(pdf)

Taxpayers know that failure to pay what they owe in a timely manner means consequences. Interest, penalties, and fees are all things a taxpayer can expect to deal with if they let the April 18 deadline pass by without filing a federal income tax return.[1] And while most states with an individual income tax adhere to this deadline as well, taxpayers may not be aware of one additional punishment that certain states will subject taxpayers to if they fall behind on their taxes: public shaming.

At least 19 states continue to publicly post “shame lists” intended to encourage other taxpayers into pressuring their delinquent counterparts into paying what they owe — or, at least, what revenue officials in that state believe they owe. How exactly this crowdsourced method of tax enforcement is meant to work is left up to the imagination.

These lists air publicly tax disputes that would otherwise be known only to parties that have a real interest in knowing about them, humiliating delinquent taxpayers with little regard for whether their delinquency is purposeful or malicious. What’s more, there is little evidence that they make any significant difference for tax compliance rates. States that continue to publish these shame lists should look at repealing the legislation that requires their publication.

A Practice That is Neither New Nor Showing Any Signs of Abating

Since NTUF’s last analysis of these lists in 2020, very little has changed. Since then, one state has begun publishing lists of tax delinquents: South Dakota, which has no individual income tax and publishes only business tax delinquents. Pennsylvania, the sole state coming off the list from 2020, continues to reference a publicly available list that is updated monthly on its website, but the list is no longer accessible. Illinois does something similar, hosting a web portal for delinquent taxpayers that is not populated with any updated data.

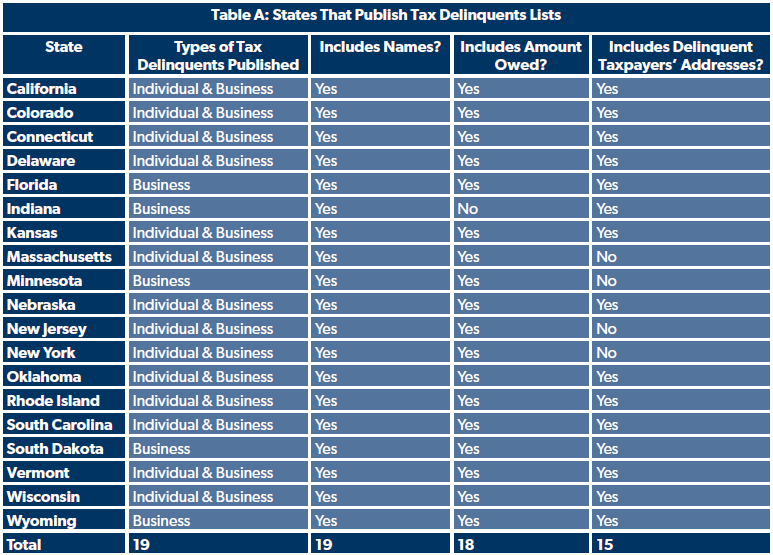

Table A shows the states that continue to publish tax delinquents lists, what types of tax delinquents are published, and what other personal information is disclosed.

States posting lists of delinquent taxpayers online is almost as old as the internet itself. All the way back in 2001, Louisiana debuted its “CyberShame” program, based explicitly on the “premise that publication of a delinquent taxpayer’s name will shame them into paying the taxes they owe.” Louisiana has since stopped publishing this list.

It’s also worth noting that aside from state-level lists, many counties publish lists of delinquent taxpayers — even in states that do not do so.

Not Just “Public Record”

While Louisiana was more overt about its goal of “shaming” delinquent taxpayers into paying what they owe, most states that publish these lists nowadays avoid using the word “shame” in official publications. Nevertheless, it is difficult to conceive of any other reason to divulge not only delinquent taxpayers’ names, but also their addresses and the scale of their delinquency.

After all, while it is true that tax liens are already public information, the publication of a list of delinquent taxpayers is a very different beast. Tax liens are “public” in the sense that they can be accessed by those specifically searching a person’s financial history. The only people or organizations likely to do that are potential creditors seeking to establish that individual’s financial history or trustworthiness — in which case a taxpayer’s unpaid tax debt would be as relevant as unpaid credit card bills.

On the other hand, normal people are not trawling through public databases of tax liens, most of which require paid subscriptions to access, in order to find out which of their neighbors and friends are behind on their taxes. The average person likely would not even know how to go about looking up tax liens against a specific person.

The “public record” argument therefore falls flat. Taxpayers paying their state taxes can easily find lists of taxpayers who are behind on their taxes right on the same website they must go to to file their taxes or seek out tax information — indeed, often on the website’s home page. News organizations will often report on the information on these lists as well, making a visit to a Department of Revenue website unnecessary.

Who Cares About Tax Cheats?

That leaves tax delinquents lists as a significant airing of dirty laundry — blasting out information about a dispute that only really needs to be between state revenue officials, the delinquent taxpayer, and possibly the courts.

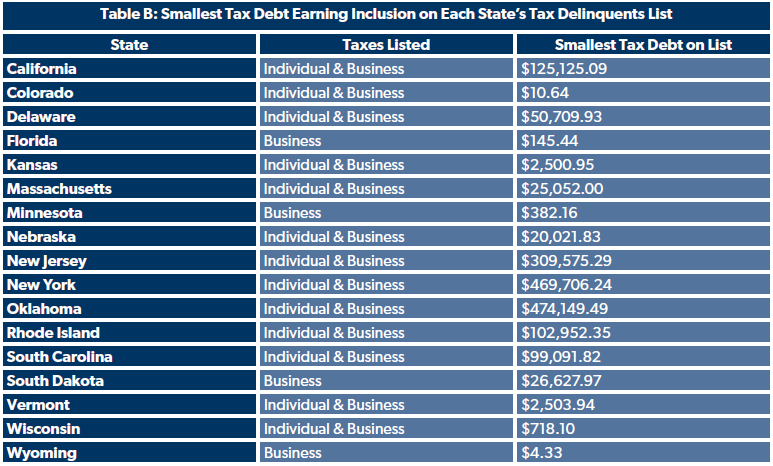

Especially this close to Tax Day, taxpayers may not be inclined to be too concerned about the privacy of tax scofflaws. But it’s important to note that taxpayers with unpaid tax debts are not necessarily wealthy individuals who can’t be bothered to pay their taxes. Table B shows the smallest tax debt earning inclusion on each state’s tax delinquents list.

Table B shows that while some states restrict the names they publish on tax delinquents lists to very high tax debts, states like Colorado and Wyoming publish public information on taxpayers who owe comically small amounts of money. Cases this small are almost certainly taxpayers who are struggling financially or even unaware of their tax debt.

That’s because states have different processes before a taxpayer is included on a list of delinquents. Most states make at least one attempt to notify taxpayers before adding them to their list, but taxpayers who are not regularly checking their mail may be out of luck. States like California and Rhode Island only notify taxpayers 30 days before they are included on a list of delinquent taxpayers, while Connecticut includes any taxpayers who are delinquent for 90 days or more.

In general, there is a clear presumption on the part of states that taxpayers who have not cleared their tax debts are not doing so knowingly. That’s an attitude that has been commonplace among tax enforcement agents at the federal level as well, one that is often harmful for compliance.

The fact is that the tax code, at every level, is often complicated, and human error only compounds the problem. Taxpayers make mistakes, miss letters, and misunderstand their obligations. The presumption that each of these errors is made maliciously creates an unnecessarily antagonistic relationship between taxpayers and tax enforcement agents.

Back in 1991, Ernest Dronenburg, then Vice Chairman of California’s State Board of Equalization, testified before Congress that “a .5% increase in voluntary compliance resulting from taxpayer education” would return more than double the expected revenue increase from doubling audit coverage. While that was three decades ago, it nonetheless illustrates how wrongheaded the recent shift in focus towards punishing taxpayers who make mistakes and away from helping taxpayers avoid them in the first place is.

Publicizing delinquent taxpayers’ addresses and tax debts for all to see is a dubious enough practice if it could be guaranteed that delinquent taxpayers were all simply scofflaws. The fact that this is far from the case only makes them even more questionable as tax enforcement methods.

Do Tax Delinquents Lists Even Work?

The case for tax delinquents lists may be stronger, if still morally dubious, if they were effective. However, there is little evidence to suggest that they are.

One analysis by German researchers at the University of Hohenheim found that tax shaming tactics could generate one-time marginal increases to tax revenue, but that the effect “tapers off quickly.” Another U.S.-based study found that while reminders of unpaid tax debt can increase payment rates among taxpayers with debts below $2,500, shaming tactics are ineffective.

Former National Taxpayer Advocate Nina Olson has warned Congress that not only can tax shaming backfire among taxpayers of a certain worldview, but that it can signal to compliant taxpayers that other taxpayers are not fulfilling their obligations. That can erode taxpayer confidence in the value of the taxes they pay to society, suggesting that their neighbors are coasting on the taxes that the taxpayer is paying. If taxpayers are convinced that tax evasion is widespread, compliant taxpayers will become embittered and may see tax evasion as more of a valid option for themselves.

It’s also worth noting that tax shaming is far from the only enforcement tool that revenue departments have in their arsenal. Others are far more effective and proven, leading to the question of whether taxpayers who are unmoved by threats of wage garnishment, further financial penalties, and potential law enforcement action would be moved by social pressure.

Conclusion

Shame lists of tax delinquents represent a deeply irresponsible publication of information that is not any of the business of the general public. Not only do they subject taxpayers to humiliation based on tax liabilities that they may be unaware of or lack the financial resources to handle, they are not even effective in achieving their stated or implied goals.

The 19 states that continue to publish tax shame lists, and the 21 states that continue to reference these lists on their revenue websites, generally do so on the basis of a legislative mandate. States should consider repealing these laws and sending a clear signal to taxpayers that tax disputes will be handled in-house or in court, not in the public square.

Research assistance provided by National Taxpayers Union Foundation Intern Louise Vieille-Cessay.

[1] Disaster relief means that taxpayers in Alabama, California, Georgia, Mississippi, and New York have a later deadline for federal income taxes returns.