Our Tax Code, along with its associated regulations and rulings, is virtually incomprehensible and imposes an enormous 6.9 billion hour compliance burden on filers. It is also remarkable how complex the U.S. tax system is when compared to other developed countries.

Every year, the accounting and consulting firm PricewaterhouseCoopers (PwC) publishes a report entitled “Paying Taxes” which compares the tax burdens faced by a hypothetical business in 189 countries of varying sizes, and levels of development. The burden is measured in hours per year spent complying with the country’s tax filing procedures, the number of payments it must make to do so, the total tax rate the business would face, and an overall “ease of payment” ranking that assigns weights to those metrics.

To illustrate how bad complexity is in the United States, NTU Foundation compared these measurements to four other countries in the Organization for Economic Cooperation and Development (OECD).

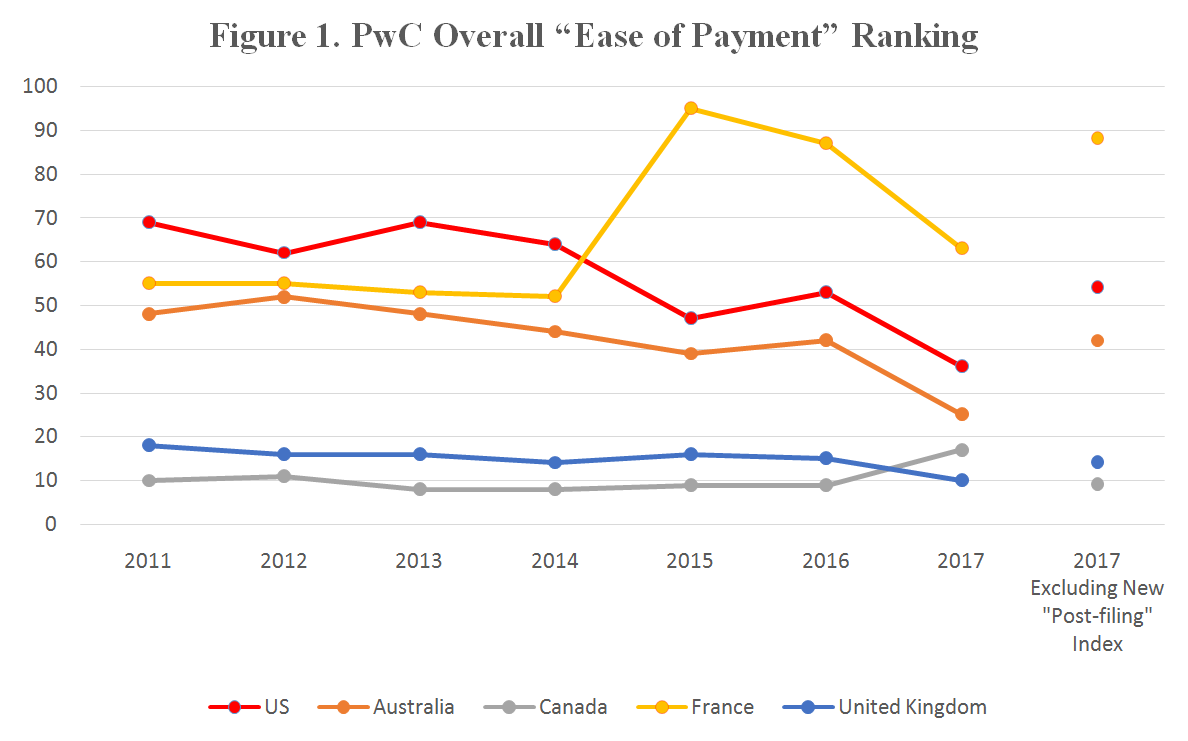

The figure above shows the overall ranking of the five countries over the past seven years. For the past three years, PwC’s studies have shown that only France scored worse than the U.S. on ease of filing. Prior to 2015, France actually scored better than the United States, but apparently the attempts at tax simplification under Socialist President François Hollande has yet to produce the desired net decrease in the chore of business and personal compliance that existed at the beginning of the decade.

While the graph seems to indicate that the U.S. made great strides relative to the other countries in 2017, the improvement has more to do with the addition of a new metric to the report this year. PwC established a new “post-filing” index based on the time to comply with an audit, the time to comply with a value-added tax (VAT), and the time to obtain a VAT refund. A VAT is a consumption based tax placed on a product whenever value is added during production, and at final sale. The VAT, which is not used in the U.S., can generate administrative and compliance burdens. Heaping a VAT on top of our current tax system would present many complexity challenges, as other countries experiences indicate. PwC also tabulated a net ranking of all the countries without this new index. Instead of greatly improving overall from 53 to 36, the U.S. dropped one spot to 54.

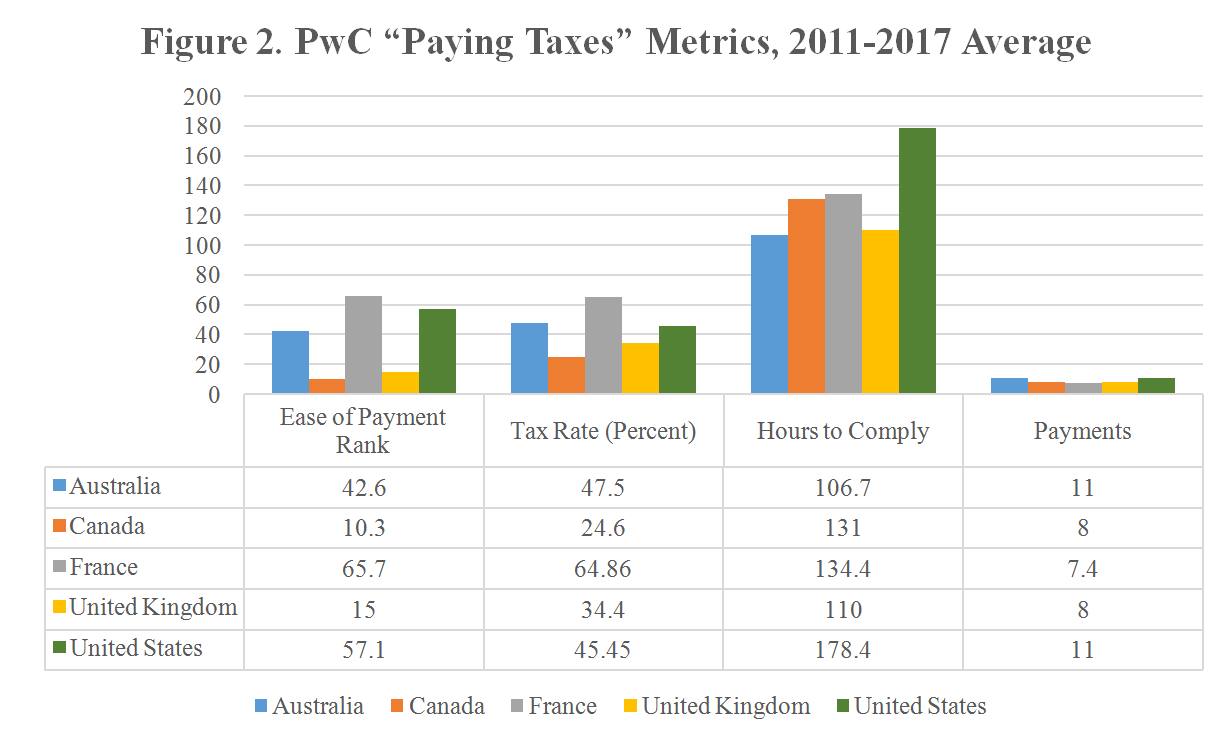

Figure 2, below, compares the metrics of the U.S. with the four OECD countries based on their average value since 2011. The total tax rate is the third highest, with the U.S. and Australia imposing the most payments. By far, the U.S. requires the most time spent complying, 178 hours, compared to France’s 134 hours.

Reforms should be enacted to reduce the overall corporate tax rate, among the highest in the OECD . But policymakers also need to find ways to simplify the compliance burden. This would make the U.S. even more competitive globally, as a destination for businesses … and job creation.