According to updated estimates from NTU Foundation, President Biden’s student debt cancelation action this week could ultimately cost taxpayers around $400 billion, up from our initial expectations. This estimate does not include the effects of a lower cap on income-driven repayments, the extension of the loan payment moratorium through December 2022, or the exemption from federal income tax for student debt cancelation, or the effects of the policy on long-term program integrity.

NTUF’s methodology is detailed further below, but based on some conservative assumptions we believe debt cancelation could result in between $386 billion and $405 billion in net costs to taxpayers. We previously relied on a $330 billion estimate from the Penn Wharton Budget Model which did not account for President Biden’s additional $10,000 in debt cancelation for up to 27 million Pell Grant recipients.

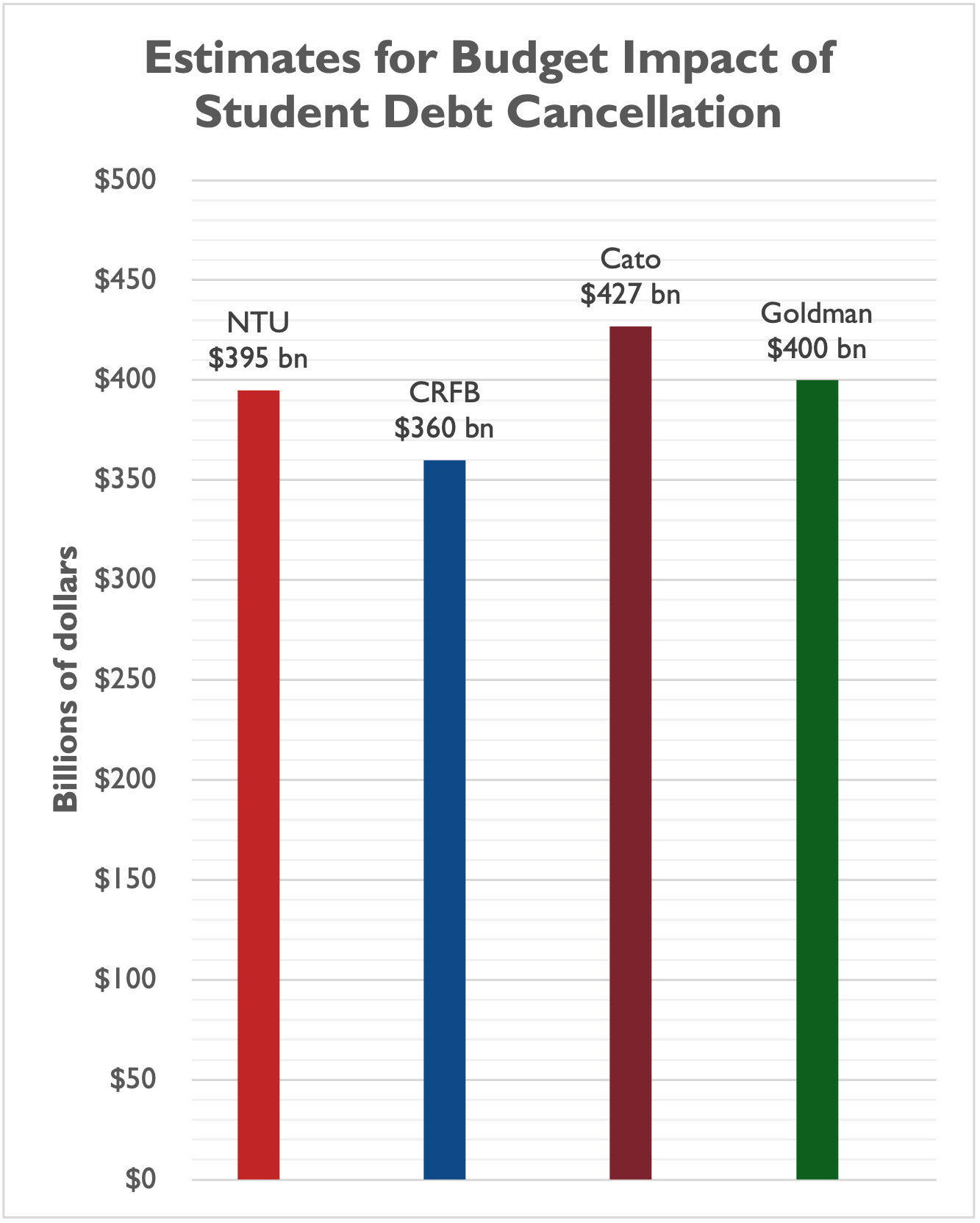

Our midpoint estimate of $395 billion in net costs to taxpayers – for the $10,000 in debt cancelation for non-Pell Grant recipients and $20,000 in cancelation for Pell Grant recipients – is near other estimates published this week from the Committee for a Responsible Federal Budget (CRFB), the Cato Institute, and Goldman Sachs.

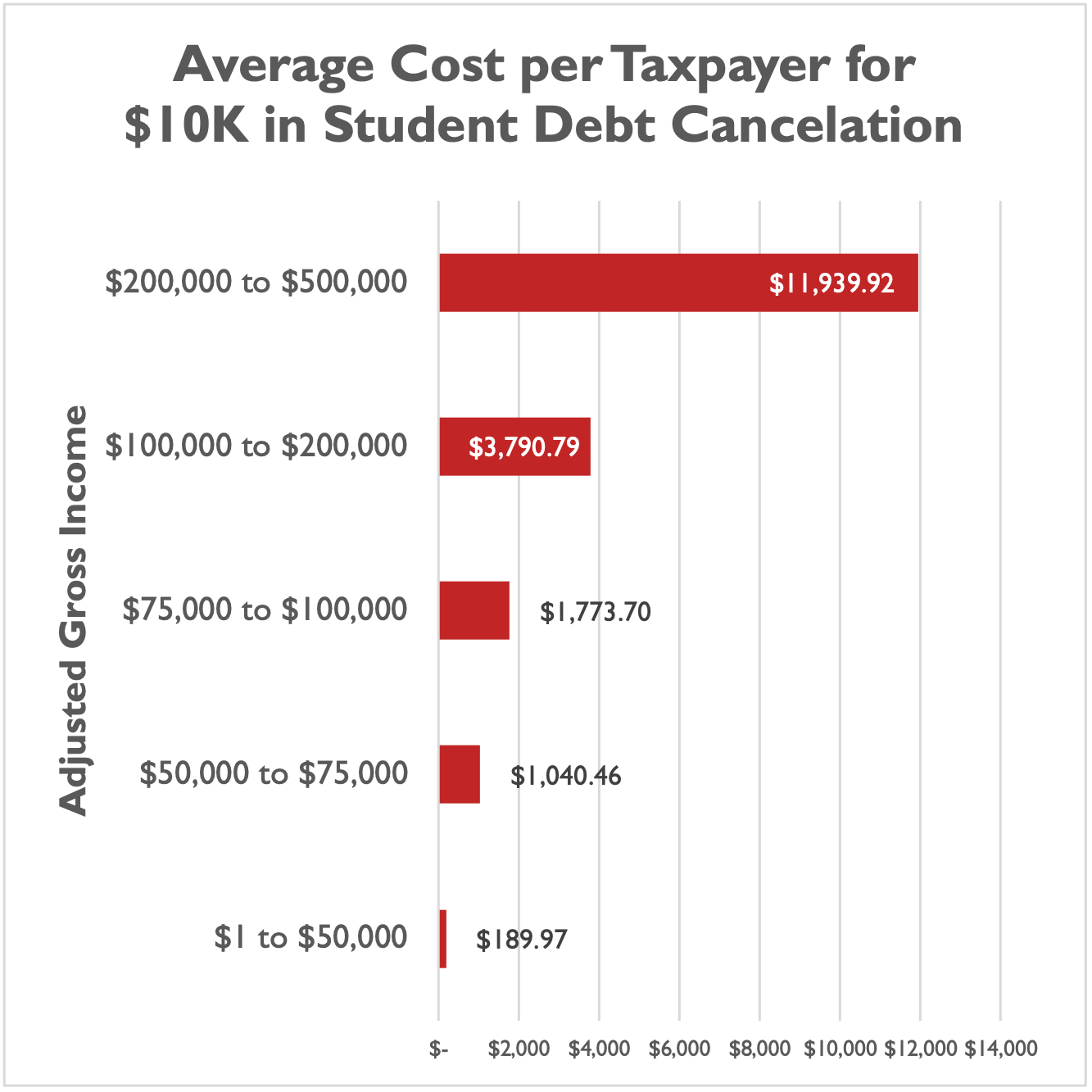

Using this new estimate, we calculate that the average burden per taxpayer in the U.S. is $2,503.22, up from our earlier estimate of $2,085.59.

Accounting for the uneven distribution of tax burdens across different income levels, we estimate that low-income taxpayers making between $1 and $50,000 would bear an average burden of $190, while taxpayers making between $100,000 and $200,000 would bear an average burden of $3,790.

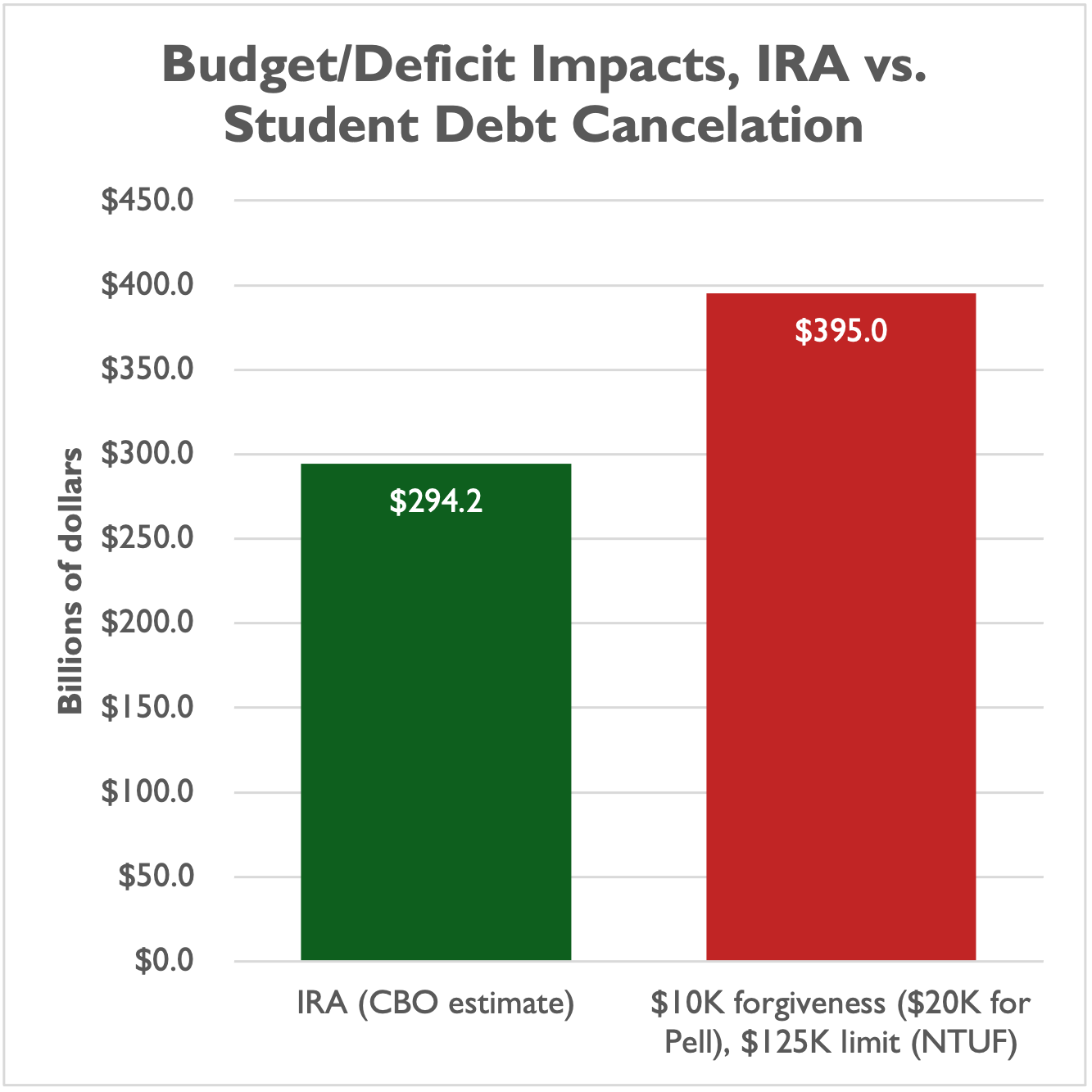

Looking through a borrowing and deficits lens instead of a taxpayer lens, this policy more than wipes out the entire first decade of projected deficit reduction from the Inflation Reduction Act (IRA). In fact, the deficit increase from student debt cancelation exceeds the deficit reduction of the IRA by $100 billion, or more than a third.

In the long run, we remain concerned about the effects that one-time, broad-based debt cancelation will have on future borrowers and on higher ed institutions. To the extent future borrowers, or colleges and universities, expect that there will be additional rounds of debt cancelation, borrowers may make riskier decisions and colleges and universities may raise their prices and fees higher than they otherwise would. The Federal Reserve Bank of New York, for example, has found that a dollar of subsidized student loans leads to $0.60 in tuition increases at colleges. Government administrators responsible for the federal student loan programs might also not work as hard to look at each loan's serviceability, in anticipation of future debt cancelation.

Methodology for $395 Billion Estimate

We used data from the Education Department, the White House, and the Education Data Initiative.

As of Q2 2022, there were 14.6 million borrowers with $10,000 of outstanding student loan debt or less, with outstanding debt for this cohort totaling $73.3 billion.

There were an additional 30.7 million borrowers with more than $10,000 of outstanding student loan debt. Starting with a simple assumption that each of these borrowers receives $10,000 in debt cancelation yields a total of $307 billion in outstanding debt canceled.

Before accounting for income limitations or the additional debt cancelation for Pell Grant recipients, we reach a simple calculation of $380.3 billion in debt canceled. We assume, as the White House does, that roughly five percent of this universe is not eligible for cancelation on account of the income cutoff. A five-percent reduction in the cost of this debt cancelation yields a total of $342.2 billion.

The White House estimates that 27 million Pell Grant recipients will be eligible for additional relief. How much additional relief that cohort averages will help determine the cost of canceling additional debt for Pell Grant recipients.

It is reasonable to assume that a significant portion of these 27 million eligible recipients will receive a full, additional $10,000 in debt cancelation. Seventy percent of borrowers with more than $10,000 in student loan debt also have student loan debt above $20,000. Assuming 70 percent of these 27 million receive the full additional $10,000, the cost of additional cancelation for those 18.9 million recipients alone is $189 billion.

For the remaining 30 percent of Pell recipients, 8.1 million in total, one could assume a mid-point average of $5,000 in student debt cancelation, or a low-end estimate ($3,300 average per borrower) or a high-end estimate ($6,700 average per borrower). That yields a cost range of $26.7 billion to $54.3 billion.

This yields a total potential cost of cancelation of between $557.9 billion and $585.5 billion. However, only 86.5 percent of the federal student aid portfolio is actually held by the federal government; FFEL loans that make up the other 13.5 percent may not be eligible for cancelation. Eliminating these loans from debt cancelation yields a conservative estimate of $482.6 billion to $506.5 billion in debt cancelation.

Baseline assumptions would also account for some of that balance permanently defaulting in the future, and some of that balance permanently being forgiven as a result of eligibility for existing loan forgiveness programs.

For example, $146.8 billion of the federal government’s $1.3962 trillion loan portfolio (10.5 percent) is in default. According to the Education Data Initiative, another 6.7 percent of student borrowers are eligible to apply for forgiveness.

We assume a conservative 10 percent of loan balances default and another 10 percent of balances are eventually forgiven through public service and income-driven repayment programs under current law, and this yields an estimate of $386 billion to $405 billion in net costs to taxpayers.

As noted above, this does not account for the costs to taxpayers borne by 1) the new five-percent cap on income-driven repayment, 2) the extension of the payment moratorium through December 2022 (through April 30 of 2022, the payment suspensions cost at least $4 billion per month), and 3) the exemption from federal income tax for student debt cancelation. These three provisions alone will add billions of dollars, if not tens of billions of dollars, to the 10-year costs of debt cancelation.

It is also worth noting that these estimates are relative to the government's projection of the costs of student loans, which uses a faulty methodology that does not fully account for the risk of default. For years, the Department of Education has projected that the Direct Loan program will save money. An alternative analysis of student loan programs by the Congressional Budget Office using a market-based fair-value accounting method, as well as a new review by the Government Accountability Office, show that this simply is not true.

Now, in addition to the risk of some borrowers defaulting, the President can determine that some people simply do not have to pay back all or a portion of their loans. With President Biden's student loan debt discharge, program integrity could worsen and drive up future costs.