How Can You Make NIL Taxes Simpler?

Name, Image, and Likeness (NIL) compensation, particularly as it pertains to college athletes, is a classic example of a field that is evolving so quickly that policymakers are struggling to keep up. Most legislative proposals to this point have focused exclusively on either the competitive impact of NIL at the federal level or niche tax exemptions at the state level.

Left behind in these conversations is the tax treatment of NIL and the confusion it brings. Not only is it unclear even to seasoned tax experts how to source and even classify different types of NIL income in each state, but the people we are asking to figure it out are often 18-year-olds filing their taxes for the first time.

NTUF recently released a report that gets into the weeds on all the (often costly) hassles that college athletes face on the tax front. The takeaways for policy folks?

- NIL is not exclusive to college athletes. Drafting laws that treat college athlete NIL differently from professional athletes, social media influencers, and other celebrities who profit from their recognizable public image will only muddy the waters further.

- Athletes need clear and consistent guidance on how to classify their income.

- Is NIL income self-employment income, royalties, or even wages? Generally, NIL income will be treated as self-employment income when it requires active services in return (appearing in an advertisement) and as royalties when it is earned passively (profiting off of depictions in a video game), but this can vary by state. Some athletes even earn pass-through income if they decide to set up LLCs. NIL income is usually not wage income now, but some will push for it to be categorized as such.

- What if their NIL contract requires them to perform different types of activities in return for one lump-sum payment? In cases like this, athletes (or their tax advisor) have to use their discretion and pray that tax authorities agree.

- Athletes need clear and consistent guidance on how to source their income.

- If an athlete’s sponsorship deal requires them to perform services in multiple states, how is the income allocated and taxed? This depends on the state and the type of compensation. Usually, self-employment income is split evenly among the states where an athlete had to perform services under their contract. This can change if the compensation for each service is defined under the contract. Additionally, the athlete’s state of residence can try to take a slice as well, and many college athletes retain residence in the state they grew up in, not where they go to school. Royalties are usually sourced to the state of residence, which makes classifying compensation even more important. States that deviate in small ways from these general rules can cause no end of confusion.

- Athletes need protection from shortsighted extensions of “jock taxes” to NIL. States may be tempted to try to take “jock tax” laws that impose income tax obligations on professional athletes who play games there, and extend them to college athletes. Not only would this require states to change existing statutes (jock taxes apply to the wages of professional athletes, and college athletes neither earn wages nor are they professionals), it would result in very little revenue for states.

- States should not create special income tax exclusions for college athletes. Not only does this privilege a certain class of NIL over others, it takes resources away from broader income tax reductions. If a state is struggling to recruit athletes because of its income tax burden, just imagine how its other businesses are faring.

There’s a lot more information on the complexity athletes are facing and how lawmakers can help by reducing it in the full report, but expect this issue to continue to fester in the meantime.

NIL, Data Centers, and OBBBA (Oh My!)

Our experts presented before state legislators who sit on tax committees on three entirely non-controversial topics: data centers, the impact of the One Big Beautiful Bill Act (OBBBA) on state budgets, and the influx of money into college sports.

Check out our resources on NIL, data centers, and OBBBA conformity at NTUF’s website. Our experts are happy to testify or present on all of these issues and more.

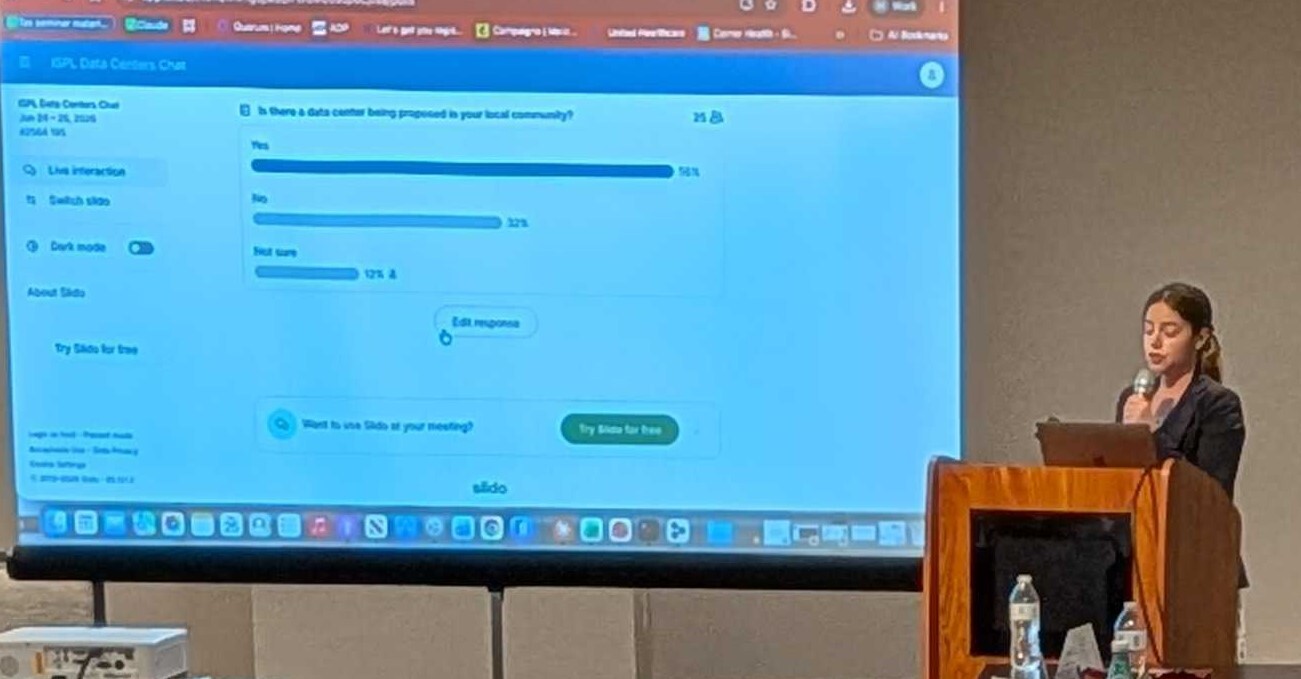

NTUF Senior Policy Manager Debbie Jennings presenting on data centers.

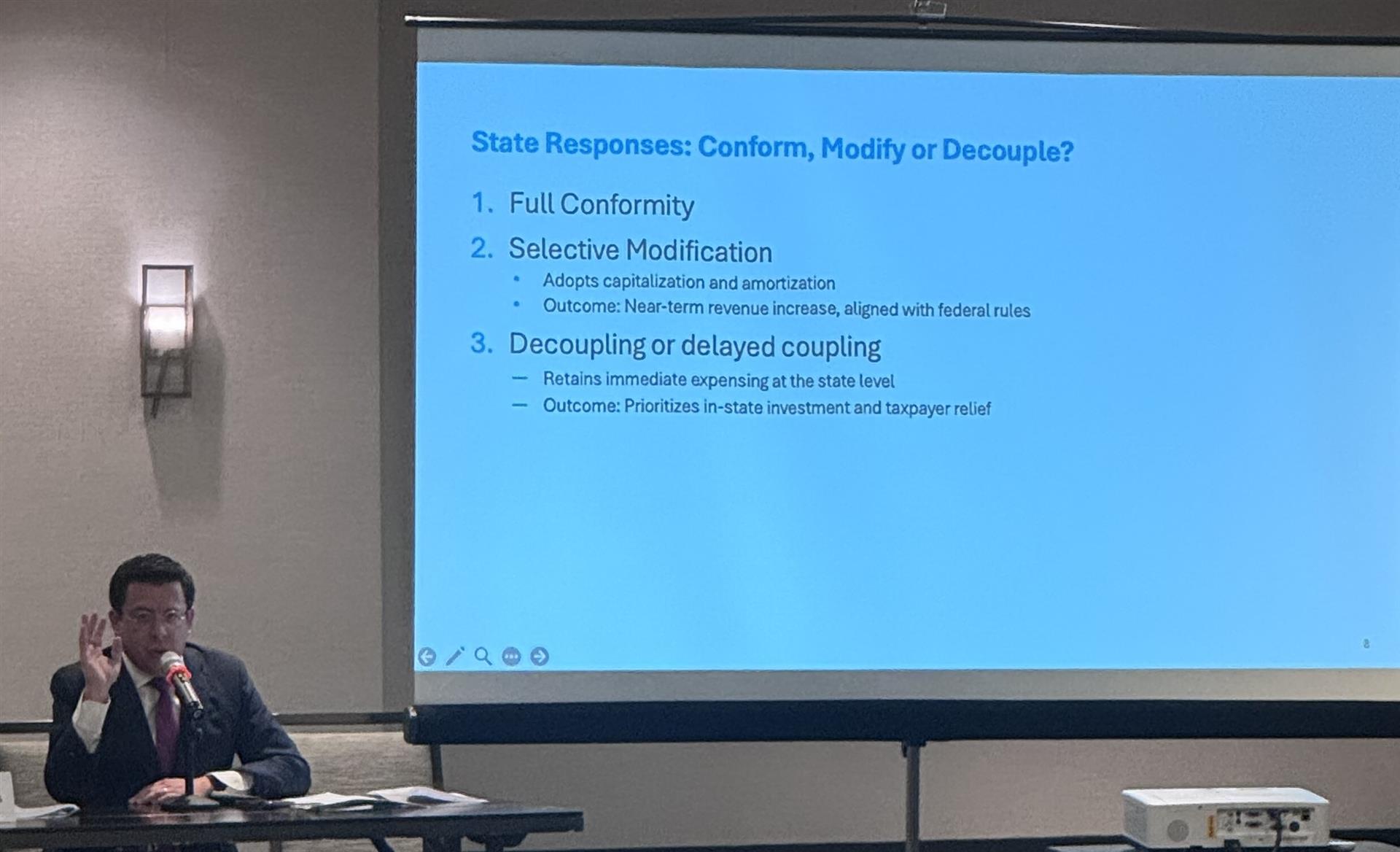

NTUF Executive Vice President Joe Bishop-Henchman presenting on OBBBA conformity.

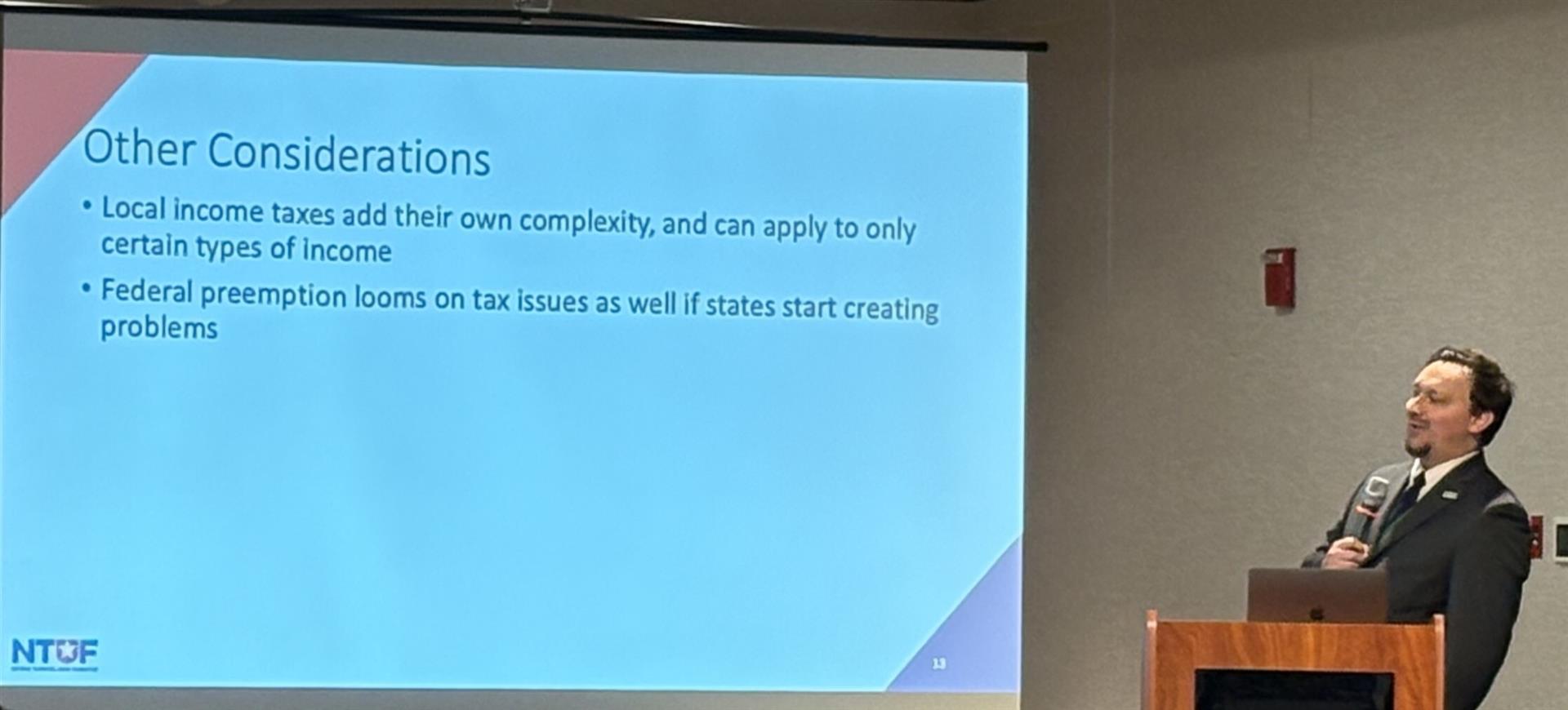

NTUF Director of State Policy Andrew Wilford presenting on NIL taxation.