Policy Paper No. 176 PDF Version Press Release

I. Summary of Findings

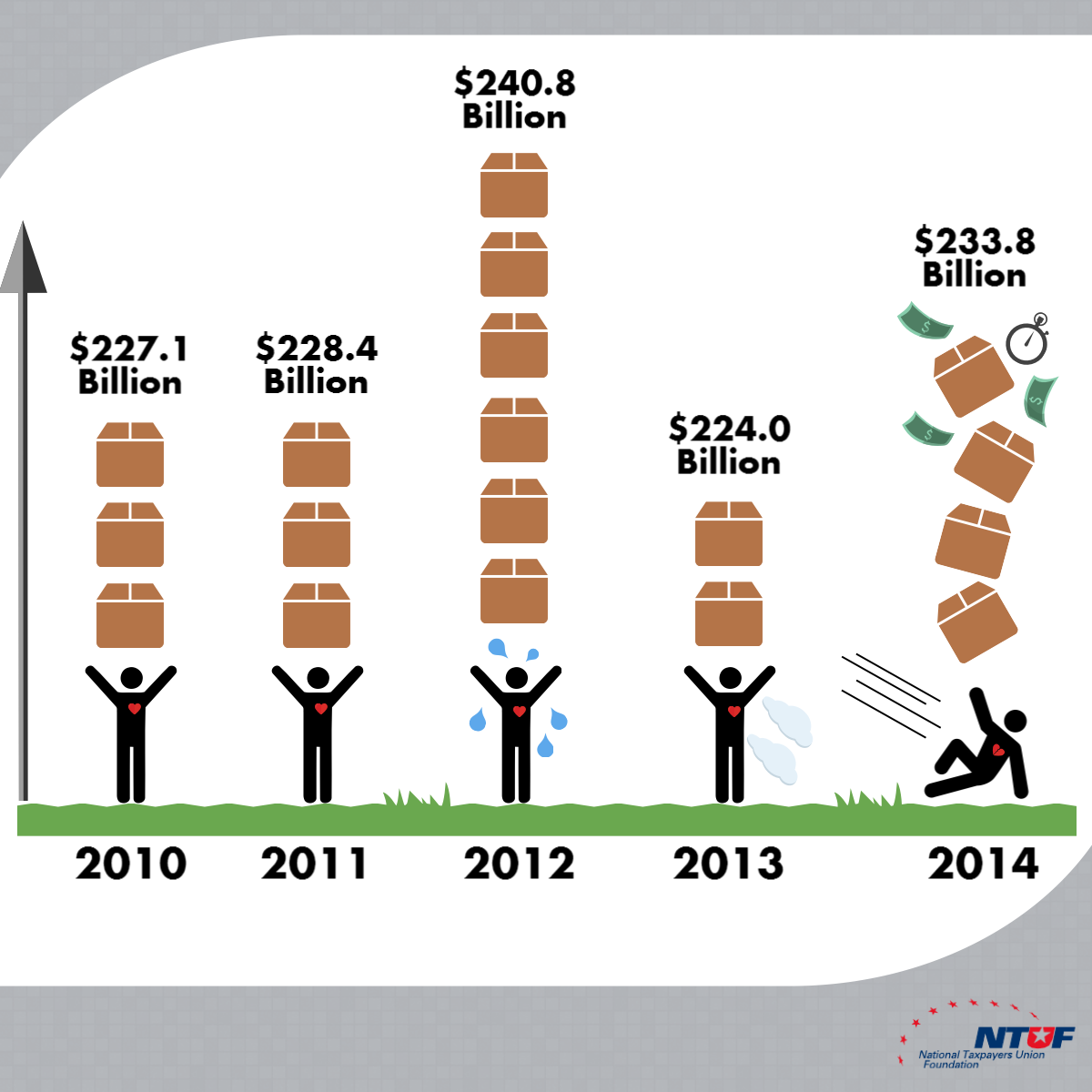

National Taxpayers Union Foundation’s (NTUF’s) annual analysis of tax complexity in the United States reveals yet another year of unconscionable burdens on America’s taxpayers and businesses, finding that compliance with the federal income tax cost the economy $233.8 billion in productivity last year.

Out-of-pocket expenses like software and other tax preparation assistance tallied $31.7 billion, combined with an estimated $202.1 billion cost due to 6.1 billion hours in lost labor spent complying with the Tax Code this past year.

II. Introduction

The Congress shall have power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration.

Ever since the United States Congress ratified the words above in the Sixteenth Amendment to the Constitution, Americans have been subjected each year to the income tax. The convoluted process of preparing and filing tax forms has been a source of humor for comedians dating back at least to the era of Burns & Allen and Bob Hope, but all too often, it is also a source of real stress, fear, and dread for many taxpayers. The system today bears little resemblance to the relatively simple one that was envisioned and developed in 1913.

In the century since then the Tax Code has grown astonishingly complex. Its annual enforcement and compliance costs require tens of billions of hours, hundreds of billions of dollars, and thousands of federal employees. The sheer complexity of the Code has spawned a multibillion-dollar industry, made up of professionals who spend years training in order to help individuals and businesses navigate the system (and frequently, even that is not enough to ensure accurate filings). Hardly a day goes by during the lead up to Tax Day that we don’t hear of a security breach or technical issue that compromises the sensitive, personal information taxpayers send to the Internal Revenue Service each year in April. And when that does happen, taxpayers must confront a daunting, weeks- or even months-long bureaucratic process through a system that is becoming increasingly overwhelmed and unable to offer assistance when needed.

The escalating economic costs, combined with the IRS’s deteriorating ability to protect and assist taxpayers, make it clear that the current system needs to change. Simplifying the laws would immediately and directly improve the country’s economic condition as well as taxpayers’ everyday lives, and should be an urgent priority for lawmakers on Capitol Hill. In the words of the IRS’s National Taxpayer Advocate Nina Olson: “… I believe we need fundamental tax reform, sooner rather than later, so the entire system does not implode.”[1]

It is the aim of this paper to highlight the current condition of the U.S. tax system – namely, its mounting complexity and costs – and how that harms taxpayers.

III. Complexity Continues to Grow

According to recent estimates from the National Taxpayer Advocate, Americans spend an average of 6.1 billion hours annually complying with the Internal Revenue Code’s (IRC) requirements.[2] It is difficult to fully comprehend how staggering that figure is even when one measures it against a more familiar context: that is just over 696,347 years, the equivalent of 152.5 million 40-hour workweeks. It would take 59,580 American workers, who begin employment at age 18 and work every single week of their lives with no days off, until reaching the full Social Security retirement age of 67, to account for that much time.

We can arrive at an estimate of the value of this time by thinking of it in terms of private sector labor costs. According to the Bureau of Labor Statistics (BLS), U.S. employers spent an average of $33.13 per hour worked on total non-federal civilian employee compensation in December 2014 (that figure includes wages and salaries as well as benefits).[3] For 6.1 billion hours of such work, then, employers would have paid $202.093 billion, valuable labor that will instead be lost to Tax Code compliance. Add to that the $31.72 billion in estimated out-of-pocket costs taxpayers spent on software and professional preparation services[4], and the total economic value of the compliance burden can be valued at $233.813 billion.

Unfortunately for taxpayers, complexity in the Tax Code does not appear to be waning by any measure. Perhaps the most tangible way to examine the growth of the Code and its overwhelming complexity is to look at its physical length: the Advocate’s most recent count in 2012 showed that the statutes contain 3,951,104 words (just over five times the length of the entire King James version of the Bible) [5],[6]. In 1991 the IRC contained a staggering 45,739 sections, sub-sections, and cross-references; by 2012 that figure had reached 66,812 – a 46 percent increase. And since 2004, the Advocate reports that there have been 4,107 changes to the IRC, an average of more than one every single day.

For many years, National Taxpayers Union tracked the length of the Form 1040 and its accompanying instruction booklet – materials that many American taxpayers are all too familiar with on a yearly basis. In 1935 the Form was a single page consisting of 34 lines, with two pages of instructions. Now, it has 79 lines over two pages, requiring the equivalent of 209 pages of instructions. While the IRS published a far shorter document than was published for 2013, the latest instruction booklet does not include directions for common Form 1040 schedules, as last year’s did. NTUF accounted for this fact in the table below.

| Table 1. Form 1040 Form and Instruction Booklet Length | |||

|---|---|---|---|

| Tax Year | Lines, Form 1040 | Pages, Form 1040 | Pages, Form 1040 Instruction Booklet |

| 2014 | 79 | 2 | 209** |

| 2013 | 77 | 2 | 206* |

| 2012 | 77 | 2 | 214 |

| 2011 | 77 | 2 | 189 |

| 2010 | 77 | 2 | 179 |

| 2005 | 76 | 2 | 142 |

| 2000 | 70 | 2 | 117 |

| 1995 | 66 | 2 | 84 |

| 1985 | 68 | 2 | 52 |

| 1975 | 67 | 2 | 39 |

| 1965 | 54 | 2 | 17 |

| 1955 | 28 | 2 | 16 |

| 1945 | 24 | 2 | 4 |

| 1935 | 34 | 1 | 2 |

| Notes: | |||

| *Excludes one extra page in the IRS’s online PDF version regarding donations for Philippines typhoon relief. | |||

| **The IRS did not include instructions for Form 1040 schedules in this edition of the instruction booklet. The 2014 For 1040 instructions amounted to 104 pages. Instructions for Form 8949 and Schedules A, C, D, E, F, R, and SE (which were included in the 2013 Form 1040 instructions) totaled 105 pages. | |||

The Tax Code accounts for a disproportionately high percentage of the government’s overall paperwork burden. Each year the Office of Management and Budget tracks the total hours each agency’s information collection requirements impose on the public and publishes the results online. While in some years an agency’s burden hours may actually recede from the previous year due to changes in the law, an agency’s discretionary actions, or even economic conditions, the net change in the burden can often serve as a proxy for how much more complicated the agency’s workload has become. The graph below shows how new statutory requirements changed the burden hours for the Department of Treasury and the entire government between each fiscal year from 2005-2013.

As Figure 1 shows, the Treasury (largely the IRS) accounts for the majority of the net changes in government paperwork burdens. From Fiscal Year 2005 through 2013, the federal government’s paperwork burden imposed on the public due to new statutes increased, on net, by about 1.3 billion hours.[7] The Treasury’s rose by 838.4 million hours, about 64.5 percent of the total for all federal agencies combined.

This data illustrates that when tax laws change, the effect tends to be realized in additional time burdens. Rarely in recent years have changes in statutes resulted in a net total reduction of paperwork burden. Fiscal Years 2010 and 2011, in the immediate wake of President Obama’s “economic stimulus” efforts, saw an especially large increase in new paperwork due to statute: OMB noted that in 2010, the IRS’s processing of individual income tax returns (identified as “control number 1545-0074”) alone required 319 million hours of additional information collection that year.[8]

Even when gross top-line paperwork hours have receded, the Treasury’s share of the total burden has remained relatively constant, as seen in Table 2 below.

| Table 2. Treasury Paperwork Burden Relative to Government-Wide Total | |||

|---|---|---|---|

| Fiscal Year | Government Paperwork Burden (millions of hours) | Treasury Paperwork Burden (millions of hours) | Treasury Paperwork Burden, Percentage of Government Total |

| 2005 | 8,241 | 6,435 | 78% |

| 2006 | 8,924 | 6,966 | 78% |

| 2007 | 9,642 | 7,631 | 79% |

| 2008 | 9,714 | 7,785 | 80% |

| 2009 | 9,796 | 7,643 | 78% |

| 2010 | 8,783 | 6,780 | 77% |

| 2011 | 9,138 | 6,734 | 74% |

| 2012 | 9,467 | 7,062 | 75% |

| 2013 | 9,453 | 7,007 | 74% |

| Source: Office of Management and Budget. | |||

The Treasury’s paperwork burden imposed on the public has grown from 6.4 billion hours to 7 billion hours over the period from fiscal year 2005 to 2013, and in that time, has never made up less than 74 percent of the burden imposed by all other government agencies combined.

A. Paid Preparation: Luxury, or Necessity?

As the Tax Code becomes more complex, taxpayers are likelier to pay money for professional services or other assistance to help them accurately file returns. The practice has become virtually standard, with the Advocate reporting that in 2013 over 94 percent of filers paid someone or used software to help prepare their returns.[9] According to market research firm IBISWorld, the tax preparation industry generated over $10 billion in revenue in 2014 and was comprised of 318,926 employees across 111,568 businesses.[10]

For several years, National Taxpayers Union has tracked the average fee charged by H&R Block, one of the largest such preparation businesses in the U.S. Perhaps not surprisingly, those fees have steadily increased along with the system’s complexity.

| Table 3. Average Fee Charged by H&R Block | |

|---|---|

| Calendar Year | Average Fee |

| 1980 | $27.36 |

| 1985 | $45.39 |

| 1990 | $49.99 |

| 1995 | $61.77 |

| 2000 | $101.40 |

| 2005* | $145.08 |

| 2010# | $187.93 |

| 2011** | $190.97 |

| 2012** | $189.96 |

| 2013** | $192.24 |

| 2014** | $215.06 |

| Source: National Taxpayers Union, H&R Block. | |

| *Through March 15. #Through March 30. **Through April 30; total U.S. tax preparation fees divided by number of retail returns. | |

| H&R Block’s calculation of the net average fee per return has changed in recent years, sometimes including fees from other services such as Refund Anticipation Loans. | |

Worth noting is that even after adjusting the $27.36 average fee from 1980 for inflation (equal to $77.94 in 2015 dollars), the cost of return preparation has nearly tripled since then, suggesting that the growth in tax complexity is outpacing even the technological and administrative improvements that have been made to professional preparation firms in that time.

B. Affordable Care Act Introduces New Complexities

President Barack Obama’s signature health care reform law, the Patient Protection and Affordable Care Act (PPACA), imposes additional cost and complexity burdens on tax filers.

The IRS website has a section devoted to “Legal Guidance and Other Resources”[11] which links to dozens of separate pages containing informational PDFs, third party resources, and multimedia related to PPACA compliance. These include:

- 47 different “concise, timely and useful” tips under the “Health Care Tax Tips” page;

- 15 flyers, publications, and trifolds totaling 87 pages;

- 11 YouTube videos;

- 7 podcasts; and

- 1 webinar on the Indoor Tanning Excise Tax.

The IRS also lists, in electronic form, many of the various legal guidances and regulatory decisions it has issued regarding PPACA implementation and compliance. On its “Affordable Care Act Tax Provisions” page, the IRS links to 1,865 pages of regulations (including proposed, temporary, and final versions), Q&A documents, notices, news releases, and procedures. The “Affordable Care Act Legal Guidance and Other Resources” page has even more documentation, many of which overlap with those listed on the Tax Provisions page:

| Table 4. Pages of PPACA Legal Guidance, IRS Website | |

|---|---|

| Section | Pages |

| Regulations | 1,077* |

| Treasury Decisions | 1,377* |

| Notices | 669 |

| Revenue Procedures | 100 |

| Revenue Rulings | 12 |

| Total | 3,322 |

| Source: https://www.irs.gov/Affordable-Care-Act/Affordable-Care-Act-of-2010-News-Releases-Multimedia-and-Legal-Guidance. | |

| *Note: Sections contained broken links to REG-140789-12 and TD 9708. | |

The law requires all Americans to obtain health insurance coverage or be subject to a penalty. An Advance Premium Tax Credit (APTC) is available to offset some of the cost of buying plans through the online marketplaces the law established, but there has been widespread confusion regarding the nature of this credit. At the time of initial purchase of health insurance through a state or federal exchange, consumers must estimate the amount of income they will earn through the rest of the year. This is used to determine the amount of federal subsidies they will receive via the APTC. Many tax filers are now learning that they misestimated.

In February, The Tax Institute at H&R Block released an analysis of PPACA’s impact so far. According to the Institute’s The Affordable Care Act: 2014 Tax Filing Impacts, through the first six weeks of the 2015 filing season, over 52 percent of taxpayers who bought insurance through a state or federal health insurance exchange underestimated their income and had to pay back a portion of the APTC they received – $530 on average. [12] Given that the APTC is a special “refundable” credit, available to individuals regardless of their income tax liability, this repayment hits low-income filers. Mark Ciaramitaro, vice president of H&R Block health care and tax services, said “[t]he level of payback of the Advance Premium Tax Credit is significant in that it’s costing taxpayers a large percentage of their refund – a refund many of them count on to pay household expenses.”[13]

The same analysis showed that 1 out of every 3 Marketplace enrollees had the opposite experience, they overestimating their incomes and then discovered they qualify for additional APTC subsidies that averaged $365.

PPACA also mandates that each taxpayer must provide proof of purchase of health insurance when they file their taxes. And for those who did not obtain insurance (and did not qualify for one of at least three dozen possible exemptions from the requirement), H&R Block found that they paid an average penalty of $172, significantly higher than the $95 fee that had been widely reported and which many had anticipated.[14]

The Institute concluded:

“The survey … exposed widespread consumer confusion about the law. …. In addition, many taxpayers who enrolled in coverage through the health insurance Marketplace and received advance tax credit payments did not understand they had received government assistance. Virtually everyone surveyed was confused about the tax credit reconciliation process, and many taxpayers without minimum essential coverage didn’t understand penalty calculations, the exemption process or tax form filing requirements.”

C. The Long Arm of the IRS Reaches Overseas

Even people quite literally on the other side of the world are beginning to feel the effects of an overbearing, convoluted Tax Code here in the United States. The Foreign Account Tax Compliance Act (FATCA) has been a recent but already highly controversial contributor to that reality. Enacted in 2010, FATCA requires any U.S. citizen or person[a] to report and pay taxes on their financial accounts held outside of the United States, even if they reside abroad. The law also requires foreign institutions to report certain information concerning their U.S. clients to the IRS.

Ostensibly designed to increase compliance with U.S. tax law and crack down on tax evasion, FATCA requires an already over-burdened IRS to devote more time and energy overseas. The United States already requires all citizens, regardless of residency, to pay income taxes. And although foreign governments[15] opt in voluntarily to the FATCA regulations, the element of choice is nearly non-existent for most overseas institutions: those that don’t comply with the law’s reporting requirements must withhold a 30 percent tax from account holders.

For American citizens living abroad, FATCA represents more than an additional reporting requirement. It is driving many to reconsider their citizenship altogether, with some polls placing that number at nearly 73 percent of all expats.[16] And for the IRS, it is difficult to overstate the challenges that enforcing the law would entail. In fact, the agency essentially admitted that it was not ready to do so, issuing a notice in May 2014 that the 2014 and 2015 calendar years would be regarded as a “transition” period for administration and enforcement of FATCA, even though final regulations were issued in January 2013.[17]

While the law’s full implementation is in limbo, some analysts have been skeptical of its ability to generate enough revenue to cover its administrative and enforcement costs, for which there has been no complete estimate. The Joint Committee on Taxation estimated that FATCA’s provisions could raise $8.7 billion over ten years, or an average of $870 million per year. By comparison, accounting firm KPMG reported that 25 percent of the global banks it surveyed will budget at least $1 million USD, with many indicating they will require more than $100 million USD annually to comply.[18] The majority of firms surveyed indicated that they would not be able to do so on their own, as KPMG reported that “given the compliance workload involved and how much is at stake, the majority of organizations (57 percent) are using or planning to use a professional services firm(s) to assist with their FATCA implementation program, with another 29 percent considering doing so.”[19]

D. The U.S. Tax System Is Lagging Behind Others

It is also remarkable how complex the U.S. tax system is when compared to other developed countries. Every year, accounting and consulting firm PricewaterhouseCoopers (PwC) publishes a report entitled “Paying Taxes” which compares the tax burdens faced by a hypothetical business in countries around the world. The burden is measured in hours per year spent complying with the country’s tax filing procedures, the number of payments it must make to do so, the overall tax rate the business would face, and an “ease of payment” ranking that weights those metrics. NTU Foundation compared PwC’s last five editions of the report, from 2011 to 2015, and compared the average results for the U.S. and four other Organization for Economic Cooperation and Development (OECD) countries.[20]

On average, PwC’s studies have shown that the U.S. ranks worst among the five OECD countries compared in terms of the total time a business spends complying with the Tax Code and overall ease of payment ranking. It is tied for worst when it comes to number of payments required. The study is a sobering reminder of just how much more difficult it is for U.S. businesses to comply with the Tax Code than those in other large economically developed countries.

IV. Complexity Leaves Taxpayers In the Dark and at Risk

Not only are individuals and businesses filing tax returns subjected to the administrative burden of an overly complicated tax system, but so are the IRS agents and government officials tasked with enforcing it. Unfortunately for taxpayers, that too often means difficulty getting help when they need it, and a high risk of fraud, identity theft, or otherwise compromised personal information.

A. The Taxpayer Service Problem

Imagine dealing with 100 million phone calls, 10 million written letters, and 5 million in-person visits per year. This is the task of the IRS, according to the Taxpayer Advocate’s latest report to Congress, and the agency is simply incapable of keeping up with the workload thanks directly to tax complexity.[21]

Over 150 million business and individual income tax returns were filed in Fiscal Year 2014, and the complicated state of the tax system means that many of those filers who ask for help will not ever receive it. That has very real implications for taxpayers’ finances, as a slow-to-respond IRS means more preventable mistakes and therefore administrative backlogs; a greater demand for more readily available professional assistance; and more time spent trying to get in touch with the agency.

The problem has become so deplorable that the Taxpayer Advocate’s latest report named the declining quality of service the single “most serious problem” out of more than 20 others facing taxpayers.

One of the clearest ways to demonstrate how increasingly difficult it is to get in touch with the IRS is by examining the “level of service” the agency achieved via its toll-free telephone assistance lines. This is a measure of how many taxpayers were able to get through to an employee and receive help before either giving up or being disconnected.

| Table 5. IRS Telephone Level of Service | ||||

|---|---|---|---|---|

| Fiscal Year | Total Calls (millions) | Level of Service (percent) | Goal Level (percent) | Average Wait (minutes) |

| 2009 | 104.2 | 70 | 77 | 8.8 |

| 2010 | 104.2 | 74 | 71 | 10.8 |

| 2011 | 112.7 | 70.1 | 71 | 13 |

| 2012 | 131 | 67.6 | 61 | 16.7 |

| 2013 | 128.3 | 60.5 | 70 | 17.6 |

| 2014 | 99.1 | 64.4 | 61 | 19.6 |

| Source: Government Accountability Office. | ||||

Even as call volume has decreased to its lowest level in recent years, the percentage of taxpayers able to actually reach the IRS has steadily dropped to fewer than 2 out of every 3 callers. Even the IRS’s goal level of service has declined; put another way, the IRS effectively defined 2014 as a successful year since “only” 4 out of every 10 taxpayers who called the agency were unable to get through to an agent for assistance. For those who were lucky enough to reach a live employee, the average wait time to do so was just under 20 minutes. According to the Taxpayer Advocate, in 2015 the IRS projects that it will only be able to assist about 50 percent of callers, who will wait an average of 30 minutes for basic assistance.

The scenario is arguably even worse when measured in terms of written correspondence. Taxpayers who are found to have inconsistencies or incongruities on their returns are given an opportunity to explain or offer documentation of their reasoning; the IRS records these as “adjustments inventory,” and any that aren’t responded to within established timeframes are referred to as “overage.” Table 6 shows recent trends in IRS overage correspondence.

| Table 6. IRS Correspondence Overage | ||

|---|---|---|

| Fiscal Year | Open Adjustments Inventory | Overage (percentage) |

| 2005 | 445,595 | 2 |

| 2006 | 573,175 | 28 |

| 2007 | 480,292 | 22 |

| 2008 | 725,943 | 33 |

| 2009 | 694,137 | 29 |

| 2010 | 606,029 | 28 |

| 2011 | 920,768 | 47 |

| 2012 | 1,028,539 | 48 |

| 2013 | 1,103,509 | 53 |

| 2014 | 937,529 | 51 |

| Source: Internal Revenue Service. | ||

The numbers speak loudly and clearly: it is taking longer and longer for the IRS to respond to taxpayers facing problems with their returns in a timely manner. That means a vicious circle of longer administrative backlogs, delayed refunds and resolutions, and a larger workload for the IRS.

B. Online Tools Convenient, but Identity Theft Presents a Growing Threat

In light of frustrating in-person, written, and telephone interaction with the IRS, more taxpayers are turning to the resources on the IRS website to get help navigating the tax system. Online access has increased rapidly in recent years, as seen in the table below.

| Table 7. IRS Online Usage | |||

|---|---|---|---|

| Fiscal Year | IRS.gov Visits (millions) | Forms, Publications, Instructions Downloads (millions) | Interactive Tax Assistance Tools Completions (thousands) |

| 2009 | 296 | 192 | N/A* |

| 2010 | 305 | 220 | 42 |

| 2011 | 319 | 229 | 177 |

| 2012 | 373 | 362 | 455 |

| 2013 | 456 | 218 | 631 |

| 2014 | 437 | 118 | 944 |

| Source: GAO, Internal Revenue Service.[23] | |||

| Note: Program introduced in 2010. | |||

However, along with a complicated tax filing process and the massive amount of personal information submitted electronically to the IRS comes a severe security threat. Unfortunately, the IRS has been overwhelmed in its attempts simply to keep the current filing system running, let alone ensure that it is secure. The result is billions of dollars in fraudulent refunds each year and an inefficient resolution process that can drag on for months.

The GAO reported in January 2015 that according to IRS estimates, $30 billion in tax-related identity theft refund fraud was attempted in the 2013 filing year. The good news for taxpayers is that 81 percent of that total – about $24.2 billion – was detected, prevented, and recovered. However, that still means $5.8 billion in fraudulent refunds were issued, and when all is said and done the IRS has no way of knowing if more went undetected.[24]

Table 8 highlights the number of documented cases of identity theft the GAO was able to identify in a 2012 report. The number has grown alarmingly even in just the five years covered by the study, jumping from 48,000 in 2008 to almost 642,000 in 2012, an increase of over 1,244 percent.[25]

| Table 8. Identity Theft Cases Recognized by IRS | |

|---|---|

| Year | Cases |

| 2008 | 47,730 |

| 2009 | 165,524 |

| 2010 | 147,680 |

| 2011 | 242,142 |

| 2012 | 641,690 |

| Source: GAO, IRS. | |

The issue was front and center in last year’s Taxpayer Advocate report, in which the Advocate noted that the IRS takes an average of 312 days to resolve an identity theft case, even though cases referred to the Advocate directly can be straightened out in an average of 87 days. The Advocate noted:

“To its credit, the IRS has recognized identity theft as a major challenge and has devoted significant resources to addressing it. Yet the IRS still takes much too long to fully unwind the harm suffered by identity theft victims and issue refunds to the legitimate taxpayers. Moreover, the IRS has yet to implement an effective program for overseeing cases with multiple issues that require coordination among [20] different IRS units, and is allowing too many victims to fall between the cracks of IRS bureaucracy. Thus, victim assistance overall, as well as the IRS’s specialized but decentralized approach, continues to be inadequate.”[26]

NTU Foundation summarized more of the risks associated with Tax Code complexity in a September 2014 report, The Need for Tax Reform: Simplicity, Savings, and Security.[27]

V. Conclusion

Every tax season that passes in the United States without meaningful tax reform is one in which the entire system becomes closer to falling apart. Rising costs and risks associated with complexity have very real economic impacts that are felt by taxpayers on a daily basis. However, they are also felt by the millions of Americans – at home and abroad – who find themselves willing but unable to comply with the system and in turn are confronted with weeks, months, even years of financial and bureaucratic difficulties as a result. Congress must face and address the rising tide of Tax Code complexity not only for the country’s fiscal future, but also its citizens’ well-being.

About the Author

Michael Tasselmyer is a Policy Analyst for the National Taxpayers Union Foundation (NTUF), the research and education affiliate of the National Taxpayers Union (NTU).

Additional research and assistance was provided by NTUF President Pete Sepp. Special thanks to David Keating, Senior Counselor of the non-partisan National Taxpayers Union for his more than 15 years of work on the “Taxing Trend” project. The research brought to light through his efforts inspired many of the directions taken in this paper.

[a] The IRS considers a U.S. “person” to include citizens, as well as certain nonresident individuals and estates and trusts if substantial decision-making authority is exercised by a U.S. court. See https://www.irs.gov/Individuals/International-Taxpayers/Classification-of-Taxpayers-for-U.S.-Tax-Purposes.

[1] Office of the National Taxpayer Advocate, “2014 Annual Report to Congress.” Accessed March 23, 2015 at https://www.taxpayeradvocate.irs.gov/2014-Annual-Report/full-2014-annual-report-to-congress/.

[2] Office of the National Taxpayer Advocate, “2014 Annual Report to Congress.” Accessed March 23, 2015 at https://www.taxpayeradvocate.irs.gov/2014-Annual-Report/full-2014-annual-report-to-congress/.

[3] Bureau of Labor Statistics, “Employer Costs for Employee Compensation – December 2014.” Accessed March 24, 2015 at https://www.bls.gov/news.release/pdf/ecec.pdf.

[4] Office of the Federal Register, 79 FR 24498, https://federalregister.gov/a/2014-09819.

[5] Office of the National Taxpayer Advocate, “2012 Annual Report to Congress.” Accessed March 24, 2015 at https://www.taxpayeradvocate.irs.gov/2012-Annual-Report/downloads/Most-Serious-Problems-Tax-Code-Complexity.pdf.

[6] Henchman, Joe. “How Many Words Are in the Tax Code?” Tax Foundation. Accessed March 24, 2015 at https://taxfoundation.org/blog/how-many-words-are-tax-code.

[7] Office of Management and Budget, “Federal Collection of Information.” Accessed April 2, 2015 at https://www.whitehouse.gov/omb/inforeg_infocoll.

[8] Office of Management and Budget, “Information Collection Budget for Fiscal Year 2010.” Accessed 4/2/2015 at https://www.whitehouse.gov/sites/default/files/omb/inforeg/icb/2011_icb.pdf.

[9] Office of the National Taxpayer Advocate, “2014 Annual Report to Congress.” Accessed March 23, 2015 at https://www.taxpayeradvocate.irs.gov/2014-Annual-Report/full-2014-annual-report-to-congress/.

[10] IBISWorld, “Tax Preparation Services in the US: Market Research Report.” Accessed March 30, 2015 at https://www.ibisworld.com/industry/default.aspx?indid=1399.

[11] Internal Revenue Service, “Affordable Care Act Legal Guidance and Other Resources.” https://www.irs.gov/Affordable-Care-Act/Affordable-Care-Act-of-2010-News-Releases-Multimedia-and-Legal-Guidance.

[12] The Tax Institute at H&R Block, “The Affordable Care Act: 2014 Tax Filing Impacts.” Accessed March 30, 2015 at https://newsroom.hrblock.com/wp-content/uploads/2015/02/ACA-2014-tax-return-impactsFINAL.pdf.

[13] H&R Block, “H&R Block: Taxpayers Following ACA Rules, Refunds Take a Hit.” Accessed March 30 at https://newsroom.hrblock.com/hr-block-taxpayers-following-aca-rules-refunds-take-hit/.

[14] Ibid.

[15] United States Treasury, “Resource Center: FATCA – Archive.” Accessed 3/31/2015 at https://www.treasury.gov/resource-center/tax-policy/treaties/pages/fatca-archive.aspx.

[16] Harjani, Ansuya, “Bulk of Americans abroad want to give up citizenship,” CNBC. Accessed 3/31/2015 at https://www.cnbc.com/id/102122343.

[17] Internal Revenue Service, “Further Guidance on the Implementation of FATCA and Related Withholding Provisions.” Accessed 3/31/2015 at https://www.irs.gov/pub/irs-drop/n-14-33.pdf.

[18] KPMG, “Surveying the Market: Are You Ready for FATCA?” Accessed 4/7/2015 at https://www.kpmg.com/Global/en/IssuesAndInsights/ArticlesPublications/Pages/surveying-market-are-you-ready-for-fatca.aspx.

[19] Ibid.

[20] PricewaterhouseCoopers, “Paying Taxes.” Accessed 4/7/2015 at https://www.pwc.com/gx/en/paying-taxes/.

[21] Office of the National Taxpayer Advocate, “2014 Annual Report to Congress.” Accessed March 23, 2015 at https://www.taxpayeradvocate.irs.gov/2014-Annual-Report/full-2014-annual-report-to-congress/.

[22] Government Accountability Office, “2014 Performance Highlights the Need to Better Manage Taxpayer Service and Future Risks.” Accessed 3/31/2015 at https://www.gao.gov/assets/670/667563.pdf.

[23] Ibid.

[24] Government Accountability Office, “Enhanced Authentication Could Combat Refund Fraud, but IRS Lacks an Estimate of Costs, Benefits and Risks.” Accessed 3/31/2015 at https://www.gao.gov/assets/670/667965.pdf.

[25] Government Accountability Office, “Total Extent of Refund Fraud Using Stolen Identities is Unknown.” Accessed 3/31/2015 at https://www.gao.gov/assets/660/650365.pdf

[26] IRS National Taxpayer Advocate, 2013 Annual Report to Congress, “Most Serious Problems: Identity Theft Victim Assistance,” January 9, 2014, https://www.taxpayeradvocate.irs.gov/2013-Annual-Report/id-theft/.

[27] Tasselmyer, Michael. The Need for Tax Reform: Simplicity, Savings, and Security, National Taxpayers Union Foundation, https://www.ntu.org/foundation/detail/ntuf-policy-paper-174-need-for-tax-reform-simplicity-savings-and-security-9-22-2014.

Associated file: