(pdf)

Introduction

The President and Congress are set to approve a budget deal that significantly increases spending caps, employs bogus offsets years from now against upfront spending hikes, and suspends the debt ceiling for an unprecedented two years. Worse, it provides no budget restraint regime as a successor to the 2011 Budget Control Act (BCA) that imposed the caps in the first place. In total, this bipartisan spending spree will wipe out 40 percent of the BCA’s savings per household, delivering a lethal blow to one of the few landmark deficit reduction achievements in the modern era.

The Budget Control Act: A Rare Moment of Restraint in Federal Spending

Back in 2011, the federal government had run up against a statutory debt ceiling of $14.3 trillion, preventing the Department of the Treasury from issuing new debt to finance deficit spending. From Fiscal Years 1998 through 2001, the budget recorded a surplus but has been in deficit every year since. Outlays soared during the first two years of the Obama Administration. The trifecta of a spike in welfare-related spending triggered by the recession, along with enactment of the ten-year $604 billion “stimulus” act in 2009 and the trillion-dollar Affordable Care Act (ACA) in 2010 pushed annual deficits over $1 trillion.

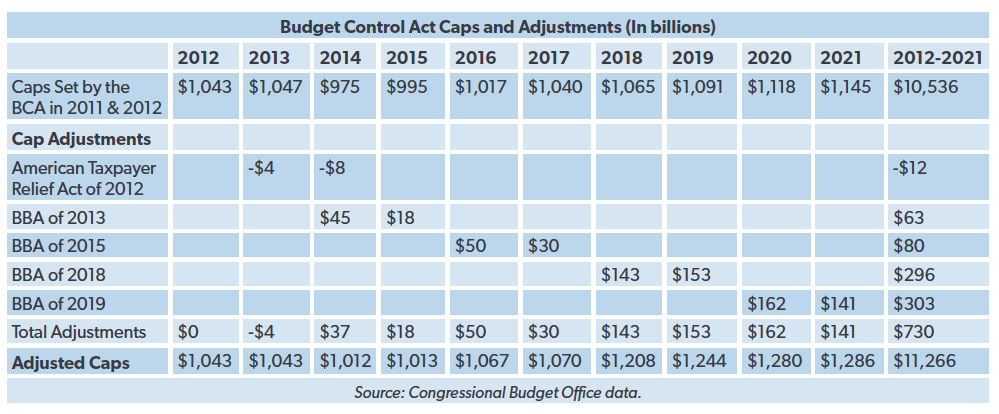

When President Obama sought an increase in the debt ceiling, he faced a much different political environment than during his first two years when his party controlled the House and Senate. In reaction to the budget crisis, the “Tea Party” movement was ascendant in 2010 and the midterm elections saw an influx of fiscally conservative members elected to Congress. After months of tense brinkmanship, lawmakers crafted the Budget Control Act of 2011, a grand compromise with the President to impose a regime of fiscal discipline in exchange for a $2.1 trillion increase in the debt ceiling. The BCA set statutory caps on spending through FY 2021 which were enforceable through “sequestration,” or automatic across-the-board spending cuts. It also established a joint committee to produce a plan including at least $1.5 trillion in deficit reduction. The failure of the committee triggered a further cap reduction and sequestration.

The law was the most significant spending reform enacted in decades and helped reset spending to a lower baseline. Unfortunately, it did not take long before lawmakers started to find ways to erode the spending restraints. Legislation was enacted to boost the caps in each year from 2014 through 2019. Before this deal, the Congressional Budget Office (CBO) estimated that lawmakers have made a total of $439 billion in adjustments to enable higher spending.

The Bipartisan Budget Act of 2019: Restraint Be Damned

The new budget deal, known as the Bipartisan Budget Act of 2019 (BBA 2019) erases the last two years of remaining BCA caps, allowing for base spending of $1.288 trillion in 2020, with $667 billion for defense and $622 for non-defense. Levels would be increased further in 2021 to $1.298 trillion, providing $672 billion for defense and $627 billion for non-defense.

The deal provides outlays for Overseas Contingency Operations (OCO) funding of $72 billion for defense in 2020 and $69 billion for 2021 and $8 billion in each year for non-defense OCO-related spending, which includes State Department and foreign affairs programs. The deal also provides $2.5 billion in 2020 for conducting the decennial census. OCO’s ostensible purpose is to fund ongoing military operations in Iraq and Afghanistan, but it has long been used a “slush fund” to skirt budget rules in order to increase defense spending. CBO found that since 2012, 60 percent of OCO funding has been for “enduring activities including funding explicitly identified for base-budget activities—that could have been incorporated into the department’s base budget but were not.” By funneling this money through OCO, the funding is not subject to the BCA caps.

Compared to the statutory caps for the next two years, the budget deal would allow for a total of $322 billion in higher base spending ($169 billion in 2020 and $153 billion in 2021). By comparison, House Budget Committee Chairman Yarmuth’s plan would have boosted spending levels by $357 billion over the two years, while Senate Budget Committee Chairman Enzi’s budget draft would reduce non-interest mandatory spending by $551 billion over the next five years.

This will also enable $1.7 trillion in higher spending to get baked into the rest of the ten-year budget baseline. Once these new levels become law, CBO will update its current-law baseline projection to account for the changes. CBO’s discretionary projection of the baseline will carry forward the statutory FY 2021 cap level with annual adjustments for inflation.

In 2017, NTUF used data from the Congressional Research Service to calculate that the BCA spending caps and related reductions in net interest costs on the debt resulted in savings of $16,463 per household. Revising those figures to account for the cap increases enacted since then, and also accounting for smaller net interest savings, finds $9,964 in savings per household – wiping out 39 percent of the savings.

The Cap Increase Compared to Current Policy

The caps that the new BBA dispenses with were effectively doomed when Congress started increasing them in the Bipartisan Budget Acts of 2013, 2015, and 2018. These all boosted statutory caps in years prior to 2020, making the ostensible reintroduction of much lower caps in 2020 and 2021 untenable to spendthrift politicians. This is especially true given the combination of Republicans wanting to boost defense spending and Democrats demanding similar increases for non-defense spending.

Sure enough, rather than allowing lower caps to return in 2020 and 2021, the new agreement continues Congress’s post-2011 spending spree. Relative to 2019 enacted levels for base spending and OCO, reflecting a more realistic baseline based on current policies as opposed to current law (which tends to over-report revenues that won’t manifest and under-reports spending levels because of its myopic methodology) the BBA 2019 deal would boost spending by $49 billion in 2020 and an additional $5 billion more in 2021.

Will Lawmakers Show Restraint in 2021?

It is likely that lawmakers will also revisit the relatively meager increases allowed for in 2021. Including OCO and Census funding along with the base cap increases, BBA 2019 allows for $1.37 trillion in funding for FY 2020. Relative to that, 2021 spending would increase by just $5 billion, or 0.4 percent. Much as the previous 2020 cap was untenable politically, this 2021 cap will likely not survive for myriad reasons.

During negotiations over the deal, Speaker of the House Nancy Pelosi sought to increase levels in the bill by $22 billion for the VA MISSION Act of 2018 that established a Community Care program for veterans. Last year, lawmakers sought to exclude the funding from caps. There will likely be a renewed push for higher spending for the program on top of the Veterans’ Administration’s base budget.

Congress is also still enacting new spending bills that will have to be accounted for. On the same day that the deal was announced, the Senate approved the House-passed permanent extension of the September 11th Victim Compensation Fund. CBO projects that this will cost $1.4 billion in 2021 and $10.2 billion over the next ten years.

The BCA also provides for adjustments to the spending caps for OCO, emergency spending, and disaster aid. In addition to these exemptions, the BCA has been subsequently amended to allow for higher spending outside of the spending caps for fire suppression and certain spending under the 21st Century Cures Act. There is an ongoing push to create another cap exemption for billions in new spending through the Harbor Maintenance Trust Fund. This spending may be excluded from caps, but they still contribute mightily to annual deficits. Taxpayers should be forewarned against such gimmicks.

Dubious Offsets

The deal does include three offsetting provisions providing for an estimated $77 billion in savings, but these are suspect and problematic for a number of reasons.

Two of the offsets are user fees that are already in place to finance spending for specific governmental services. The first is an extension of Customs User Fees assessed on commercial vessels, trucks, aircraft, and passengers arriving at ports of entry to cover the cost of certain customs services. The Government Accountability Office pointed out that there is a misalignment between the custom inspection activities and the statutory uses of the customs fees: “not all of the activities that may be funded from the customs fees are associated with conducting customs inspections, and not all customs inspection activities are reimbursable (i.e., can be covered by funds from the user fee account).” The fees are only available to fund a limited list of inspection activities and also for deficit reduction.

BBA 2019 also extends Merchandise Process Fees under section 503 of the U.S.-Korea Free Trade Agreement Implementation Act. As described in a committee report on the enacting legislation, these fees are intended to “offset the salaries and expenses that will likely be incurred by the Customs Service in the processing of entries and releases.”

Counting these user fees as offsets against unrelated spending is an abusive accounting gimmick. But the problem is even worse: these fees are currently in effect through 2027, but the budget deal extends them through 2029. This means that the drafters are counting offsets nine and ten years from now - again, for fees in place for specified services - against spending hikes over the next two years. Reformers should put an end to this oft-used gimmick.

The third offset included in the budget deal would similarly extend mandatory spending reductions for two years beyond their expiration in 2027. BCA also provided for sequestration of certain mandatory programs. Programs including Social Security, Medicaid, and Temporary Assistance for Needy Families are exempt from these reductions. According to the Office of Management and Budget, the mandatory sequester saved $18 billion in 2018. CBO estimates that this provision in the deal would decrease outlays by $17.1 billion in 2028 and $28.7 billion in 2029.

History teaches that taxpayers should be skeptical that Congress will keep these savings in place. Congress had already taken multiple stabs at clawing back the BCA’s savings before this final blow to the discretionary caps. There are many other examples of intended savings that failed to materialize because they were either scoring tricks or were repealed before they were implemented, including:

The ACA’s Independent Payment Advisory Board and CLASS Act, both of which were included drafted in the law to provide offsets to the massive new spending and ease its passage. But they were both repealed before they were implemented. There were grave concerns that IPAB would impose rationing and price controls if its authority was ever triggered. The CLASS Act started collecting offsetting receipts from enrollees years before benefits would start paying out, but the program turned out to be entirely unsustainable. It was shelved by the Obama administration and then wisely repealed by Congress.

The Balanced Budget Act of 1997’s Sustainable Growth Rate to check the growth in Medicare physician payment rates. However, this resulted in a ritual of passing regular “Doc Fixes” to prevent the cuts from taking place, until it was replaced in 2015 with automatic increases for all doctors through 2019 (succeeded by a Merit-Based Payment Incentive System).

Boost in the Debt Ceiling

A central provision of the deal, and one of its worst features, is an unprecedented two-year suspension of the debt ceiling until August 1, 2021. While an imperfect instrument, the debt ceiling is one of the few reminders to lawmakers that the government is financially overextended.

In the past, Congress would raise the debt ceiling by a set amount. In some cases, such as the BCA or the Balanced Budget and Emergency Deficit Control Act of 1985, the increases were paired with deficit reduction plans. The trend lately is to instead suspend the debt ceiling for a defined period of time. While the limit is suspended, the Treasury can issue new debt to finance deficit spending and when the suspension expires, the debt ceiling is re-established at the total amount issued at the time.

The duration of the suspensions has been growing longer as Congress punts on fiscal responsibility while administering its power of the purse. Back in 2013, the ceiling was only suspended for a few months and in 2014, for just one month. However, the Bipartisan Budget Act of 2015 suspended the debt limit for 18 months. The BBA 2019 plan suspends it for a full two years, a record-setting punt on the part of Congress.

Conclusion

President Trump’s own FY 2020 Budget warns, “We must protect future generations from Washington’s habitual deficit spending.” This budget deal effectively kills off the last vestiges of the signature spending restraint law of the new millennium. The spending increases coupled with dubious offsets is doubly concerning given the long-term budget outlook. Earlier this year, CBO published an analysis of the budget if current law spending and revenues are extended out over the next three decades. Under that scenario, federal debt grows from 78 percent of GDP this year to 144 percent by 2049. But under an alternative scenario taking into account current policies, debt would be on track to grow to 175 percent of GDP in that timeframe. A lot of lip service is paid to addressing the debt crisis, but little is actually accomplished.

There are lots of warnings that without a serious course correction to tackle the growing debt, the government will soon reach a tipping point, triggering a loss of confidence in the dollar, soaring interest rates on financing and issuing debt, leading to economic contraction. Nobody knows exactly when this might occur, but the risk of this tipping point is that we will become aware of it only after it has been passed.

With this new budget deal, Congress has gutted one of its most significant recent achievements and put the federal government on even shakier financial footing.