(pdf)

February 15, 2024

The Honorable Jason Smith, Chair

The Honorable Richard Neal, Ranking Minority Member

U.S. House Ways and Means Committee

1100 Longworth House Office Building

Washington, DC 20003

Dear Chairman Smith, Ranking Member Neal, and Members of the Committee,

On behalf of National Taxpayers Union Foundation (NTUF), I respectfully submit this statement for the record of the House and Ways and Means Committee’s Hearing with Commissioner of the Internal Revenue Service Daniel Werfel. NTUF has been a leader in developing responsible tax administration for nearly five decades. We always strive to offer practical, actionable recommendations about how our tax system should function. Our experts and advocates engage in in-depth research projects and informative, scholarly work pertaining to taxation:

- Our annual Tax Complexity report highlights the increasing time burden and out-of-pocket filing expenses imposed on taxpayers as they comply with the tax code each year. In 2022, Americans spent 6.553 billion hours worth $364 billion on the tax complexity burden, a 7 percent increase over the previous year.[1]

- Our annual Who Pays Income Taxes report shows the burden of the federal income tax.[2] In 2021, the top 1 percent by income ($682,577 and above) paid 46 percent of all income taxes, an all-time high (even above time periods when top income tax rate was 70 percent). 89 percent of income taxes were paid by the top 25 percent of filers; the bottom 50 percent by income (below $46,637) paid just 2 percent of all income taxes.

- NTUF has testified on multiple recent proposed Treasury and IRS rules, including Supervisory Approval of Penalties, IRS Dispute Resolution, and Gross Proceeds Reporting by Brokers and Determination of Amount Realized and Basis for Digital Transactions.[3]

Given our policy expertise, outreach know-how, and true non-partisanship, we seek to build lasting consensus for impactful reforms.

A Recent GAO Study Raises Questions About 2023 Tax Filing Season’s Successes.

“A normal tax season,” headlined the Washington Post in March 2023, citing that the IRS answered 90 percent of phone calls. “IRS answered 2.4 million more taxpayer calls due to new funding,” wrote Reuters in April 2023. “Influx of $80 billion has helped customer service” headlined the New York Times in August 2023, again citing reduced hold times.[4]

We welcome the Commissioner’s focus on customer service initiatives and the desire to see demonstrable improvements in metrics such as call wait times, late correspondence, and number of taxpayers helped to a resolution. However, victory should not be declared prematurely. A new study from the Government Accountability Office (GAO) provides data that gives alarming context to these claims.[5]

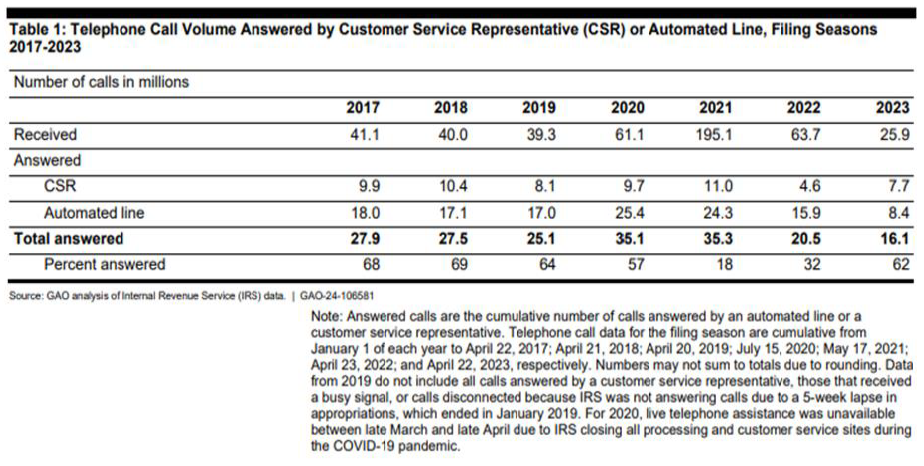

While the IRS did answer more phone calls in 2023 (7.7 million) vs. 2022 (4.6 million), the volume remained below all recent previous years (see chart below). Total taxpayer attempts to contact the IRS by phone plummeted, from 63.7 million to 25.9 million. The percentage of phone calls answered did rise, from 32 percent to 62 percent (not “90 percent”), but mainly because the denominator fell as taxpayers gave up trying:

The Commissioner should help the public understand why, despite the infusion of resources, various phone metrics are lower than the “starvation budget” level of 2017-2019:

- Calls received was 25.9 million in 2023, but 39.3 to 41.1 million in 2017-2019.

- Calls answered was 7.7 million in 2023, but 8.1 to 10.4 million in 2017-2019.

- Percent calls answered was 62 percent in 2023, but was 64 to 68 percent in 2017-2019.

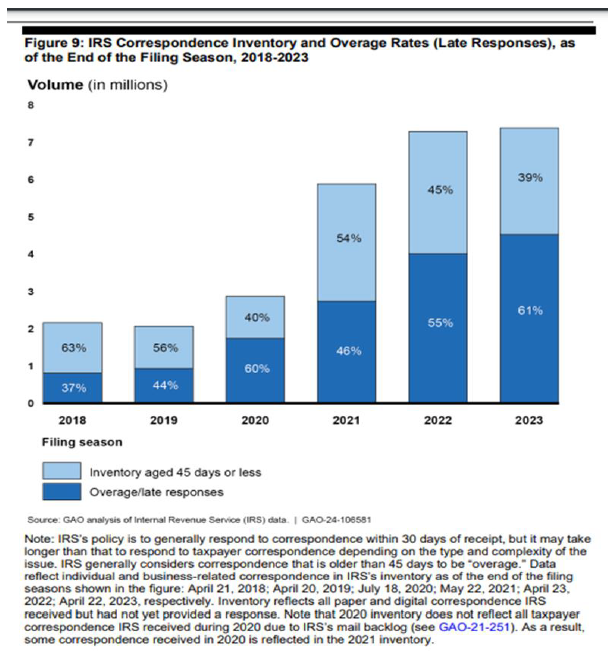

The GAO also found that the IRS correspondence backlog grew in 2023, with over 4 million late replies in 2022 rising to nearly 5 million in 2023. As the GAO notes, overall “correspondence inventories averaged 7.4 million compared to about 2 million in 2018 and 2019.” It should be noted that the IRS demands taxpayers respond to notices within 30 to 60 days, even while the Service takes over six months to do the same:

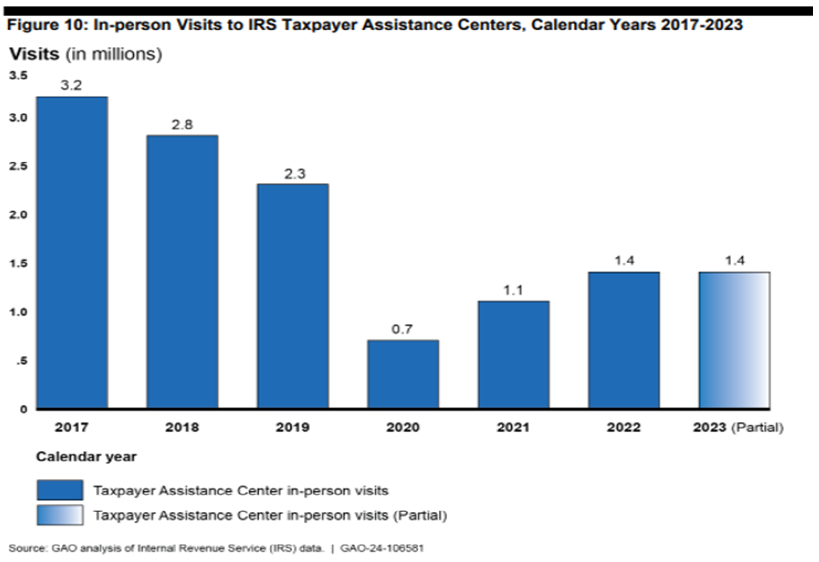

In-person visits to Taxpayer Assistance Centers (TACs), while rising, remain below pre-pandemic levels:

The Commissioner should explain the average and range time it takes the IRS to respond to taxpayer correspondence, and why correspondence backlog metrics worsened in 2023. The Commissioner should also explain IRS goals with taxpayer assistance centers and whether the goal is number of office locations, employees hired, or taxpayers helped.

The $600 1099-K Reporting Threshold is Unworkable and Should Be Modified, but the IRS Does Not Have Authority to Set it at $5,000.

In the past, third-party payment platforms were not required to generate a Form 1099-K until a taxpayer exceeded $20,000 in gross transactions and 200 transactions on the platform. The American Rescue Plan Act (ARPA) of 2021 changed that, setting the threshold at $600 in gross transactions and doing away entirely with the threshold for number of transactions. Under ARPA, this new threshold was set to go into effect in the beginning of 2022. In late December 2022, recognizing that this new threshold was unworkable and that taxpayers and third-party platforms (not to mention the IRS itself) were wholly unprepared to comply with this lower threshold, the IRS delayed its implementation by a year. That was the right move, and NTUF applauded the IRS at the time for its efforts to provide taxpayers with badly needed relief.[6]

There was, and remains, broad bipartisan support in Congress for raising the $600 threshold. Despite this fact, a legislative solution has failed to materialize. Throughout 2023, we noted that all the reasons that forced the IRS to delay ARPA’s threshold remained unresolved. In November 2023, the Government Accountability Office (GAO) confirmed NTUF's concerns, stating:

Many taxpayers will receive Form 1099-Ks who did not in the past, which may help some taxpayers comply. But, despite IRS communication efforts, it also may exacerbate confusion among some taxpayers, such as gig workers, who may not understand the taxability of their payments and taxes owed. For example, some of these taxpayers may not know how to calculate profit or loss and may not understand the information reported on the form. This puts them at risk of inaccurately reporting their incomes to the IRS or not meeting their tax obligations.[7]

In December 2023, the IRS again announced a one-year delay in implementation. This time, however, the IRS also announced a “phase-in” threshold of $5,000 for tax year 2024. By doing this, the IRS exceeded its authority to determine the most appropriate means of enforcing Congressional directives and effectively took it upon itself to rewrite the statute at issue. If the IRS recognized that the $600 threshold was not administrable, it only had one course available: a further delay. The idea that the IRS can unilaterally decide to make up a different threshold for Form 1099-K filing obligations from anything Congress had ever enacted is legally unfounded and sets a dangerous precedent for the future.

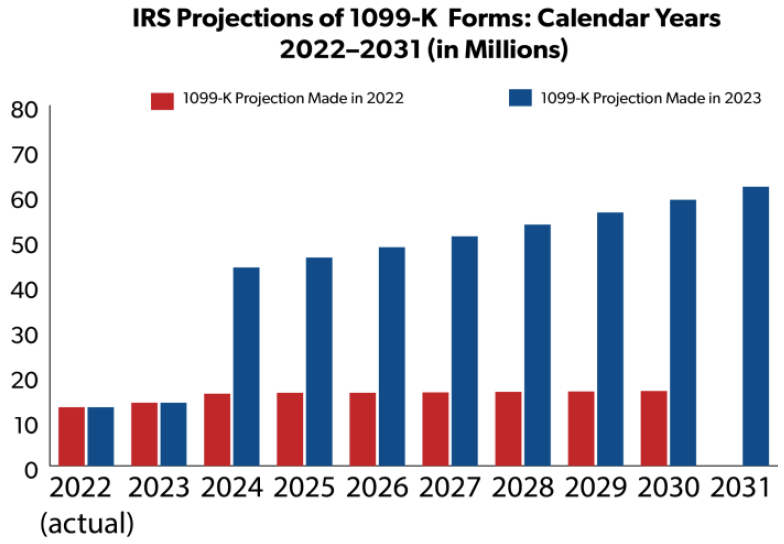

First, the IRS continues to underestimate the number of people who stand to receive a 1099-K. The IRS previously estimated that 16 million 1099-Ks would be distributed in 2024. NTUF warned that this estimate vastly undercounted the number of people who will be impacted.[8] In October 2023, the IRS dramatically revised its projection to 44 million 1099-K Forms in 2024 — three times higher than the amount it reported it received in 2023.[9] A more accurate estimate earlier along in the process may have catalyzed more urgent action by Congress, and it raises the question of why the IRS did not update this figure far sooner. The day after the filing deadline in 2023, IRS Commissioner Daniel Werfel told the Senate Finance Committee that ARPA’s 1099-K threshold was paused because the agency was “not ready to administer in a way that provides taxpayers the clarity they need.” Later in that hearing he also said that the IRS would have a much easier time administering the threshold if it was changed. Additionally, news coverage throughout 2023 highlighted the persistent confusion of a person’s tax obligations for the transactions reported in the 1099-K.

Second, the Commissioner should provide a missing key metric: an estimate of the compliance burdens with the lower threshold. The compliance burden cost of a $600 threshold is likely considerable. The lower threshold will drastically increase paperwork burdens on people to track the nature of all transactions conducted on third party platforms. Many will also spend out-of-pocket for tax advice.

Under the federal Paperwork Reduction Act, federal agencies are supposed to calculate the time and out-of-pocket expense burden of all forms that the public is required to fill out. This information is published in a database managed by the Office of Information and Regulatory Affairs (OIRA). The currently available calculation for the 1099-K is out of date. The Supporting Statement the IRS published in January 2023 shows an estimate of only 10.4 million forms.[10]

Third, it is likely that the IRS acted unlawfully when it expanded the de minimis threshold. While the IRS may delay implementation of such a threshold, it may not legislate new terms. The IRS’s acts in this case exceed their authority and violate clear legal standards. Under current Supreme Court precedent, courts first examine whether “Congress has directly spoken to the precise question at issue.”[11] “If the intent of Congress is clear, that is the end of the matter[,]” and the agency “must give effect to the unambiguously expressed intent of Congress”[12] because “Congress knows to speak in plain terms when it wishes to circumscribe, and in capacious terms when it wishes to enlarge, agency discretion.”[13] Here, the statute clearly states the minimum threshold to be $600. It is possible that the IRS may claim that Congress did not explicitly prohibit the IRS from setting a higher de minimis threshold, but the Supreme Court is currently considering this very issue – agency authority in an area of alleged statutory silence – in Loper Bright Enters v. Raimondo this year. The IRS is on safer legal ground by simply delaying imposition of the $600 threshold rather than creating a new threshold, however more desirable it may be than $600.

The IRS Needs to Fully Comply with the Paperwork Reduction Act.

The Paperwork Reduction Act mandates that the IRS and other government bodies assess the time and financial expenses individuals will bear while completing their forms. These forms are categorized into “information collections” and can be reviewed on the Office of Information and Regulatory Affairs (OIRA) website.

In our most recent analysis of complexity in the tax code, NTUF discovered the IRS struggles to evaluate cost burdens for all its forms, with just 18 out of 465 forms including an out-of-pocket cost estimates.[14]

For example, OIRA’s dashboard shows Form 1099-B, widely considered by tax preparers as the worst tax form, as having no out-of-pocket cost. The IRS estimates that the form imposes 674 million burden hours, the third highest time burden across the Internal Revenue Code., but a deep dive into the Supporting Document associated with the form notes, “To ensure more accuracy and consistency across its information collections, IRS is currently in the process of revising the methodology it uses to estimate burden and costs. Once this methodology is complete, the IRS will update this information collection to reflect a more precise estimate of burden and costs.”[15] This same stock language is used in the Supporting Statements for many other IRS forms.

First, the IRS should disaggregate burden into lines or instructions of that form which have required the most taxpayer time and effort. The Service could then issue guidance, in the form of a safe harbor, revenue procedure, or new instruction, designed to target and improve the comprehensibility of those lines or instructions. Then, controlling for other factors such as changes in economic circumstances of the filing population, or the tax laws themselves, the net effect of the guidance on reducing the taxpayer time and effort could be reasonably, if not perfectly, estimated.

Second, the IRS should distinguish information collections that have no actual cost from those where the cost is indeterminate. For example, in the Supporting Statement for the W-2 information collection, the IRS writes, “There were no estimates of capital or start-up costs and costs of operation, maintenance, and purchase of services provided to respondents.” This statement does not explain whether the forms impose no out-of-pocket expense or whether the IRS has not completed a calculation. The information on OIRA’s paperwork burden database should specify that a cost is indeterminate instead of listing it as $0.

The IRS Should Stop Attempting to Weaken the Requirement that IRS Supervisors Approve Penalties on Taxpayers.

The IRS has engaged in regulatory and litigation efforts to disregard 26 U.S.C. § 6751(b), which requires the IRS to obtain a supervisor’s approval before issuing a penalty on a taxpayer.[16] The IRS frequently does not comply with the statute’s requirement, and the solution to this is not to water down the provision or backdate supervisor approvals during litigation, but to follow the law.

Section 6751(b) was enacted, in part, to be a first line of defense against maladministration, before penalties become a problem of contention between the taxpayer and the government.”[17] As NTU President Pete Sepp said at a recent IRS hearing, one side benefit of such a requirement is for the IRS: by going through the procedure, the Service’s paper trail would be less susceptible to legal challenge in individual penalty cases, and so they would save potential litigation costs down the road.

But the IRS recently proposed regulations that would significantly undermine the supervisory approval requirement.[18] For example, the proposed regulation would lengthen the timeframe for the IRS to obtain a supervisor’s approval so long as it is any time before formal assessment—which is after the IRS has already communicated the proposed penalty to the taxpayer. Within the proposed regulation, the IRS steadily goes through the steps of communication with a taxpayer and concludes that a supervisor’s pre-approval for a penalty is not required for any of them (information request, pre-assessment notice, settlement discussion, even a Tax Court petition filing) except final, formal assessment.[19] An IRS agent would therefore be able to threaten penalties on a taxpayer, wait to see if they engage tax professionals and attempt to decrease the penalty or simply pay it, and only after that point obtain a supervisor’s approval, and it would all be a valid “approval.” This cannot be what Congress meant.

Evidence that the IRS already improperly sidesteps this requirement emerged recently in Lakepoint Land II, LLC v. Comm’r, where documents showed (and the government attorneys acknowledged) that the IRS had backdated a supervisor’s approval for penalties against Lakepoint, and then attempted to hide this fact from the Court in litigation.[20] Although the taxpayer in that case was able to uncover this during litigation, it is unlikely given the IRS’s animus toward the provision that this was an isolated incident. Other taxpayers may have difficulty proving the IRS’s noncompliance with section 6751(b).[21]

In 2021, the Joint Committee on Taxation calculated the revenue effect of watering down the supervisor approval requirement would be +$1.4 billion over ten years, showing that IRS agents’ failure to get supervisory approval is hardly a small problem. The Commissioner should commit to ceasing IRS regulatory and litigation efforts to evade the requirement that supervisors approve all penalties before they are communicated to the taxpayer.

The IRS’s Legal Strategy Should Be Reassessed in Light of Continuing Losses in the Courts and the Disregard It Shows to Taxpayers.

The IRS has recently suffered two 9-0 losses in the U.S. Supreme Court, and a string of losses in Tax Court, raising serious questions about their legal strategy and litigation posture. The Commissioner and the incoming IRS Chief Counsel should take these reversals as an opportunity to consider redirecting the IRS’s legal resources towards intentional evasion, and away from “gotcha” claims against taxpayers who have made honest mistakes navigating a confusing tax code. The Commissioner should also pledge to follow the Administrative Procedure Act (APA) for all binding guidance on taxpayers.

The Supreme Court rejected an IRS attempt to insulate its activities completely from taxpayer challenge in CIC Services v. IRS, in a unanimous opinion authored by Justice Kagan in May 2021. The case involved a notice issued by the IRS in November 2016 that any taxpayer engaging in certain micro-captive transactions (or their tax advisor) must comply with extensive and expensive reporting and record-keeping requirements or face $100,000 in fines and one year imprisonment. CIC Services LLC challenged the requirements, pointing out that the agency issued them without advance notice or accepting public comments as required by the Administrative Procedure Act.[22] The IRS took the surprising position that the federal Anti-Injunction Act (AIA) prohibits taxpayers from challenging any IRS guidance that might conceivably impact revenue collection. The Court rejected this position, explaining that only lawsuits to stop tax collection itself fall under the AIA. As we wrote about the case: “It is no accident that the IRS set up a situation where they claimed their one-sided and burdensome regulation was both exempt from the Administrative Procedure Act and also unable to be challenged because of the Anti-Injunction Act. The IRS strongly resists efforts to subject its sweeping powers to even basic protections and safeguards.”

The IRS also lost their attempt to win by default when a taxpayer misses a deadline, in Boechler v. Commissioner in another unanimous opinion, authored by Justice Barrett in April 2022. The IRS argued that a taxpayer who was one day late submitting their appeal to the U.S. Tax Court had forfeited their case and could not appeal. This position was especially tone-deaf, coming at a time when the IRS was a year behind in opening mail and months behind in responding to taxpayer replies to information demands. The Court held that the statute, 26 U.S.C. § 6330(d)(1), could be read multiple ways but that denying jurisdiction to appeal should only occur if the statute clearly states so.

The IRS has also lost a string of cases in Tax Court (notably, Hewitt v. Commissioner, and Green Valley Investors, LLC v. Commissioner) relating to conservation easement deductions, because the IRS is litigating essentially 100 percent of cases but focusing on esoteric deed language (and denying its shifting regulatory posture) rather than valuation disputes. In its annual report, the Tax Court noted that its docket has been crowded with hundreds of conservation easement cases, and anecdotally we have heard that judges are nudging the IRS to be less inflexible in their position in these cases.[23] The IRS responded to these losses by adding 200 lawyers to litigate the same unproductive strategy in more cases.[24] In another case, the IRS has allegedly hired an appraisal expert to give a zero valuation but where that same expert was used by the plaintiffs, creating a clear conflict of interest and tainting the evidence the IRS was seeking to introduce.[25] Whatever one may think of the policy of conservation easement deductions, Congress has placed them in the tax code and therefore the IRS’s policy to litigate 100 percent of partnerships who take the deduction is inappropriate and overbroad.

Most taxpayers want to comply with the law. IRS legal positions, however, seem primarily motivated by the perspective that all taxpayers are suspect and thus deserve the full weight of enforcement authority used against them as a first resort, is unfortunate. Where law-abiding taxpayers who try to do the right thing are treated as wrongdoers by the IRS, this has negative attendant effects on compliance and respect for the law. These IRS abuses, while seemingly technical in nature, have real impacts. Given the chilly reception this approach has received in the U.S. Supreme Court and the Tax Court, and the considerable resources (IRS, judicial, and taxpayer) being wasted, the Commissioner and the incoming Chief Counsel should reassess the direction of their legal strategy.

The IRS Should Work to Improve the Free File Program Instead of Spending Funding on a Duplicative Program

The IRS recently announced that it is phasing in a pilot version of a direct tax filing program. As of January, only filers who resided in Arizona, California, Florida, Massachusetts, Nevada, New Hampshire, New York, South Dakota, Tennessee, Texas, Washington, and Wyoming during 2023 are able to file through the pilot. There are also limitations on sources of income and allowable credits and deductions.

This represents a concerning initial foray into that space by the IRS. Thanks to its length and complexity, many aspects of the tax code remain open to interpretation, especially by an IRS prone to land on the most narrow and restrictive interpretations possible. Private tax preparation services have an incentive to find all the deductions and credits a taxpayer could reasonably claim. The IRS has no such incentive — in fact, every signal it has received from Congress as of late has pointed it in the exact opposite direction. To properly verify the figures the IRS input into the form, filers would still need to keep track of all the necessary paperwork and be familiar with the forms and schedules. State leaders both inside and outside the Direct File pilot have expressed similar concerns.[26]

Under the Inflation Reduction Act (IRA), the IRS received $15 million to study how a direct filing program might work and the costs involved. An expanded direct filing program could have a significant administrative cost. Converting to a new ready return system would also impose significant compliance burdens on employers, financial institutions, and even governmental agencies that administer benefit payments. Any business or organization that writes a check to employees or beneficiaries would have to report that information to the IRS on a new time table so that the agency has time to reconcile all the data and turn around the forms to filers for review. Estimates of the third-party costs, ranging from $500 million to $5 billion, would outweigh the potential savings for the government and taxpayers. It is also debatable whether the IRS is up to the challenge of gathering, securing, and reporting the financial data necessary to complete the forms. The IRS has already been struggling to maintain and upgrade its existing technology and respond to taxpayers’ correspondence in a timely manner.

No one should be deluded into believing that the IRS’s Direct File program would be a “free service” from the IRS. The costs, which could be significant, would ultimately fall on taxpayers.[27] Instead of building a new system from scratch, the IRS should improve upon the Free File system that it already established with private sector firms. More than 71 million returns have been filed through Free File since it was started in 2003, saving eligible taxpayers time, and reducing administrative costs to the IRS.

The Commissioner (and the Committee) Should Consider Insights and Guidance from the Taxpayers FIRST Project.

NTU Foundation has launched a cross-ideological coalition, Taxpayers For IRS Transformation (Taxpayers FIRST), to provide constructive advice to the IRS as it spends the infusion of funding it received from Congress in the Inflation Reduction Act. Taxpayers FIRST convenes an expert group of non-governmental stakeholders with a diverse set of backgrounds and perspectives to assist officials and policymakers so that the new funding is spent effectively, improves taxpayer services, upgrades outdated technology, and helps efficiently reduce the tax gap while respecting and strengthening taxpayer rights and due process.

Over the coming year, Taxpayers FIRST will discuss and develop policy recommendations in collaboration with this expert group, produce papers to communicate these recommendations with policymakers at the IRS and in Congress, and share a vision for improved services and technology with taxpayers across the country.

Focus areas include:

- Modernization of the IRS. Outdated equipment and processes are longstanding problems at the IRS and ones that are often used as justification for funding increases. We will advocate for what it will take to achieve digitization of tax filing and processing of tax returns.

- Measuring and assessing the tax gap. Government estimates of unpaid taxes are often used to justify harsher enforcement practices. We will look at which estimates are most accurate and correct in determining the sources of the gap. We will also assess the root causes for taxpayer errors during filing.

- Improvements to customer service. The S in IRS stands for service, and improving customer service has long been a work in progress. Expanding funding and expediting deployment of long-promised taxpayer services, such as improved digital communications tools, the “Where’s My Refund” online tool, and online accounts would go a long way in improving how taxpayers interact with the IRS and ensuring citizens are paying what is required from them.

- Enhancing taxpayer rights and privacy. A more powerful IRS should be accompanied by stronger protections for taxpayers and their private information. We will look at expanding access to Tax Court, creating a firewall between the Independent Office of Appeals and IRS agents, requiring the IRS to comply with legally mandated notice-and-comment procedures, and making greater use of alternative dispute resolution procedures.

We welcome the opportunity to engage with the Commissioner, the Committee, and other stakeholders in sharing these insights in the near future.

Conclusion

We appreciate the opportunity to provide these views to the Committee. Should you have any questions on our comments or on other matters before you, NTUF is at your service. Thank you for your consideration.

Sincerely,

Joe Bishop-Henchman

Executive Vice President

National Taxpayers Union Foundation

jbh@ntu.org

[1] Demian Brady, “Complexity 2023: 6.5 Billion Hours, $260 Billion: What Tax Complexity Costs Americans,” National Taxpayers Union Foundation, https://tinyurl.com/yyaxskem.

[2] Demian Brady, “Who Pays Income Taxes: Tax year 2021,” National Taxpayers Union Foundation, https://tinyurl.com/47zp98mz.

[3] Pete Sepp, “NTU Comments on IRS Proposed Rule for Supervisory Approval of Penalties,” National Taxpayers Union, Jul. 11, 2023, https://tinyurl.com/3phhkud9; Lindsey Carpenter, et al., “Comments on IRS’s Dispute Resolution Program,” National Taxpayers Union Foundation, Aug. 28, 2023, https://tinyurl.com/3nrmrsf7;

Lindsey Carpenter, “NTUF’s Comments on IRS Cryptocurrency Regulations,” National Taxpayers Union Foundation, Nov. 14, 2023, https://tinyurl.com/4u7t7k6n.

[4] See Jacob Bobage, “The IRS braces for the unthinkable: A normal tax season,” Washington Post, Mar. 3, 2023; Reuters, “US IRS answered 2.4 million more taxpayer calls due to new funding,” Apr. 17, 2023; Alan Rappeport, “$80 Billion Influx Has Helped Customer Service, I.R.S. Says,” New York Times, Aug. 16, 2023.

[5] Government Accountability Office, “2023 Tax Filing: IRS Improved Customer Service, but Could Further Improve Processing and Evaluate Expedited Hiring,” Jan. 2024, https://www.gao.gov/products/gao-24-106581. The following charts appear on pages 25, 31, and 34 of the GAO report.

[6] Andrew Wilford, “IRS Delays Lower Form 1099-K Threshold By One Year,” National Taxpayers Union Foundation, Dec. 23, 2022, https://tinyurl.com/3ar5ycm6.

[7] Government Accountability Office, “TAX ENFORCEMENT: IRS Can Improve Use of Information Returns to Enhance Compliance,” GAO-24-107095, Nov. 2023, https://www.gao.gov/products/gao-24-107095.

[8] Demian Brady, “Taxpayers Aren’t Ready for the Coming 1099-K Deluge - And the IRS May Not Be Either,” National Taxpayers Union Foundation, Jul. 12, 2023, https://tinyurl.com/yc6cvu3c.

[9] Demian Brady, “New IRS Data Still Vastly Underestimates the Increasing 1099-K Burden on Taxpayers,” National Taxpayers Union Foundation, Oct. 3, 2023, https://tinyurl.com/2nsc4vu3.

[10] Office of Information and Regulatory Affairs, ICR Documents, Jan. 17, 2023, https://www.reginfo.gov/public/do/PRAViewDocument?ref_nbr=202301-1545-003.

[11] Chevron, U.S.A., Inc. v. NRDC, Inc., 467 U.S. 837, 842 (1984).

[12] Id. at 842-43 (1984); see also Mendez-Garcia v. Lynch, 840 F.3d 655, 663 (9th Cir. 2016) (“If Congress has directly spoken to the precise question at issue, we must give effect to the unambiguously expressed intent of Congress.” (quotation omitted)); cf. City of Arlington v. FCC, 569 U.S. 290, 297 (2013) (explaining an agency’s “power to act and how they are to act are authoritatively prescribed by Congress” (cleaned up)).

[13] City of Arlington v. FCC, 569 U.S. 290, 297 (2013).

[14] Demian Brady, “Complexity 2023: 6.5 Billion Hours, $260 Billion: What Tax Complexity Costs Americans,” National Taxpayers Union Foundation, Apr. 2023, https://tinyurl.com/yyaxskem.

[15] Internal Revenue Service, “Supporting Statement: (Form 1099-B) Proceeds From Broker and Barter Exchange Transactions OMB 1545-0715,” Nov. 16, 2020, https://www.reginfo.gov/public/do/PRAViewDocument?ref_nbr=202007-1545-008.

[16] 26 U.S.C. § 6751(b)(1) (“No penalty . . . shall be assessed unless the initial determination of such assessment is personally approved (in writing) by the immediate supervisor of the individual making such determination or such higher level officiate as the Secretary may designate.”), enacted by Internal Revenue Service Restructuring and Reform Act of 1998, H.R. 2676 (1997-98).

[17] See “National Taxpayers Union Comments and Request for Public Hearing on Proposed Rule for Supervisory Approval of Penalties,” REG-121709-19, Jul. 11, 2023, p. 2, https://www.regulations.gov/comment/IRS-2023-0016-0007.

[18] Proposed Rule for Supervisory Approval of Penalties, 88 Fed. Reg. 21564 (Apr. 11, 2023).

[19] “A proposal of a penalty . . . to a taxpayer does not include mere requests for information relating to a possible penalty or inquiries of whether a taxpayer wants to participate in a general settlement initiative . . . .” 88 Fed. Reg. 21564, 21570; “The requirements of section 6751(b)(1) and paragraph (a)(1) of this section are satisfied for a penalty that is not subject to pre-assessment review in the Tax Court if the immediate supervisor of the individual who first proposed the penalty personally approves the penalty in writing before the penalty is assessed.” Id.; “The requirements of section 6751(b)(1) and paragraph (a)(1) of this section are satisfied for a penalty that is included in a pre-assessment notice that provides a basis for Tax Court jurisdiction upon timely petition if the immediate supervisor of the individual who first proposed the penalty personally approves the penalty in writing on or before the date the notice is mailed.” Id. at 21571; “The requirements of section 6751(b)(1) and paragraph (a)(1) of this section are satisfied for a penalty that the Commissioner raises in the Tax Court after a petition . . . if the immediate supervisor of the individual who first proposed the penalty personally approves the penalty in writing no later than the date on which the Commissioner requests that the court determine the penalty. Id.; “[B]y allowing a supervisor to approve the initial determination of a penalty up until the time the IRS issues a pre-assessment notice subject to review by the Tax Court . . . the supervisor has the opportunity to consider a taxpayer’s defense against a penalty, if applicable, and decide whether to approve the penalty.” Id. at 21567.

[20] Lakepoint Land II, LLC v. Comm’r, T.C. No. 13925-17, T.C. Memo. 2023-111, at *2-3, 10-11 (Aug. 29, 2023) (Memorandum).

[21] See, e.g., Tyler Martinez, “IRS Accused of Backdating and Lying to the Tax Court,” National Taxpayers Union Foundation, Jun. 28, 2023, https://tinyurl.com/ywv6umrj.

[22] Treasury and the IRS have a long-standing view that it need not fully comply with the APA. See, e.g., CIC Services, LLC v. IRS, 925 F.3d 247, 258 (6th Cir. 2019) (“Defendants do not have a great history of complying with APA procedures, having claimed for several decades that their rules and regulations are exempt from those requirements.”); Cohen v. United States, 650 F.3d 717, 726 (D.C. Cir. 2011) (en banc) (“The IRS envisions a world in which no challenge to its actions is ever outside the closed loop of its taxing authority.”); Kristin E. Hickman & Gerald Kerska, Restoring the Lost Anti-Injunction Act, 103 Va. L. Rev. 1683, 1714 (2017) (“Even after the Supreme Court’s pronouncement in Mayo Foundation that both specific and general authority Treasury regulations carry the force of law, the government has continued to assert that many or even most Treasury regulations are exempt interpretative rules.”); Kristin E. Hickman, A Problem of Remedy: Responding to Treasury’s (Lack of) Compliance with Administrative Procedure Act Rulemaking Requirements, 76 Geo. Wash. L. Rev. 1153, 1214 (2008) (“Despite Treasury’s claims to the contrary, the evidence is strong that Treasury has an APA compliance problem.”). The 1986 regulation was a product of this defiance, with Treasury using two pages of the Federal Register “to address more than 700 pages of timely comments and more than 200 pages of public testimony.” Oakbrook Land Holdings, LLC v. Commissioner, 154 T.C. 180, 221 (2020) (Toro, J., concurring in the result).

[23] In 2019 and 2020, the National Taxpayer Advocate recommended that the IRS “avoid litigation by providing model language taxpayers could use in deeds conveying conservation easements.” National Taxpayer Advocate, Annual Report to Congress 2020 at 218, citing National Taxpayer Advocate, Annual Report to Congress 2019 at 203. The IRS declined to do so, citing “other workload priorities.” See Pete Sepp & Joe Bishop-Henchman, “IRS Sends Settlement Offer Scare Tactic on Conservation Easements,” National Taxpayers Union Foundation, Jul. 1, 2020, https://tinyurl.com/2jez8tf6. As the pandemic hit, the IRS did send settlement offers to those with pending conservation easement litigation, demanding that the deduction be disallowed in full, partnerships agree to pay full penalties and interest, and investor partners allowed to deduct costs but services partners allowed to deduct none. See id., citing IRS, IR-2020-130. Given the unfair terms, it is no surprise that “[i]t does not appear that many taxpayers have accepted the offer to date.” National Taxpayer Advocate, Annual Report to Congress 2020 at 217.

[24] See, e.g., Internal Revenue Service, “IRS Chief Counsel looking for 200 experienced attorneys to focus on abusive tax deals; job openings posted,” Jan. 21, 2022, https://tinyurl.com/y4mmvx6b; Theresa Schliep, “Tax Court Denies IRS Early Win In $15M Easement Fight,” Aug. 29, 2022, Law360, https://tinyurl.com/3z5f72th; Emlyn Cameron, “Tax Court Denies IRS Win on Easement Purpose Protection Issue,” Jul. 20, 2022, Law360, https://tinyurl.com/33xzhye7; Emlyn Cameron, “IRS Denied Win On Deed Validity In $26M Easement Case,” Law360, https://tinyurl.com/mvavc9ep; Guinevere Moore, “Courts Are Deciding Some Conservation Easement Cases In Favor of Taxpayers – At Least In Part. Is It Time To Rethink Settlement?,” Forbes, Dec. 17, 2020, https://tinyurl.com/3jtbz3md; Pete Sepp, “Shortsighted: How the IRS’s Campaign Against Conservation Easement Deductions Threatens Taxpayers and the Environment,” National Taxpayers Union, Nov. 29, 2018, https://tinyurl.com/22z2cewd.

[25] See Kristen A. Parillo, “Tax Court Easement Litigants Want To Impeach IRS Appraisal Expert,” 184 Tax Notes 367, Jan. 8, 2024.

[26] Letter from Montana Attorney General Austin Knudsen to U.S. Treasury Secretary Janet Yellen,, Jan. 30, 2024, p. 4, https://dojmt.gov/wp-content/uploads/IRS-Direct-File-Letter-Final.pdf.

[27] Robert A. Boisture, Albert G. Lauber, and Holly O. Paz, “Policy Analysis of 'Return-Free' Tax System,” Computer & Communications Industry Association, Apr. 2006, https://ccianet.org/wp-content/uploads/library/Return-Free-WP.pdf.