New York’s “Convenience of the Employer” Rule Is Back in Court

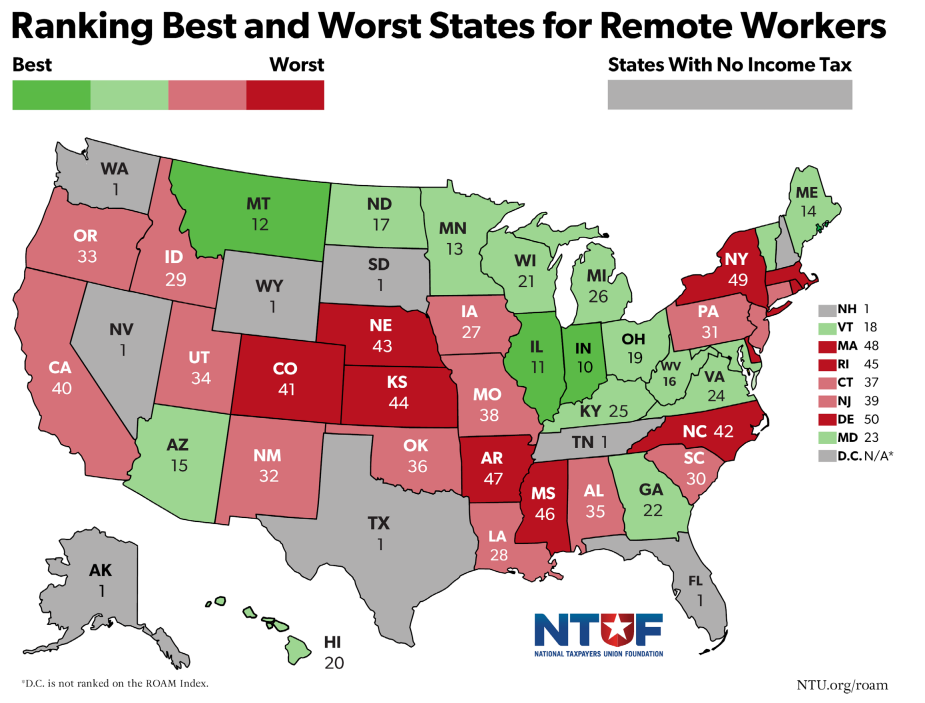

NTUF has long ranked states based on how burdensome their tax codes are to remote and mobile workers. Our Remote Obligations and Mobility (ROAM) Index ranks states based on a few factors — one of which is whether a state taxes remote workers even after they leave the state.

No state enforces such a policy more comprehensively or aggressively as New York. But that could soon change. Last week, New York’s third appellate division heard arguments on a case challenging the state’s “convenience of the employer” rule.

Despite its name, this rule is anything but convenient. In the vast majority of states, Americans pay income tax based on the state where they are physically located while working. New York, on the other hand, says that anyone working remotely for a New York-based employer owes New York state income tax so long as it is a matter of “employer convenience” rather than necessity.

Not only is New York’s position completely illogical, it also can subject a remote-working taxpayer to double taxation. Normally, states offer credits for taxes paid to other states. But if a taxpayer is physically working in another state, that state may be disinclined to offer a credit for taxes paid to New York.

Beyond this, New York’s definition of “convenience” is narrow, to put it mildly. During the pandemic, New York told millions of workers, including Connecticut-based law professor Edward Zelinsky, not to come into their New York offices, to avoid public spaces, and to stay home.

Yet, in oral arguments last week, New York took the position that it was merely a matter of “convenience” for Zelinsky to work from home. After all, he could have worked from home in New York, apparently. Never mind that that would have involved buying a New York house — not doing it was merely a matter of convenience.

It remains to be seen whether even the notoriously deferential New York state court system will buy those arguments. But should New York’s rule fall, it would likely spell the end of the rule in most other states where it exists as well. While eight states have some version of the convenience of the employer rule currently in effect, most are either directly in response to New York or much more limited in scope.

States That Tax Nonresident Remote Workers Even After They Leave

State | Who Can Be Affected? |

Alabama | All remote workers |

Connecticut | Residents of states that tax remote workers |

Delaware | All remote workers |

Nebraska | Nonresidents spending at least 7 days physically working in Nebraska |

New Jersey | Residents of states that tax remote workers |

New York | All remote workers |

Oregon | Managers only |

Pennsylvania | All remote workers |

For example, Connecticut and New Jersey only apply a convenience of the employer rule to nonresidents who are residents of a state that imposes a convenience of the employer rule of their own. Delaware and Pennsylvania adopted their own versions of the rule in response to New York. Nebraska and Oregon limit the application of their rules to specific circumstances.

Even legislators or policy workers in states that do not impose such a rule need to be aware of it, because it often appears without any legislative action. In Alabama, the state Department of Revenue unilaterally reinterpreted an existing statute in 2023 to give itself the power to tax nonresidents working out of state, without any legislative input. This is why adopting simple language to protect taxpayers against being harassed by overzealous state revenue department officials is so important.

And if you don’t like your state’s ranking on the ROAM Index and want to fix it, we’ve got lots of other ideas!