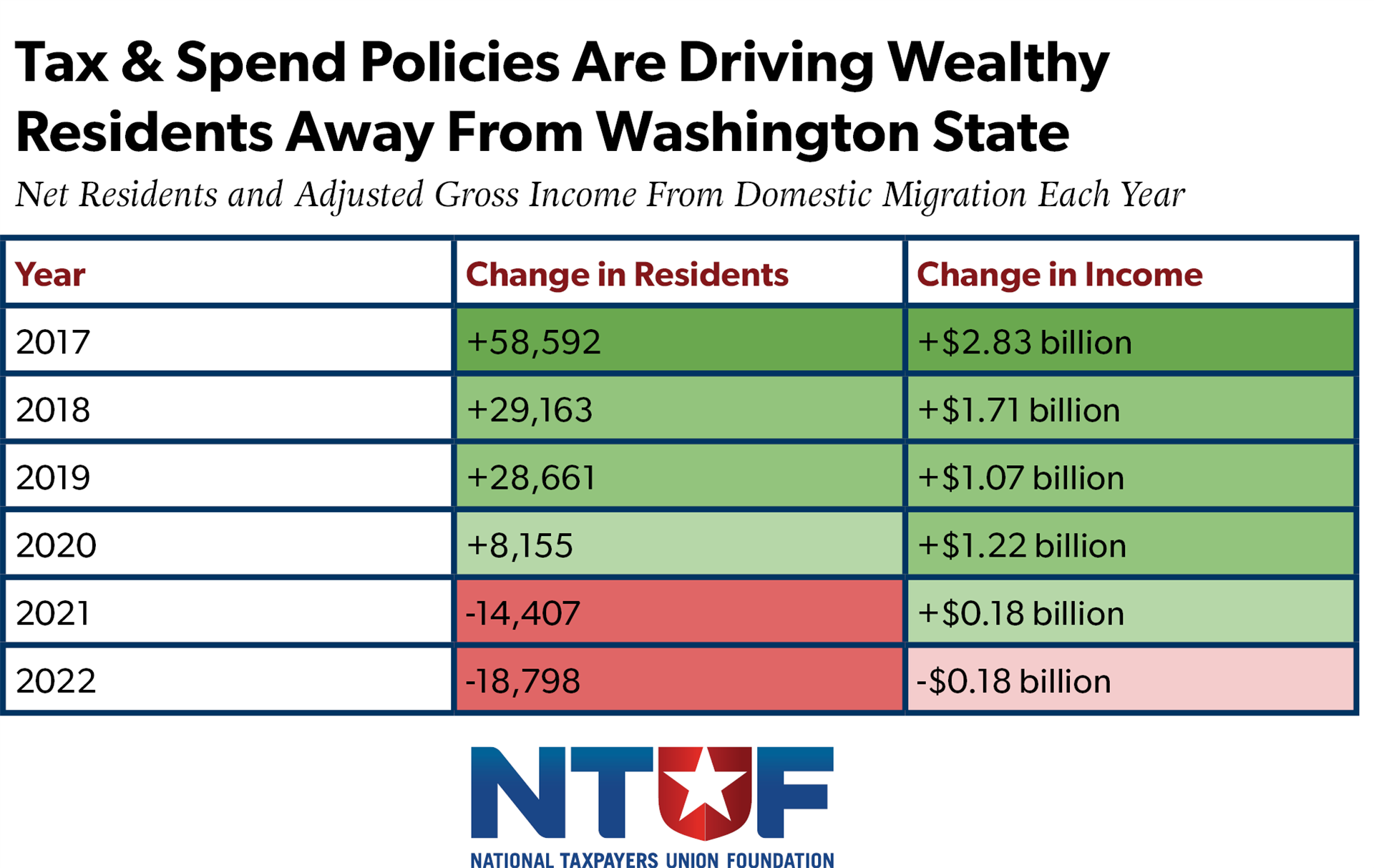

No state is a better case study in how tax-and-spend policies can devastate a once-prosperous and competitive state than Washington. Before 2020, Washington consistently gained more new residents from interstate migration than it lost. Starting in 2017, that positive trend rapidly began to slow, then flip upside down.

Of the nine states without an income tax, only Alaska and Washington were net migration losers in 2022—and Washington is not located in a frozen tundra hundreds of miles away from the contiguous United States.

Coinciding with this exodus is a sudden and stark pivot toward tax-and-spend policies. Between FY2005 and FY2016, state budgets increased by an average annual rate of 4.1%. From FY 2017 through the end of this year, budgets have increased by more than double that amount—an average of 9.2%. Tax collections are set to more than double between 2017 and 2029, even before factoring in this new income tax.

Should it be passed into law and survive legal challenges, the millionaire’s tax will only exacerbate these trends. The state assumes that 21,000 millionaires will pay the tax, but further out-migration may make that an overestimate. Many of those millionaires are business owners who would be liable for the new tax on “pass-through” income, and a recent survey by the Association of Washington Businesses found that a stunning 44% of Washington business owners are looking to relocate their personal residence to other states ahead of the new millionaire’s tax, while a further 17% are considering moving their businesses.

Other progressive policies have also blown up in Washington’s face. A law passed last year that subjects digital advertising to the state’s sales tax, a business input that should not be subject to taxation. A 2024 state law setting a special minimum wage for rideshare drivers has led to Washington having the most expensive Ubers in the nation. A 2024 Seattle law setting the minimum wage for gig economy delivery drivers at about $26, significantly higher than other workers, led to no benefit for drivers as the increased pay-per-order was offset by a drop in order volume, leading to drivers having more unpaid time idling and waiting for a delivery.

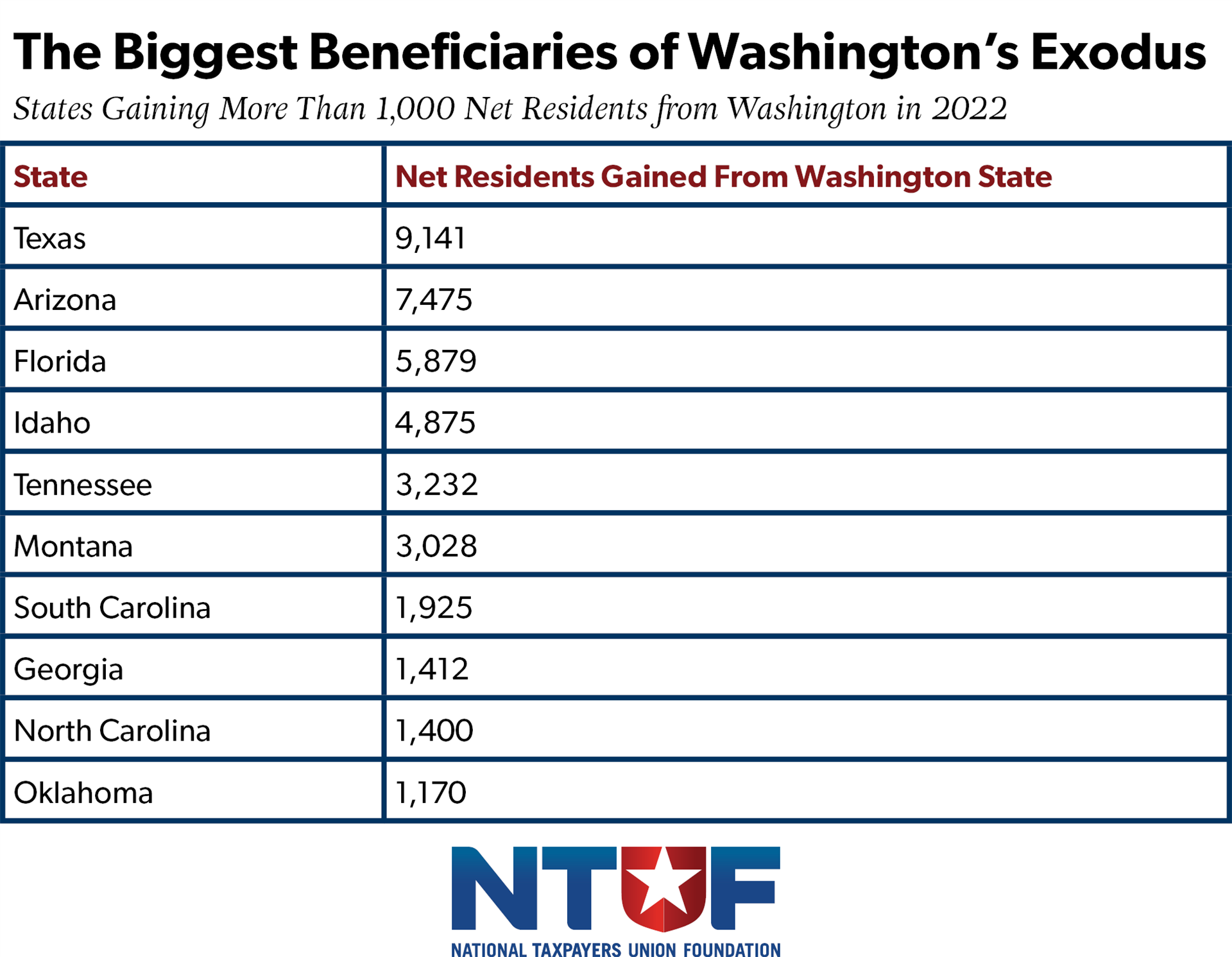

Washington should be profiting from the follies of other West Coast states, with the bar to be more competitive than California or Oregon practically on the floor. Yet, while Washington gained about 21,000 residents on net from these two fellow coastal states in the latest IRS data, it lost even more to three states that are nowhere close: Texas, Arizona, and Florida. Other major beneficiaries of Washington’s generosity include Idaho, Tennessee, and Montana.

Conclusion

At this point, Washington reversing course would only limit the damage, not undo it. Even should the tax ultimately be shelved, Washingtonians have to know by now that their representatives’ efforts to levy new taxes to fuel their spending addiction will only continue.

Even so, Washington is uniquely positioned, both geographically and in terms of tax policy, to set itself up as a major beneficiary of the California exodus. Unfortunately, that window of opportunity shrinks with every new foolish tax put forward by the legislature.