(pdf)

Introduction

Before the Supreme Court case South Dakota v. Wayfair was even a glimmer in a tax collector’s eye, states and a diverse array of special interests spent decades agitating for greater cross-border tax authority. In the process, there were grandiose claims that tens of billions of dollars in taxes were going uncollected. Thus, allowing states to collect tax on remote sales made by businesses with no physical presence in their borders was supposed to allow them to generate huge new streams of revenue to patch state budgets. Reality hasn’t come close to matching this revenue dream.

In fact, the revenue that states are now expecting from their post-Wayfair tax laws is barely more than one-quarter as much as exuberant advocates claimed they could expect prior to the case. In state after state, when budget analysts were required to assess remote sales tax collection laws — and be held accountable for them — revenue estimates came in at just a fraction of earlier claims. What was billed as a revenue tsunami has been little more than a ripple.

How We Got Here

The Supreme Court’s decision in Wayfair had far-reaching consequences. Before the Wayfair ruling in June 2018, states had to respect the precedent established in the 1992 case of Quill Corp. v. North Dakota, which said that a state could not force a business to collect its sales tax unless that business had a physical presence, or “nexus,” in their state—such as a storefront, warehouse, or full-time employees. But in Wayfair, the court threw out this precedent, opening the door for states to impose “economic nexus” taxes on any business that sells into the state, regardless of their location.

That’s had a significant effect on small businesses. Remote retailers that previously remitted sales taxes to a single jurisdiction (or none at all, if located in states without a general sales tax) were suddenly faced with the prospect of having to collect for hundreds or even thousands of the estimated 12,000 jurisdictions nationwide. The added burden of implementing extensive compliance infrastructure throughout one’s small business has left many business owners in a tough position.

Unsurprisingly, the expectation that small businesses stay up to date on the flurry of laws and regulatory pronouncements coming out following the Wayfair decision has left many business owners feeling left behind. A recent study by Intuit Quickbooks found that 52.8 percent of small business owners thought that managing sales tax for their business is either not at all clear or only somewhat clear. As many as one-fifth of small business owners reported feeling “very concerned” about the Wayfair decision, while nearly 30 percent should be concerned by don’t know it — they hadn’t even heard about it!

This is the climate that states have foisted upon small businesses around the country in a frantic grab at a perceived revenue gold mine. The only problem — that “gold mine” is not panning out as promised.

In Pursuit of An End to Quill

For years after the Supreme Court ruled in Quill Corp. v. North Dakota that businesses must have physical presence within a state to be liable for collecting and remitting sales taxes on purchases within the state, the so-called “Kill Quill” movement aimed to overturn this impediment to greater taxing powers. What started with efforts to pass a federal law blessing cross-border taxation tied to simplification efforts quickly morphed into “frontal assaults” on the precedent by states. To do so, they passed laws they knew to be unconstitutional under Quill with the express intent of taking litigation all the way to the Supreme Court.

South Dakota was far from the only state that drafted and passed an economic nexus law before the Wayfair decision affirmed the constitutionality of such laws — Indiana and North Dakota also did the same in 2017 alone. Other states came up with more creative workarounds to avoid the Quill precedent. Massachusetts and Ohio each imposed “cookie nexus” rules in the buildup to Wayfair, alleging that “cookies,” or information that websites store on devices to streamline the browsing experience, constituted “physical presence.” Though this argument was legally hollow and unlikely to pass constitutional muster, it illustrated the desperation that states felt to end Quill.

Why were states willing to peddle such frivolous legal arguments? The short answer is that they believed a jackpot of revenue was waiting on the other end of the tunnel if they could only find a way to force their way through. The National Conference of State Legislatures (NCSL) insisted that states were missing out on $25.9 billion in revenue in 2015 from sales where tax was not collected by the out-of-state business. The more cautious federal Government Accountability Office (GAO) suggested in late 2017 that states were missing out on anywhere between $8.5-13.4 billion in 2017 revenue.

While these numbers may sound significant, they represent only a small fraction of state budgets. The GAO’s figures would represent between 0.44 percent and 0.69 percent of total FY 2017 state expenditures. The NCSL’s estimates are slightly more generous, yet still pale in comparison to state budgets as a whole, adding up to just 1.33 percent of state spending. In other words, the revenues that states stood to gain were minimal, even granting the wild claims of enormous amounts of untapped potential.

States nevertheless used these theoretical revenue loss estimates to claim that the increase in internet sales was contributing to erosion of the sales tax base, forcing upward pressure on rates. But there is a significantly greater culprit than online retail when it comes to state sales tax base erosion: exemption of services from the tax base. Today, the typical sales tax base is roughly 20 percent smaller than it was in 1970 — however, were services to be included as taxable, the sales tax base would actually be 11 percent larger.

That’s not to say that the solution to states’ revenue woes is to rush headlong to tax services instead. Instead, it shows that the growth of online retail, while real and significant, is by no means the dominant factor in states’ challenges with their sales tax.

Nonetheless, many rushed to enforce new remote sales tax laws as soon as the Court made public its decision in the Wayfair case, with some holding special sessions to make economic nexus legislation enforceable in time for the holiday season. States such as Michigan and Wisconsin could not even wait for their legislatures to draft legislation enacting economic nexus laws, instead relying on administrative issuances to make these new tax rules a reality.

Did this haste deliver the returns that were promised? The short answer: no.

The Wayfair Windfall Falls Short

Two major organizations produced state-by-state estimates that became some of the most commonly-cited “lost revenue” estimates that advocates of overturning the Quill standard pointed to: the National Conference of State Legislatures (NCSL), and the federal Government Accountability Office (GAO). NCSL’s claims were based on the work of University of Tennessee professors William Fox, Donald Bruce, and LeAnn Luna from 2009, while the GAO released state-by-state data in November of 2017.1

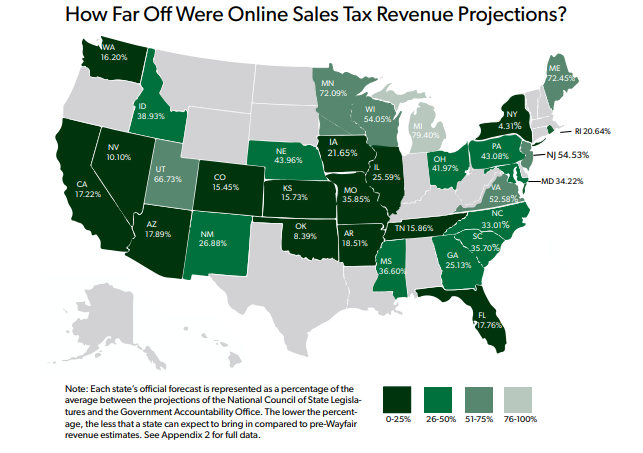

By comparing authoritative estimates of revenue associated with new remote sales tax legislation to previous estimates of revenue available from NCSL and GAO, we can assess the initial accuracy of the pre-Wayfair projections upon which many states pinned their hopes.

NTUF was able to collect official revenue estimates from 32 different states that have come out after the Wayfair decision. These are estimates prepared by fiscal agencies, revenue commissioners, and other official sources that face some sort of public accountability for the accuracy of their numbers.

Not a single state met or exceeded NCSL’s revenue estimate. Only two of the 32 states met or exceeded the midline of the GAO’s range of estimates. On average, official estimates were about one quarter the amount that NCSL estimated (25.96 percent) and about half the amount that GAO estimated (49.85 percent). The median official estimate was just 21.81 percent of NCSL’s projections and 46.75 percent of GAO’s.

In these 32 states, NCSL projected a total of $19 billion in “missing revenue,” while the midline of GAO’s range of estimates predicted nearly $8.6 billion. In reality, official estimates have turned up just $3.627 billion. While $3.627 billion sounds like a lot of money in a vacuum, it is in fact a vanishingly small percentage of state revenues. It represents an average of just 0.7 percent of general fund revenue, which amounts to little more than noise in the data in most states.

Though this paints a stark picture of spectacularly inaccurate revenue projections used to help justify seizing greater tax power, the reality is likely worse than the data in this paper shows. NCSL’s estimate was for 2015 revenue, while GAO’s was for 2017. Meanwhile, in order to be as conservative as possible, our research generally utilizes later-year data, which on average will show higher revenue due to economic growth and inflation. In fact, in the majority of states in our study, we utilize revenue estimates from 2020 or later. This will have the effect of significantly understating the true scale of NCSL’s and GAO’s inaccuracy.

Why Pre-Wayfair Estimates Were So Wrong

Naturally there is imprecision in any prediction for future revenue, but the numbers reported by NCSL and GAO were not only wrong, but in most cases not even close to what fiscal analysts have projected now that legislation is actually being implemented. With virtually every pre-Wayfair revenue estimate proving staggeringly inaccurate, the big question is: why?

Without getting into an exhaustive analysis of the methodology of the studies cited here, there are several factors that have contributed broadly to overexuberance on the part of lawmakers and activists about post-Wayfair tax revenue possibilities. The first is overestimating the growth in online retail.

It is true that internet sales have become far more commonplace over the past couple of decades, growing to roughly 10 percent of total retail sales at the end of 2018 compared to closer to 4 percent just ten years before. But to simply extrapolate this trend and assume that substantially all retail will be conducted remotely over the internet in the coming years is a grave misunderstanding. While online business is indeed growing substantially, retail trends are more suggestive of a convergence on a so-called “brick-and-click” model, where the most successful businesses blend physical outlets with robust online sales.

Take Amazon’s acquisition of Whole Foods, its building of book stores, or its experimentation with new technology at its Amazon Go convenience stores. In the world of traditional brick-and-mortar stores, look to Walmart’s 40 percent increase in e-commerce sales last year or its rapidly-expanding Walmart Marketplace, which offers small sellers a platform not unlike those of well-known purveyors of marketplace platforms like Amazon, eBay, or Etsy. Along with the strong performance of the retail sector as a whole in recent years, these anecdotes are an indication that traditional in-store retail is by no means on the road to extinction at the hands of the internet.

An additional factor that has tricked many lawmakers into overestimating the size of a post-Wayfair revenue boost is underestimating the extent to which sales tax was already required to be collected for many online sales even prior to the case being decided.

In June of 2018, the Census Bureau estimated that nearly 89 percent of retail sales still happened in brick-and-mortar stores. By virtue of benefiting from widespread physical presence in states, these stores were already required to collect sales tax. Of the remaining 11 percent of so-called “nonstore” sales, including internet retail and mail order houses, the GAO estimated that 80 percent of tax on such sales was already collectible under pre-Wayfair law.

This stands to reason, because the majority of online sales are conducted by businesses that either had legal obligations or agreements to collect tax for all of their sales even before Wayfair. That’s because the list of top 10 online retailers is dominated by companies like Amazon, Walmart, Apple, The Home Depot, Costco, and Macy’s that already had business models that required them to collect tax for their web sales. These companies alone represent more than 60 percent of e-commerce sales. In other words, the total universe of sales that were non-taxable prior to Wayfair and taxable after it is quite small, representing at most a few percent of retail commerce.

One additional factor, which in context is a reasonable one, is the fact that states pushing post-Wayfair tax rules have generally included a “safe harbor” provision ensuring that smaller businesses that lack a significant economic impact in the state are not required to collect tax. These provisions have the effect of reducing the revenue haul a state can expect since some portion of sales into the state would not have tax collected by the seller. However, it is worth noting that the administrative costs to states (and the compliance costs to small businesses) involved in collecting such revenue would be significant enough that the net result may not yield much additional revenue even if states eliminated a safe harbor.

Conclusion

The urgency that states felt to eliminate Quill, and the reasoning that a bare majority of the Court eventually concurred with in Wayfair, was based upon overblown and inaccurate estimates. The revenues that states based their hopes upon (themselves not all that significant relative to state budgets) have failed to materialize.

It is unfortunate, therefore, that states have been so reckless in their implementation of economic nexus taxes. Despite the apparent harm to small and medium-sized businesses that were unprepared to take on a massive new compliance burden, many states made quick implementation of economic nexus rules a top priority in order to capture as much revenue as possible.

Now that revenue estimates are approaching reality, states with economic nexus laws should consider revisiting their laws to take the concerns of small businesses more seriously. And states considering new economic nexus laws should beware: the promised revenues may not deliver as expected.

1 Fox, Bruce and Luna did update their data in 2012 (estimating even higher amounts of lost revenue), but NCSL continued to use their 2009 estimates; thus, NTUF does as well.

![]() Appendix 1: State Data and Sources

Appendix 1: State Data and Sources

![]() Appendix 2: Official revenue estimate as a percentage of the average of NCSL/GAO projections

Appendix 2: Official revenue estimate as a percentage of the average of NCSL/GAO projections