Last Thursday, NTUF testified before the Vermont House Ways and Means Committee on a proposal to dramatically increase the top state income tax rate from 8.75% to 13.3% and introduce a Vermont version of the federal Net Investment Income Tax (NIIT), levied at a rate of 4%.

Altogether, NTUF warned, high-earner investment income would face a combined state-federal rate of 41.1% — higher than any other state in the nation. Additionally, the top individual income tax rate in Vermont would tie with California for the highest in the nation, though the income threshold for the top bracket in California would be nearly three times higher.

Vermont is not the only state in the region trending in this direction. Maine just passed a 2% surtax to the individual income tax rate in the state, effective for the 2026 tax year, raising the top rate to 9.15%. A few years back, Massachusetts abandoned its flat tax by creating a new 9% top income tax bracket.

Northeast States’ Income Tax Rates, 2026 Tax Year

State | Top Individual Income Tax Rate |

New York | 10.9%* |

New Jersey | 10.75%* |

Maine | 9.15% |

Vermont | 8.75% (Proposed: 13.3%) |

Connecticut | 6.99% |

Rhode Island | 5.99% |

Nationwide average (rest of the country) | ~4.4% |

Pennsylvania | 3.07%** |

New Hampshire | 0% |

*Excludes local income taxes levied in a few jurisdictions.

**Excludes local income taxes levied in most jurisdictions statewide.

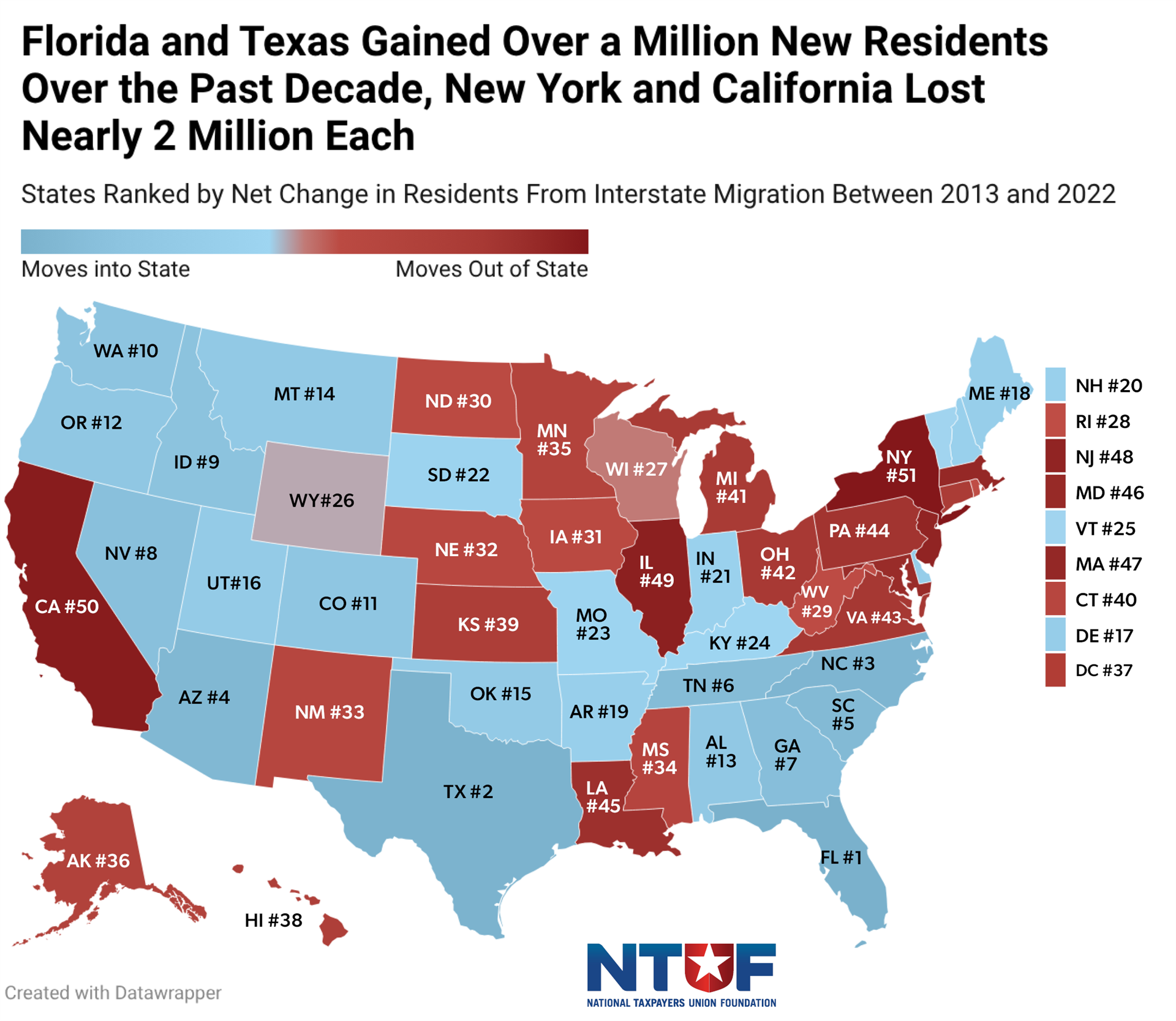

Of these states, only New Hampshire, Vermont, and Maine have experienced a net increase in population from interstate migration in the previous decade’s worth of IRS data (and Vermont essentially just breaks even). In total, the Northeast region has lost about 2.62 million residents and $25.4 billion in tax revenue to interstate migration in that period.

Should Vermont and Maine continue to head down this path, New Hampshire will owe them some very generous gift baskets.

One More Quick Note on Taxing High Earners…

. . . is that it’s a very unstable revenue source. Maine’s new tax rate will affect around 2,600 filers, while Vermont’s would apply to around 3,500. The widely-publicized ballot initiative aiming for a 5% wealth tax on California billionaires would apply to just around 200 taxpayers.

Those numbers won’t stay constant or even predictable, either. Not only are tax bases this small particularly sensitive to the outmigration that high-earner taxes lead to, they are also greatly affected by the booms and busts of the business cycle. Investment and pass-through business profits can spike in good years and plummet in lean ones.

States counting on taxing a small group of individuals to fund broadly-utilized services are committing the cardinal budgetary sin related to an incorrect ratio of eggs to baskets.