For most people, it isn’t very hard to establish which country to pay tax to. For those whose work routinely calls them to spend long amounts of time abroad, the tax consequences can be nightmarish.

Colombian pop singer Shakira found that out in 2017, when an investigation by the Spanish tax department determined that she should have paid about $30 million in personal income and wealth taxes to Spain in 2011. Penalties and interest doubled that amount to $60 million.

In most countries, a non-resident does not owe tax unless they spend 183 days there in a year — in other words, more than half the year. That seemingly straightforward standard can get a bit fuzzy, however.

In Shakira’s case, Spain could only prove that she spent 163 days in the country. Nevertheless, Spanish authorities alleged that Shakira’s public relationship with Spanish soccer player Gerard Piqué constituted enough of a connection to make up for the remaining 20 days.

This week, Shakira finally won in Spain’s National Court, securing a judgment that Spain had to pay her back the $60 million plus interest.1 While the Spanish government can still appeal to the country’s Supreme Court, the case illustrates the complexity that can beset people who work outside their country of residence.

U.S. Tax Residency

For example, the United States takes that 183-day test and turns it into a high school-level math problem. Nonresident Americans owe U.S. tax in a year if they exceed 183 days working in the U.S. over the previous three-year period, calculated as follows (please take out your TI-84s):

- Each day of that year, plus

- Each day of the year prior, multiplied by ⅓, plus

- Each day of the year before that, multiplied by ⅙.

Additionally, the nonresident must have spent at least 31 days working in the U.S.

American citizens living abroad are also required to file a U.S. tax return every year. They can be eligible to deduct up to $132,900 in income earned outside the U.S. for tax year 2026 (adjusted for inflation annually), as well as a conditional deduction or exclusion for housing costs. This is provided that they either meet the bona fide residence test (a test that is so obscure that the IRS cannot determine whether a taxpayer qualifies until they file their income tax return), or are physically present in a foreign country for more than 330 days.

Americans abroad are also required to report income under the Foreign Account Tax Compliance Act (FATCA), as well as a Report of Foreign Bank and Financial Accounts (somewhat bizarrely abbreviated as FBAR).

FATCA requires American citizens to file reports on financial accounts held in foreign countries. Americans living in the United States need to report foreign financial assets if they exceed $50,000 at the end of the year or $75,000 at any time during the year. Both these thresholds are doubled for married filing jointly taxpayers.

Americans living abroad face the same requirements, but only if foreign financial assets exceed $200,000 at the end of the year or $300,000 at any time during the year. Once again, these thresholds are doubled for married filing jointly filers.

FBAR, on the other hand, does not get sent to the IRS, but the Financial Crimes and Enforcement Network of the U.S. Treasury Department. FBARs must be filed by U.S. citizens on foreign bank accounts exceeding $10,000.

FATCA and FBAR have proven far more of a headache than a financial boon to the United States government. At the time it was passed into law, it was estimated that FATCA would result in ten times the compliance costs for taxpayers compared to the amount of revenue that it would raise. These onerous reporting requirements have caused many Americans living abroad choosing to renounce their U.S. citizenship rather than continue to face the burdens such citizenship imposes on them.

U.S. States

Even if you live exclusively in the United States, establishing tax residency can be complicated for people with connections to multiple states. Where physical presence can be established based on a number of days, most states determine residency to be established if a taxpayer spends 183 days in that state. Exceptions abound, however: New Mexico requires 185 days, Hawaii uses 200 days, while residency in Idaho is established at 270 days.

On more complicated residency questions, states fall back on the more vaguely-defined determination of a taxpayer’s “domicile.” States establish this based on multiple factors, including the state a taxpayer is registered to vote in, where their spouse and children live, the state their driver’s license belongs to, the location of a taxpayer’s bank, and so on.

This question can become particularly tangled when a taxpayer is attempting to change their domicile, particularly when trying to escape high-tax states for low-tax ones. Billionaires attempting to flee California’s wealth tax, for example, might have to liquidate any physical connection they still have to the state of California, including property, business interests, and so on. Aggressive states often use any lingering presence to claim that a taxpayer’s domicile has not truly changed.

Additionally, many Americans remain unaware that they can owe income tax to states even if they are nonresidents. Many states require nonresidents to file an income tax return based on even just a single day’s work in that state, even if it was for a conference or working vacation visiting family.

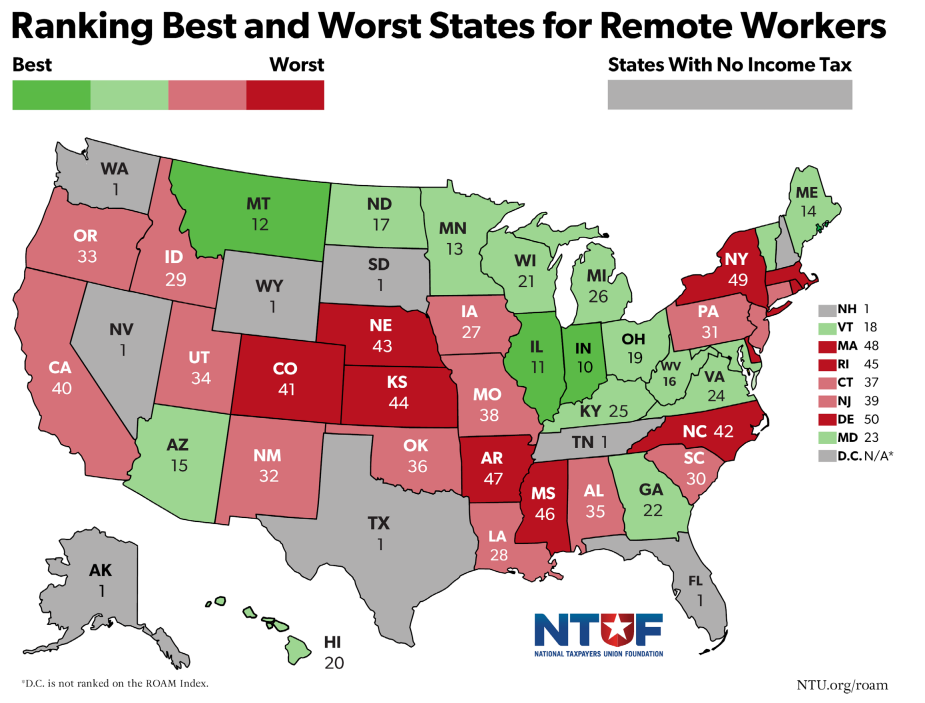

Some states have taken measures to limit this irrational burden. NTUF’s Remote Obligations and Mobility (ROAM) Index tracks the safe harbors states provide to short-term nonresident workers, with the gold standard being states like Indiana, which does not require nonresidents to file a tax return until they spend more than 30 days working in-state. Additionally, some states have entered into bilateral reciprocity agreements to allow taxpayers with connections to each state to only file taxes on income earned in their states of residence.

Conclusion

So while Shakira’s hips don't lie, the apparent simplicity of establishing residency can. Taxpayers who live and work in different countries, and even different American states, can face complexity as significant and costly as that which enmeshed the Colombian music icon. Tax officials and legislators coming up with their own unique flair on these sorts of determinations are not doing taxpayers any favors.

Fortunately, reform is straightforward. FATCA and FBAR have proven to be byzantine messes that cost taxpayers far more than tax money. Reform at the state level should involve reining in overzealous tax administrators and establishing reasonable safe harbors for nonresidents performing short-term work in a state.

Taxes are complicated enough when you know who you’re supposed to pay them to. Spain’s creative justifications for taxing a successful artist receiving a well-deserved judicial rebuke are a step in the right direction.

1 Shakira was also separately indicted for tax fraud based on similar claims by Spanish authorities that she should have paid Spanish tax between 2012 and 2014, a case which was ultimately settled with an $8.5 million fine as part of a deal to avoid prison. The 2011 case remained separate as it was outside the country’s statute of limitations for tax fraud prosecution.