Key Facts

- The Inflation Reduction Act of 2022 included nearly $80 billion in supplemental funding for the IRS with the intention to fundamentally transform the Service.

- We began “Grading the IRS” to compare the Service’s self-reported success against initiatives that should be undertaken for meaningful transformation.

- In this second annual edition of “Grading the IRS,” the Service earns better grades in taxpayer service, modernization, and tackling the tax gap, contingent upon the successful completion of recently announced initiatives.

Introduction

The IRS continues to struggle in the court of public opinion despite improvement efforts spanning decades and recent legislative changes. The Inflation Reduction Act (IRA) of 2022 included nearly $80 billion in supplemental funding for the IRS with the intention to fundamentally transform the Service. With just $26 billion of its funding remaining, the IRS is shifting away from the Biden-era plan that guided its transformation in light of progress that has been more limited than promised.

In late 2024, we analyzed the IRS’s self-reported successes in transforming its taxpayer services, upgrading information technology, and closing the tax gap. We graded the IRS against outcomes that we would expect from a truly transformational change. At the time, we gave grades of C, D, and C for those categories, respectively. With the change in Administration, an uneven overhaul of the IRS workforce, and swift passage of an expansive new tax law, the IRS is making some improvements in all three areas.

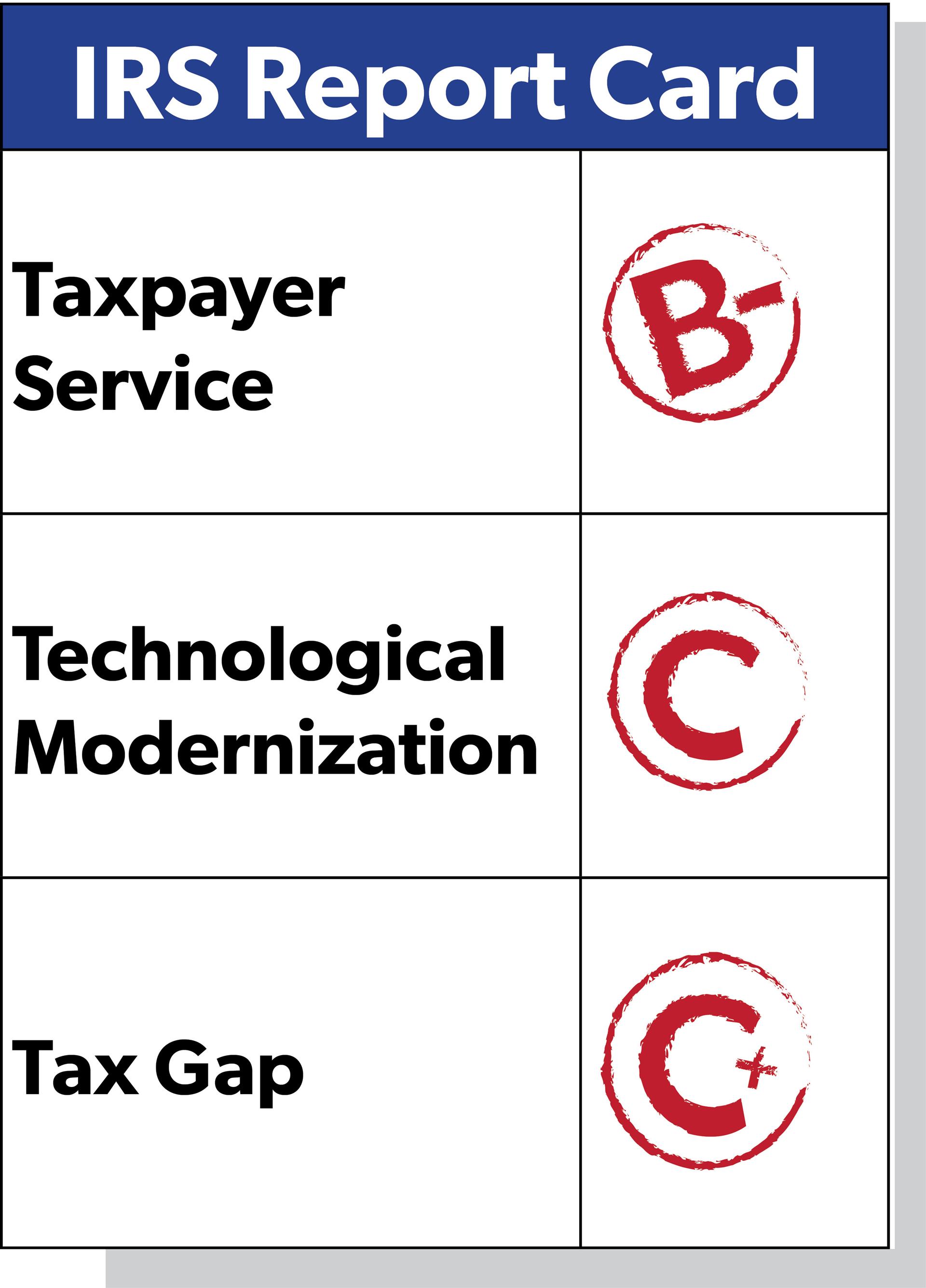

In light of information released during 2025 and early 2026, including data on the last tax filing season, we are conditionally upgrading the IRS’s grades. The IRS has earned a B- for taxpayer service, a C for technological modernization, and a C+ for closing the tax gap. While we are enthused about recent progress in improving taxpayer services and information technology, these letter upgrades are conditional upon the completion of deliverables that the IRS has promised to release soon.

Taxpayer Services: B- (Conditional)

Recent improvements to taxpayer services warrant a higher grade than our first report card, but the B- provided here is conditional upon several factors. First, we anticipate forthcoming details about the 2026 tax filing season and hope to see an overall smooth experience for taxpayers. In addition, we hope to see the impending rollout of new metrics, including an alternative to the Level of Service metric, to provide better insight into the taxpayer experience. Finally, we hope to see technology upgrades that will modify both how taxpayers interact with the IRS and how IRS agents manage taxpayer information.

Accessibility of Telephone Services

Taxpayers in need of assistance are able to contact the IRS on the phone, online, or at in-person locations. In recent years, 80% of all taxpayer assistance was provided over the phone. Accurately measuring both the quality and quantity of telephone assistance provided to taxpayers remains a crucial indicator of the adequacy of the IRS’s taxpayer service performance.

The IRS continues to make incremental improvements to its telephone services while also making a welcome overhaul to service metrics. For the third year in a row, the IRS exceeded its 85% Level of Service target, reaching 87% for the 2025 tax filing season. As we have previously noted, this metric means the IRS answered 87% of the phone calls to the Accounts Management phone line that were not otherwise routed to automated services or dropped. Since the Level of Service metric does not account for the majority of taxpayer calls, it is frequently exaggerated.

Other phone lines continue to go unanswered, yet at a rate that is slowly improving. The Taxpayer Protection Program (TPP) line and the Installment Agreement/Balance Due Line had levels of service of 29% and 46% last filing season, up from 17% and 42% respectively.

Inefficient phone services do not only affect the taxpayer making the call. The IRS Advisory Council (IRSAC) notes that, while specialized phone calls go unanswered, agents are idle waiting for phone calls to the main line, where answered calls are included in the headline Level of Service figure. In our last report, we noted that the IRS implemented a callback feature to address unanswered calls and we suggested increasing services provided over the phone and using more transparent metrics to demonstrate a clearer picture of taxpayer access to service representatives.

In response to these concerns, the IRS is now implementing alternative metrics going forward to measure its level of service, according to IRSAC and the National Taxpayer Advocate. IRSAC’s latest report lauds the IRS for improving its Level of Service measurements with the new Enterprise Service Completion Rate. The National Taxpayer Advocate notes that this metric will provide a holistic view of live assistance provided across multiple methods including new technology and recommends the IRS expand and utilize this metric by the end of the current fiscal year.

Availability of Online Tools

The expanded use of modern technology, including for taxpayer services, remains an area where the IRS fell far short of expectations for its transformation with IRA funds. In our first report grading IRS modernization, we compared the IRS’s vague proclamations of success with the results actually being reported. This led us to provide a D grade, citing a lack of results. Due to a shift in approach to its consideration of online tools, we can now provide the IRS with a C grade, yet much work still needs to be done.

A major success touted by the prior Administration in its improvements to online taxpayer service was creation of the Document Upload Tool, providing taxpayers with an online resource to quickly send documents to the IRS. We previously noted that IRS modernization resources would have been better allocated toward truly transformational projects such as upgrading backend systems and legacy technology that has been in use for six decades. Unfortunately, our concerns were proven true. The National Taxpayer Advocate flags that the Document Upload Tool, one of the last Administration’s most touted successes, does not have any backend system to process uploads. Therefore, the IRS often has to print uploaded documents and manually route them to employees.

The current Administration has taken a different approach to revamping how the public interacts with the IRS online. In early 2025, simple, yet effective, changes were made to make the IRS website more intuitive, addressing a challenge we called attention to alongside the Taxpayers for IRS Transformation (Taxpayers FIRST) Advisory Board. One change to the website included moving the login button from the lower middle of the page to the top right corner as it appears often across the internet. Officials report that this change would have otherwise been delayed due to red tape.

The Administration shifted focus to backend tools that will expedite processing and is also working to make more notices accessible online. Backend improvements include work to implement an application processing interface (API) allowing multiple systems to communicate among each other, which may also enhance phone services by allowing representatives to have access to more taxpayer information. The IRS also added 22 new forms to its website for taxpayer access and allowed nine new information returns to be downloaded via Individual Online Accounts.

While we appreciate the IRS’s continued efforts to expand access to services and documents online, as well as a renewed focus on backend technology, work must continue to ensure taxpayers see noticeable changes in online service.

Assistance Provided In Person

Most in-person taxpayer interactions occur at Taxpayer Assistance Centers (TACs) or through Volunteer Income Tax Assistance (VITA) and Tax Counseling for the Elderly (TCE) programs. While the latter two programs went relatively unchanged this past year, the IRS made some concerning changes to TACs. However, it continued recent efforts to expand service hours at TACs during tax filing season by offering weekend and evening availability well after the end of the filing season in both 2025 and 2026.

One area of concern is the requirement for taxpayers to make an appointment to receive service at TACs. The Treasury Inspector General for Tax Administration (TIGTA) reports that, during the last filing season, its investigators were denied service at several TACs as they did not schedule an appointment in advance despite prior practice that TACs also accept walk-ins if assistance is available.

In addition, the Administration recently announced the closure of nine TACs and did not offer Community Assistance Visits during the last tax filing season. Community Assistance Visits act as “pop-up” TACs in communities that are more than a 2 hour drive from the nearest TAC. These measures will certainly limit taxpayer access to in-person services. To fill the demand for live communication with an IRS agent, the IRS has piloted a Web Service Delivery (WebSD) program for taxpayers to schedule a virtual appointment with an IRS agent. Yet, this may not be as effective as in-person visits.

We previously recommended that the IRS improve data collection and reporting regarding service at TACs so the public can better understand what drives an increase or decrease in taxpayer contact with TACs. Until phone and online services demonstrate significant improvement, the IRS must continue to staff and support in-person assistance centers.

Technological Modernization: C (Conditional)

In our first “Grading the IRS” report, we highlighted the lack of long-term vision in the IRS plan to modernize its technology. No progress was made toward most important upgrades, such as replacing the severely outdated Individual Master File, while resources were spent replacing hardware that continues to rely on inefficient software.

Given those shortcomings, an overall shift in direction under the Trump Administration is welcome. Yet, our grade improvement in technological modernization is conditional, mainly due to the fact that we have yet to see an updated modernization plan after the obsolescence of the prior Strategic Operating Plan. The IRS plans to release an updated plan this summer, which we hope will be delivered in a timely fashion with clear benchmarks for key changes.

Shifting Modernization Strategy

Last year, we analyzed the progress of several new IRS modernization projects funded by the Inflation Reduction Act. This included the Paperless Processing Initiative, the Simple Notice Initiative, and changes to Individual Online Accounts. While we would like to see some of this work continue, we acknowledge that many of these initiatives would not result in the type of transformational change that could have been made possible with the increased funding, much of which was largely reserved for enforcement activities. Instead, the IRS should have focused on replacing outdated software that brings the risk of outages, security failures, and user difficulty.

The Trump Administration has announced it is now focusing on replacing legacy systems and ensuring existing technologies are interoperable. In April 2025, the IRS changed its definition of a legacy system from those that are at least 25 years old or using obsolete technology to those that do not align with the IRS mission. The IRS also hosted a hackathon event in April 2025 to develop an application program interface (API) to improve communication and data sharing across IRS systems. While it is unclear what was achieved at the hackathon, the Department of the Treasury announced a contract with Palantir to create a unified API in September 2025. Nearly six months later, we have yet to hear a status update on this work.

The use of legacy systems such as the Individual Master File and Business Master File is one of the IRS’s biggest challenges. Thus far, it has failed to make meaningful progress replacing these systems since the 1990s. Watchdogs consistently reported that, despite the influx of funding, the IRS under the Biden Administration failed to make any meaningful progress in retiring or replacing these systems.

The shift in focus toward replacing legacy systems and ensuring technologies are compatible with each other could result in more progress in IRS modernization than we have seen in recent years.

Leveraging Innovative Technologies

In early 2025, President Trump issued an executive order directing the federal government to remove barriers to usage of artificial intelligence. In response, the IRS released an interim policy for artificial intelligence use specifying that the IRS should maintain an inventory of artificial intelligence use cases to help fill gaps in current reporting.

The Government Accountability Office reports that some IRS contractors provide services to taxpayers using artificial intelligence and that these use cases are not properly identified in the artificial intelligence inventory. While the IRS has not released the inventory publicly, it is important to ensure that all taxpayer and IRS employee uses of artificial intelligence are included in the list.

More broadly, TIGTA believes that artificial intelligence will play a larger role in the 2026 tax season. The Department of the Treasury has signalled that artificial intelligence will be used to replace some of the functions of employees lost to reductions in force.

TIGTA also highlights key achievements in improving efficiency through use of artificial intelligence at the IRS. For example, the IRS has incorporated machine learning into the audit selection process, which may increase efficiency.

Artificial intelligence is an important tool for the IRS in its modernization process, but should be used with caution. We have previously pointed out that practitioners warn artificial intelligence may not be able to distinguish between routine anomalies and intentional wrongdoing when selecting taxpayers for audit. Artificial intelligence could also produce errors, such as by oversimplifying complex tax laws in communication with taxpayers—a process deemed “symplexity” by tax experts. Finally, the greater the prevalence of AI in tax administration, the more important that “human backstops” are available for taxpayers to contact when technology fails them. Last year’s staffing reductions to the Taxpayer Advocate Service, for example, could make it difficult for taxpayers to resolve individually complicated issues with the IRS.

Tax Gap: C+

It is unsurprising that the Biden Administration’s IRS transformation efforts focused on tax enforcement, given that a significant portion of the $80 billion in supplemental IRA funding was earmarked for enforcement. We graded the IRS a C- in these efforts for singling out niche groups of taxpayers, failing to implement new metrics for defining the tax gap, and an overall lackluster strategy to close the tax gap.

The Trump Administration has not announced notable initiatives to close the tax gap. While this means that taxpayers are spared from being audited on problematic criteria, as was the case under the Biden Administration’s large partnership examinations, it also means we are unsure whether new tax enforcement initiatives are ongoing. Reports indicate that, while there has been a recent decline in some high-income audits, enforcement revenue has increased this fiscal year and examinations remain thorough.

There are encouraging signs of change underway that we believe warrant a modest grade improvement in IRS efforts to close the tax gap. As NTUF has often pointed out, good tax compliance begins with clear instructions and comprehensible guidance. For instance, the Service recently established a public comment period for its decision to repeal problematic guidance on what the government called “basis shifting” in partnership transactions. The IRS has also issued several rounds of guidance in an attempt to simplify compliance with the highly complex Corporate Alternative Minimum Tax; the ultimate aim, according to a Treasury news release, is to “enable Treasury to re-propose the entire CAMT regulatory framework to reflect stakeholder feedback and ensure that final rules that are workable and predictable.”

In addition, during 2025, the IRS began improving its alternative dispute resolution (ADR) programs, which NTUF believes “will decrease litigation costs, increase taxpayer accessibility to dispute resolution, and increase taxpayer confidence.” A Post Appeals Mediation pilot program, along with other measures to encourage ADR and Fast Track Settlements, could be crucial this year into next, as they take root. NTUF looks forward to assessing these results in a future report card.

Conclusion

Addressing longstanding concerns, such as the inadequate Level of Service metric, shifting focus from poorly developed taxpayer-facing tools to backend upgrades, and making systemic changes in direction toward a more transformational approach call for a rising grade in taxpayer services. Similarly, shifting focus toward longstanding technological modernization priorities is a notable improvement. Despite this, we have yet to see some of the most critical determinants of real progress in these two categories. As such, our grades for taxpayer services and modernization are conditional. While the Trump Administration has not announced new initiatives to close the tax gap, we are encouraged by recent efforts to support voluntary tax compliance, warranting a modest increase in our score.

There are many further improvements that the IRS must make, many of which will rely on technological modernization. With less than three years left of the current Administration, we hope that IRS leadership can soon present more results from its efforts—as well as more detailed strategic plans—alongside a successful 2026 tax filing season.