Ever since 2021, college sports have undergone an expensive makeover. Where once college athletes were strictly forbidden to accept compensation in any form, now the money that has always flowed around college sports is making its way to the players as well. In that brief span, Name, Image, and Likeness (NIL) has come to mean far more than just the sponsorship deals it once referred to. Regardless of one’s opinion of whether or not this is a good thing for college sports, it’s certainly a good thing for college athletes’ bank accounts.

But with great money comes great tax obligations—and, consequently, great tax complications.

NIL income will encumber young men and women with tax compliance obligations that far exceed the general population, even if most college athletes make little more than spending money from sponsorship deals.

Congress has recently shown interest in addressing the patchwork of state laws governing whether, how, and when athletes can earn NIL income. Yet, while conversations about the NIL income itself suck up all the oxygen in the room, taxation of NIL income remains confusing and likely to lead to young adults accidentally incurring tax debts and penalties. To resolve this problem, colleges should prioritize helping their young athletes figure out their tax obligations, and policymakers at all levels of government should work to make the tax rules simpler and more intuitive.

States should resist the urge to try to assess jock tax obligations on visiting athletes, and should seek to harmonize their tax treatment of different types of NIL income with other states. On the other hand, they should avoid handing out special tax breaks for NIL income that are not available to other taxpayers in a misguided attempt to boost recruitment for local sports teams.

Federal policymakers, meanwhile, should not forget about tax issues if they choose to wade into college sports. A federal standard that appropriately categorizes NIL income would be far easier and more straightforward than attempting to harmonize dozens’ of states income tax codes on NIL, and would prevent individual states from creating disproportionate compliance burdens.

Background: The Road to NIL and Current State of Play

Up until 2021, the National Collegiate Athletic Association (NCAA) enforced strict rules that emphasized the unique status of college athletes as “student-athletes” who participated in sporting events as amateurs. Practically, this meant that college athletes could only be compensated for their participation in NCAA sporting events in ways that related directly to their education and athletic competition.

For decades, this included scholarships, room and board expenses, textbooks, and access to special team training and medical resources. Over time, additional forms of allowed compensation were added, such as a “Cost of Attendance” stipend and other emergency funds that could allow teams to provide financial assistance in cases of family or personal emergencies. None of these forms of compensation approached what the highest-profile college athletes could earn if they were allowed access to endorsement deals, however.

These restrictions began to receive more scrutiny and attracted litigation under the Sherman Antitrust Act until, in 2019, California passed the Fair Pay to Play Act (FPPA). The FPPA prohibited universities in California from restricting a college athlete’s ability to enter into NIL deals or contracting with agents.

In the wake of the FPPA, 34 other states passed similar bills—while some others passed and then later repealed NIL-enabling rules out of concern that their state’s law would be more restrictive than updated NCAA regulations. Concurrently, in the 2021 case NCAA v. Alston, the Supreme Court unanimously upheld a lower court case ruling that any caps on education-related benefits to college athletes were illegal under the Sherman Antitrust Act.

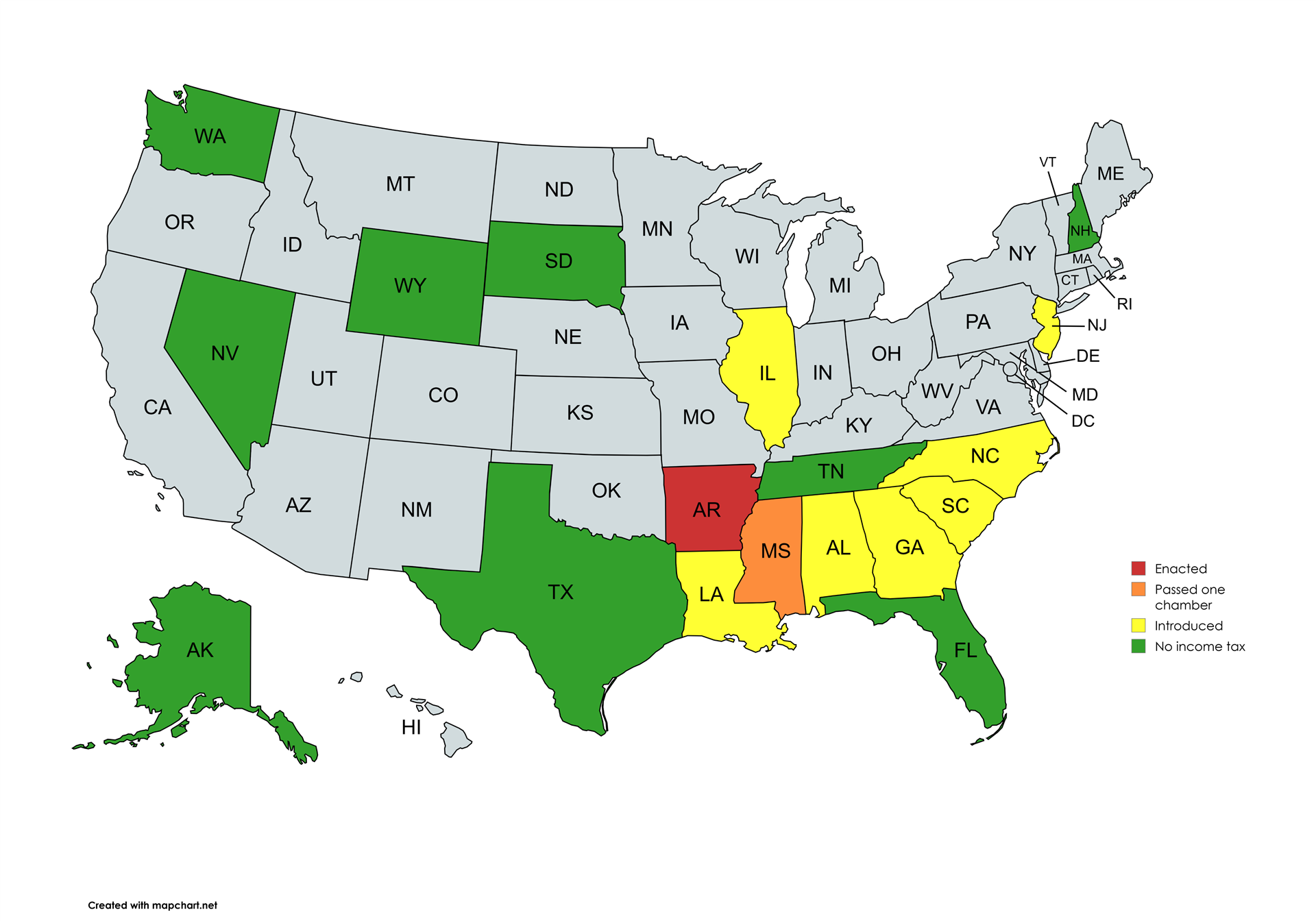

Most SEC States Have Considered NIL Income Tax Exemptions

States that have introduced or passed an NIL tax exemption bill

![]()

In the face of this ongoing legislative and legal assault, the NCAA began to consider an about-face on NIL. In June of 2021, this change in position was formalized via an interim guidance that allowed athletes to profit off of NIL without violating NCAA rules.

Formally, the NCAA continued to enforce rules against “pay-for-play,” or NIL deals that were contingent upon committing to or playing for a certain school. These rules have proven extremely difficult to enforce; while promising a potential recruit a certain NIL contract should they commit to a school may be forbidden, boosters can ensure that players at their school are known to receive larger NIL contracts than competitors.

In 2025, a settlement deal in House v. NCAA further undermined these paper-thin restrictions. Under this agreement, NCAA athletes who participated in college sports between 2016 and 2024 were able to submit claims from a $2.85 billion compensation fund. An estimated 75% will go towards football players and 15% to men’s basketball players, leaving the remaining 10% to be split between women’s basketball and other sports.

But, even more importantly for the future, the House settlement allowed schools to share a percentage of revenue from athletic programs, up to a $20.5 million cap that will increase annually. Scholarships will not count toward this cap. This form of compensation, known as direct pay, is still based ostensibly on licensing compensation, but comes directly from the school as opposed to a separate business or organization.

Direct pay is only available to D1 schools that opt in to the House settlement and agree to contribute toward the compensation fund. However, the vast majority of D1 schools have opted in to the House settlement already. Of the 18% or so of D1 schools that opted out, most are tiny or academically-focused schools in the Ivy, Patriot, or Northeast conferences, the majority of whom never appear on ESPN except as an occasional 16-seed getting walloped by Duke in the first round of March Madness.

Current Forms of College Athlete Compensation

As things stand, three primary forms of compensation are available to college athletes. First is traditional NIL—college athletes receiving brand sponsorships, endorsement deals, and merchandising income that comes about naturally. In this scenario, brands organically reach out to athletes and offer to pay an athlete to appear in advertisements, post about the brand on their social media account, or perform similar activities. This can also take the form of an athlete profiting off of their own NIL by selling their own trademarked merchandise, or the passive use of an athlete’s NIL in video games.

The uniting factor behind the traditional NIL category is that the athlete is profiting from the natural market value of their NIL. The team or school the athlete plays for is relevant only to the extent that it enhances their marketability, and the compensation the athlete receives comes from the market. Depending on whether the compensation requires the athlete to actively perform services (such as appearances in advertisements/at events) or passively allow the use of their NIL (such as through video games), this compensation can be classified as business/self-employment income or royalties, respectively.

The next way that college athletes earn income is via NIL collectives—groups of school boosters who pool resources. These NIL collectives will then compensate their school’s athletes either directly or indirectly, providing the funding for NIL deals that may involve activities such as appearing in local businesses’ advertisements. For higher-profile athletes, these collectives can help connect athletes to larger brand sponsorships.

In contrast to traditional NIL, the motivation behind NIL collectives is to reward their school’s players and, indirectly, recruit future players by ensuring that their school’s players are known to be well-compensated. Income that can be traced back to an NIL collective usually requires some activity by the athlete, making it business/self-employment income.

The last form that college athlete compensation takes is direct pay. This is a new development, arising from the aforementioned House settlement. In this scenario, an athlete is paid directly by the school, out of the school’s budget. Direct pay income classification depends on how the school structures it—normally, athletes will be paid as independent contractors, but schools could choose to treat athletes as salaried employees and withhold income taxes on their behalf.

What Tax Considerations Do Athletes, Schools, and Policymakers Need to Be Aware Of?

Concerns for Athletes

For many student-athletes, NIL will represent their first experience earning taxable income. Unfortunately, NIL income often entails many more tax complications than the average 18-year-old’s summer gig.

Federal Income Tax

Most straightforward is the federal tax. College athletes earning NIL will usually need to report their NIL income as self-employment income. Not only does this type of NIL income require athletes to pay the 15.3% self-employment tax in addition to normal federal income tax liability, athletes must also make quarterly estimated tax payments. Failure to do so can incur penalties and interest that, while not exorbitant, are still best avoided.

Athletes earning significant NIL income also need to be aware of the federal Net Investment Income Tax. This applies to single taxpayers earning over $200,000, and is assessed at 3.8% of the lesser of net investment income or income over the $200,000 threshold. This is particularly relevant for athletes who receive large amounts of NIL income that is classed as royalties, as royalties fall under “net investment income.” Additionally, athletes who choose to be compensated in cryptocurrency instead of cash can end up with a substantial NIIT bill.

State Income Tax

At the state level, things become far more complicated. Normal state-level income taxes apply, as does the requirement to submit quarterly estimated tax payments. The complexity lies in sourcing different forms of income.

Beginning with self-employment income from traditional NIL or NIL collectives, athletes need to track where they perform services related to their NIL contracts. Even a single day spent filming a sponsored advertisement in another state can trigger tax liability there. How exactly this income is apportioned between multiple states is dependent on the language in the NIL contract. If the contract explicitly states what an athlete will earn for each appearance, then the income will be sourced based on the contract. If the compensation for each appearance is not explicitly stated, it would likely be divided up based on the percentage of appearances in each state.

For instance, imagine an athlete at the University of Louisville in Kentucky earns $50,000 in NIL income for five public appearances, four of which are in Kentucky, and one across the border in Indiana. If the compensation for each appearance is not spelled out, the athlete would source $10,000 of NIL income to Indiana and $40,000 to Kentucky. Each state will require its own tax return and likely its own quarterly estimated payments.

Adding yet another layer of complexity is residency. An athlete’s state of residence will tax the entirety of an athlete’s NIL income, even if it is earned out-of-state. It should provide credits for taxes paid to other states. This means that athletes leaving high-tax states like California or New York to go to college in low-tax states should be careful to quickly change their residency status upon heading off to college.

Returning to the example of the Louisville athlete, imagine now that the athlete grew up in California and remains a California resident. Below is a simplified (without deductions or marginal tax brackets) example of how this individual would be taxed.

State | Taxable NIL Income | Rate | Tax Owed |

Indiana | $10,000 out of $50,000 | 2.95% | $295 |

Kentucky | $40,000 out of $50,000 | 3.5% | $1,400 |

California | $50,000 out of $50,000 | 13.3% | $6,650 - $1,695 (taxes paid to IN & KY) = $4,955 |

Total State Tax Paid |

|

| $6,650 |

While residency can raise an athlete’s tax bill, it can also lower it in some circumstances. Royalties are generally sourced to an athlete’s state of residence, so if the above athlete resided in Tennessee, they may be able to avoid state-level tax on their royalty income. States losing out on tax revenue in this manner are likely to closely scrutinize the designation of NIL income.

The last form of college athlete compensation, direct pay, adds what is arguably the most complexity of all. States enforce what are known as “jock taxes” (in truth, just an aggressive application of the income tax) on professional athletes who play games in their states, even if they are only there for a day or two.

More aggressive states may attempt to impose these same obligations on college athletes earning direct pay income. Like traditional NIL income, which is paid based on an athlete’s appearances at events or filming advertisements, direct pay is officially structured as compensation from the school for the use of the athlete’s NIL. Yet some states may argue that since an athlete would not receive this income if they transferred to another school, it is more akin to employment income. This reasoning would allow these states to impose jock tax obligations on the direct compensation the athlete receives.

Jock tax liability is based on the percentage of “duty days,” which comprise not only game days but also days spent training, practicing, in team meetings, and so on. They also include weekends, holidays, and rest days, since the player is required to be available to the team, even if not actively engaged in team activities. Consequently, the percentage of a visiting athlete’s direct pay compensation that is actually taxable by a hosting state is usually in the low single digits.

Nevertheless, athletes need to be careful to comply with these obligations, even if the actual tax payments are small. While similar obligations for regular work travelers often go unenforced, college athletes’ time spent in other states is broadcast on national television. States can easily find out which visiting athletes are not filing tax returns and come after them.

While traditional NIL income is generally not subject to jock taxes, this depends on what the contract requires. An athlete whose endorsement contract with Nike contains any performance-based stipulations, no matter how roundabout, may find that they have inadvertently opened themselves up to demands for tax payments from other states.

Local Income Taxes

The final layer of tax for college athletes to concern themselves with is localities. Just as with state taxes, players who perform contractually obligated activities in cities or localities can be subject to all relevant local income taxes.

In most cases, localities’ rules about nonresident taxation will closely mirror those at the state level. However, the rules can vary based on the classification of income. For example, Kansas City, Missouri, taxes only wage income at a 1% rate, not self-employment income, while Missouri taxes both wage and self-employment income at the state level.

All in all, filing a tax return with NIL income is a complicated task for a seasoned CPA, let alone a college kid whose favorite subject in high school was gym class. Which leads us to . . .

Concerns for Colleges

Colleges need to be intentional about how they choose to classify their athletes. The only reason why jock taxes in professional sports leagues have not led to thousands of exasperated athletes burning the midnight oil to file their tax returns is that most professional sports teams handle tax compliance for their players. Colleges need to start thinking of their athletes the same way.

For purposes of direct pay, colleges that classify their athletes as employees must offer the benefit of tax withholding, at least on that portion of their athletes’ income. This will be the portion of an athlete’s NIL income that is most likely to face jock taxes in many different states, so leaving the complexity to dedicated college accountants would take much of this burden from athletes.

But whether colleges prefer to designate athletes as W-2 employees or independent contractors, they should be scrambling to develop tax support for athletes. Most athletes are not earning millions of dollars on NIL—according to brand advisor and agent Bill Carter, the median NIL deal is worth about $60 (with the median athlete’s total earnings worth just over $1,000).

Athletes earning NIL income in the low five figures, particularly combined with taxable room and board income, are making enough money to have tax compliance obligations. However, they are not making nearly enough money to hire someone else to handle those obligations for them. Tax advisors for athletes need to become as standard as academic advisors for colleges running a sports program.

The last thing for colleges to consider is less directly tax-related, but important nonetheless. Colleges across the country are raising their athletic fees for regular students to raise more revenue to fund direct pay deals. Sharing existing revenue from sports programs with athletes is one thing, but colleges should resist the urge to pass these costs on to other students. It’s a deeply unfair way to attract top recruits.

Concerns for Policymakers

State Policymakers

Lawmakers in any of the 15 states that have not done so should consider implementing clear and straightforward rules about how athletes can earn NIL income in their states, whether colleges can assist athletes in finding NIL deals, disclosure requirements, and what industries can offer NIL deals.

States also need to be clear about how they plan to treat NIL income for tax purposes. Most states already have rules on the books about how they intend to tax endorsement income, professional athlete contracts, and licenses to use a player’s likeness for video games. Yet all of these rules were designed with professionals in mind, where the line between team salary and sponsorship income was much clearer. Lawmakers should not leave it up to state revenue officials to interpret existing statutes in the NIL era, lest they end up not liking the rules that the state revenue officials come up with.

To the greatest extent possible, states should be seeking to harmonize these rules across state lines. The greatest complexity for athletes will come from navigating the patchwork of separate state laws. To the extent that states can form interstate compacts or rely on existing ones to simplify the tax filing process, they should do so.

The same thing is true for jock taxes. As noted above, while advertising and brand deals are clearly licensing deals, some states may be tempted to assess jock tax obligations on direct pay. Not only is this an inappropriate treatment of NIL, it would cause massive compliance burdens for college athletes, most of whom are not earning large sums of money.

States concerned that not taxing visiting athletes will mean missing out on a pile of tax dollars should recognize just how little jock taxes on NIL would raise. For the sake of an example, imagine a hypothetical college that pays out three-quarters of its $20.5 million direct pay budget to its football team. Then, let us assume that the team spends 3 out of 180 duty days practicing for and then playing a game against Rutgers in high-tax New Jersey.

Once again, we will use a simplified calculation that ignores deductions and tax brackets and just assume that the entire $15.38 million is taxable at New Jersey’s top rate. New Jersey would then tax 1.67% (or 3/180ths) of the $15.38 million total salary base at its 10.75% rate.

All told, jock taxes on all this income would gain New Jersey just $27,547 more in tax revenue. If six top-tier teams, with maxed-out direct pay budgets, visited Rutgers over the course of the year, New Jersey would bring in only an extra $165,281. After accounting for deductions and marginal brackets, the real number would be even lower.

And, when all is said and done, New Jersey would only net a fraction of even that amount. Because other states will do the exact same thing back to Rutgers’ players when they travel, New Jersey will need to credit their Rutgers athletes for taxes paid to other states and reduce their New Jersey tax liability. In the end, it will work out to be something of a wash at the level of state budgets, leaving the players with the burden of tax compliance.

Therefore, states should consider entering into a jock tax truce on NIL. Paltry jock tax revenues do not justify the compliance costs they create at the professional level, where individual athletes can make tens of millions of dollars in a single year. For NIL, where most athletes’ income will be measured in thousands instead of millions, the cost/benefit ratio will be even more skewed.

What states should not do is create special tax exemptions for NIL to try to lure athletes to their schools. Arkansas has already passed one such tax break, while many other southern football states have seen bills introduced that would do the same. This would not solve the complexity issues, as the biggest source of those will be multistate taxation. Neither would it meaningfully contribute to recruiting efforts. States that want their taxes to be more competitive for 5-star quarterbacks should make zero income tax the goal across the board, not just for a tiny subset of the population.

Federal Policymakers

Federal policymakers have been watching the development of state NIL rules and may soon jump in with a bill at the congressional level. Most recently, the bipartisan Protect College Sports Act passed the Senate Commerce Committee.

The Protect College Sports Act would enshrine the right of college athletes to earn NIL nationwide, regulate athletes’ agents, and restrict transfers, college eligibility, and conference consolidation, among other things. NTU’s Brandon Arnold has written critically about some of the potential negative impacts on college competition, but the problem on the tax front is that it addresses none of the issues raised above.

Perhaps the best thing that federal policymakers could do for college sports is establish uniform rules about how NIL income is taxed and where, particularly by cutting down on the number of states that could claim a slice of each athlete’s tax pie. Individual states may be hesitant to unilaterally disarm on jock taxes, but Congress could help by making all of them do it at the same time.

Congress should consider weighing in on all these issues. This would mean not just addressing the patchwork of non-tax rules that athletes earning NIL currently are confronted with, but also defining different forms of NIL income, clarifying where and how to source NIL income, and preventing states from taxing college athletes for playing games in their state.

Conclusion

Even after half a decade in existence, NIL income for college athletes remains a new and evolving concept. Unfortunately, new and evolving concepts are exactly the types of things to which tax rules struggle to adapt.

College athletes need to be aware that their new income streams will come with significant tax complexity. Schools and policymakers at all levels of government should also recognize this and take action to protect young athletes from getting buried under a mountain of paperwork. A few simple and straightforward clarifications and fixes can help bring it back down to more entomologically normal dimensions.