(pdf)

Introduction

A new bill in the House of Representatives lays bare the brazen attempts to manipulate the Congressional Budget Office’s scoring process through a harbor maintenance funding gimmick. The legislation would exclude harbor maintenance funding from discretionary spending limits, creating a significant loophole through which to drive higher spending. CBO published a cost estimate of the bill which concluded that it would have zero impact on budgetary outlays or the deficit. This defies common-sense assumptions about the spending that would occur if the bill is enacted.

What the Legislation Would Do

Representative Peter DeFazio (D-OR), Chairman of the House Transportation and Infrastructure Committee, has sponsored H.R. 2440, the Full Utilization of the Harbor Maintenance Trust Fund Act. The bill would provide that spending from the HMTF would be excluded from discretionary spending limits. The Budget Control Act of 2011 set caps on spending that remain in effect through 2021. Congress has voted many times already to override the caps and talks are underway to try and eviscerate the remaining budgetary restraints. While they are still in effect, Section 251(b) of the Balanced Budget and Emergency Deficit Control Act allows for adjustments to the caps for certain spending:

- spending designated as “emergency” and “overseas contingency operations;”

- disaster funding;

- continuing disability reviews and redeterminations;

- health care fraud and abuse control;

- reemployment services and eligibility assessments; and

- wildfire suppression.

The emergency and disaster designations are so that Congress could react swiftly to emergencies but are in need of reform to limit their use for spending that should be included in the base budget and to find ways to offset deficit spending. The overseas contingency operations account has been used to fund the wars in the Middle East but has since become a slush fund. The latter four designations are spending that ostensibly lead to savings by reducing fraud and abuse, additional welfare payments, and mitigation. H.R. 2440 would add HMTF as a new category of spending under this section to enable higher spending levels without the need for offsets elsewhere.

The HMTF is financed by an ad valorem tax on imported goods, levied in 1986 at a rate of 0.04 percent. Congress appropriates money from the HMTF for U.S. Army Corps of Engineers’ operation and maintenance of harbors. The tax was increased to 0.125 percent in the Omnibus Budget Reconciliation Act of 1990, a package of revenue increases and spending reductions to reduce the deficit. The Congressional Research Service notes that the tax was increased to “recover 100% of the Corps’ port [operation and maintenance] expenditures." Lately, the annual spend-rate from the Fund is far less than the tax revenues deposited in the Fund. According to CBO, it currently has an unappropriated balance of $9 billion.

Attempts to Abuse HMTF Aren’t New

As far back as 1996, the so-called Truth in Budgeting Act would have exempted HMTF and other transportation funding from any spending limitations. Earlier this year, Senator Shelby sought to add a spending loophole for the HMTF as amendment to the disaster aid package. But this had nothing to do with emergency aid or disaster relief. Furthermore, Senator Enzi pointed out that it would lead to billions in additional deficit spending. Shelby eventually agreed to withdraw the amendment.

The Water Resources Development Act of 2018 initially included a provision to allow for spending from the HMTF without appropriations starting in 2029 – just outside of CBO’s ten-year scoring window. CBO’s score estimated this “would significantly increase direct spending by more than $2.5 billion and on-budget deficits by more than $5 billion in at least one of the four consecutive 10-year periods beginning in 2029.” In part as a response to this scoring issue, the provision was stripped from the bill as it moved forward.

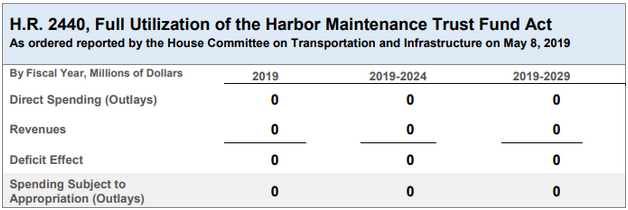

CBO’s Cost Estimate for H.R. 2440

Starting earlier this year, the top of each of CBO’s cost estimates shows a table depicting the overall impact on spending and deficits by the bill analyzed. The table in the score of H.R. 2440 is replete with zeros:

It is clearly the intention of the sponsors of this legislation to increase federal spending from the HMTF. In a summary of a draft of the bill, they wrote that it would provide for an additional $34 billion in funds for harbors. Despite the obvious motivation to use HMTF as a vehicle for spending hikes, CBO’s zero score reflects a myopic reading of the bill.

The legislation would establish a loophole for higher spending, but that higher spending would occur as a result of subsequent legislative action. CBO effectively ends its analysis after the first step in this two-step process, thus ignoring the stated goals of sponsors to boost spending significantly. CBO notes hypothetically, “if H.R. 2440 were enacted and the Congress subsequently enacted appropriation bills that otherwise were equal to the new caps—including appropriations from the HMTF—then in 2020 and 2021 up to $10 billion more could be appropriated from the HMTF for that period without exceeding those caps. But CBO has no basis for predicting the total budget authority that will be provided in future appropriation acts.”

In situations where CBO is uncomfortable forecasting future Congressional action, it should produce a score indicating that the impact on outlays and the deficit is “unknown,” “not applicable,” or “to be determined.” A zero score gives a misleading impression that legislation such as this has no more impact on federal spending than a proposal commemorating a post office.

This is an important scoring point because there are several other proposals to exclude favored types of spending from the budget caps:

H.R. 2021, the Investing for the People Act, would exempt Census and Internal Revenue Service enforcement spending from budget caps. H.R. 2401 and S. 1250, the American Cures Act, would exempt research expenditures at the National Institutes of Health, Centers for Disease Control and Prevention, the Department of Defense Health Program, and the Medical and Prosthetics Research Program of the Department of Veterans Affairs. H.R. 5455, the Accelerating Biomedical Research Act, would exempt National Institutes of Health funding. And H.R. 2400 and S. 1249, the American Innovation Act, would exempt research funding at the National Science Foundation, the Department of Energy’s Office of Science, the Department of Defense Science and Technology Programs, the National Institute of Standards and Technology, and the National Aeronautics and Space Administration.

In each of these cases, the clear intention of the legislation is to provide for increased spending in such areas. But if CBO were to follow its precedent for the Harbor Maintenance Trust Fund, it would score them all as having zero impact on outlays or the deficit.

Conclusion

After running into a scoring hurdle to their efforts to boost spending through the Harbor Maintenance Trust Fund, the sponsors of this legislation drafted a new bill to better game the system. CBO’s score gave them the result they hoped for: a zero score despite the bill facilitating billions in new spending. Unless Congress and the CBO work to fix this problem, it could lead to the creation of new and even bigger loopholes to hide the deficit impact of its fiscal policy decisions.