Recently, a number of non-partisan tax administration experts have called on lawmakers or the Internal Revenue Service (IRS) itself to reallocate some of the Inflation Reduction Act’s (IRA) nearly $46 billion in enforcement funding to the IRS’s taxpayer services and modernization activities instead. Such an effort, if successful, could more rapidly improve IRS customer service efforts and reduce the tax gap by enabling taxpayers to receive assistance and have their questions answered before making potential errors on their tax forms.

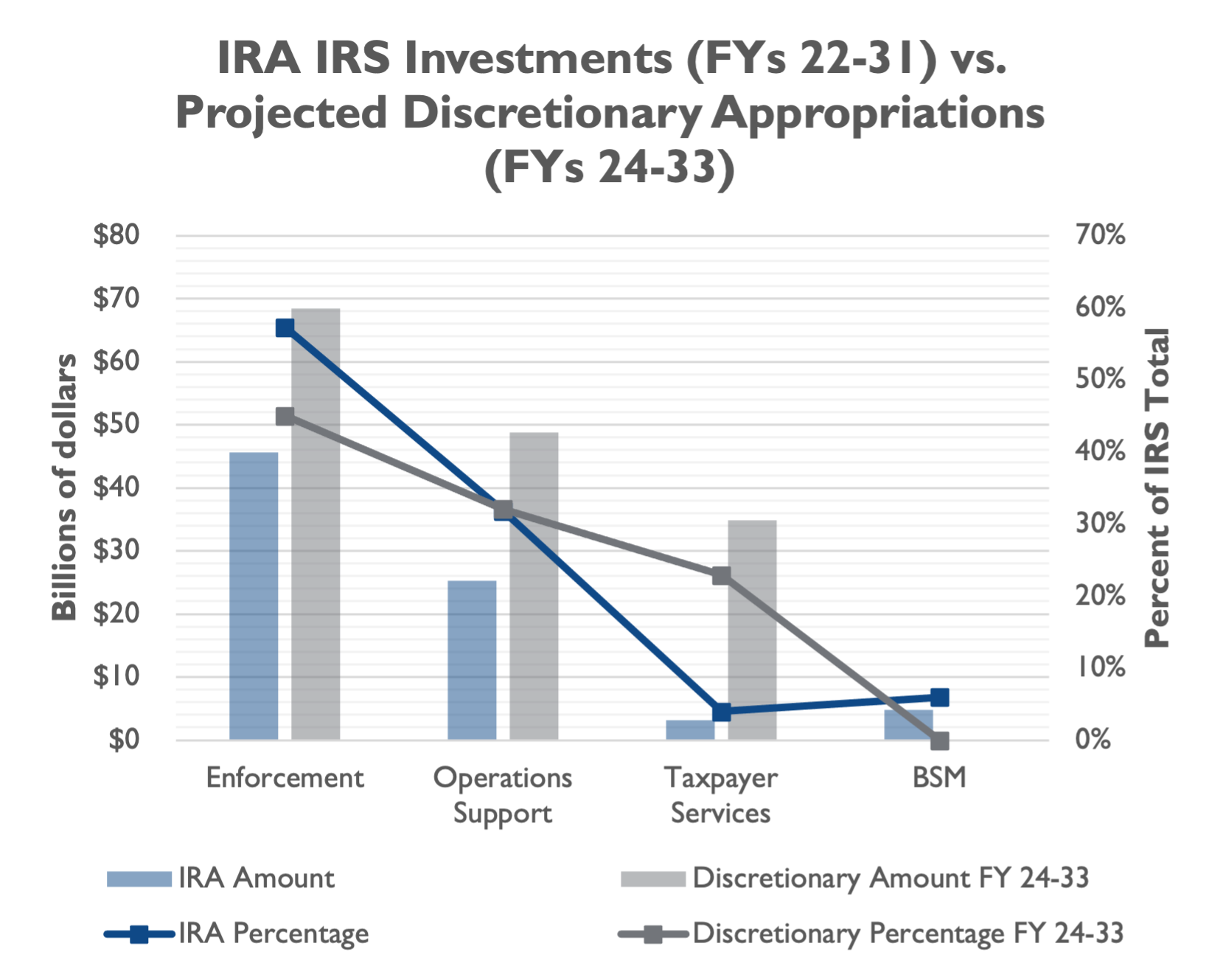

When Congressional Democrats appropriated $80 billion in 10-year funding for the IRS under the IRA in August 2022, many stakeholders – including NTU Foundation and its sister organization, NTU – pointed out that a disproportionate amount of the additional IRS funding in the law was dedicated to increased tax enforcement activities: nearly $46 billion, or more than 57 percent of the total additional funding.

This compares unfavorably to a typical year in the IRS’s discretionary budget, where around 45 percent of total funding is dedicated to enforcement activities. Only 10 percent of the IRA’s additional funding for the IRS went to business systems modernization ($4.8 billion, or six percent of the $80 billion) and customer service ($3.2 billion or four percent), whereas in a typical funding year for the IRS about 23 percent of total appropriations go to customer service.

Lawmakers skewed IRS investments in the IRA towards enforcement in part to offset increased spending and tax cuts included in the IRA. The Congressional Budget Office estimated that the $80 billion appropriation for the IRS – and particularly the increased enforcement activities that would result from the law – would increase federal revenues by $180 billion over 10 years, for net deficit reduction of around $100 billion. And an early version of the IRA, called the Build Back Better Act, focused nearly the entire $80 billion on enforcement activities alone.

Now that the IRA has been enacted into law – and as stakeholders still await the IRS’s plan for spending the $80 billion over the next decade – an increasing number of tax administration experts are asking Congress or even the IRS itself to consider reallocating some of the enforcement funding to taxpayer service and modernization efforts.

National Taxpayer Advocate (NTA) Erin Collins, a non-partisan expert respected by policymakers across the ideological spectrum who was appointed to lead be the nation’s third ever NTA in March 2020, recently called for shifting IRA funds away from enforcement and to taxpayer service:

“...the top tax administration priority now should be to improve taxpayer service, particularly after the struggles of the last few years, and to do that, the IRS needs more funding in the Taxpayer Services and [Business Systems Modernization] accounts.”

Collins also made a persuasive case for improving the IRS’s customer service efforts and pre-tax filing assistance, arguing that these are the “most efficient way[s] to improve compliance” and, in the process, narrow the gap between taxes owed and taxes paid:

“The most efficient way to improve compliance is by encouraging and helping taxpayers to do the right thing on the front end. That is much cheaper and more effective than trying to audit our way out of the tax gap one taxpayer at a time on the back end.”

We at NTUF could not agree more.

The American Institute of Certified Public Accountants (AICPA), a national group of tax practitioners, also recently recommended that the Treasury Department and IRS address “imbalance[s]” between the enforcement account and taxpayer services account:

“…given the historic low levels of IRS taxpayer services, we are concerned that there was an insufficient allocation of funding in the IRA to improve taxpayer services to appropriate levels. We are concerned that service challenges will persist unless sufficient, targeted funding for technology improvements, human talent and training, and taxpayer services are appropriated.”

AICPA even suggested that improving services within the IRS’s enforcement account could help taxpayers and tax practitioners comply with the law, through attracting and retaining a quality workforce, upgrading technology infrastructure, and improving enforcement customer service.

NTU made a similar suggestion in a recent communication to the IRS regarding its proposed rules for the Independent Office of Appeals, writing in November 2022 that:

“...additional funding for the Office would be an acceptable and welcome use of a portion of the $80 billion in funding Congress has appropriated to the agency for use over the next 10 years under the Inflation Reduction Act (IRA) of 2022. In fact, additional spending to expand appeals rights and independent review of tax controversies could ultimately save the agency money over the long run, by obviating more expensive and protracted litigation over tax controversies.”

And although the IRS has already spent $426 million from the IRA on improving customer service – more than 13 percent of the total allocated the IRS for customer service over the next 10 years – there are at least two data points bolstering the case for Congress to increase the proportion of IRA funding going to customer service:

- First is that the IRS has already burned through about one-seventh of its 10-year customer service funding in just the first six months of the IRA. While this high burn rate may be in part due to the need to scale up quickly on the customer service workforce, efforts to retain these workers and maintain a robust increased customer service presence may cause the IRS to burn through its entire customer service funding years before the 10-year window runs out.

- Second is that while the IRS has improved its service and access levels for taxpayers attempting to resolve an issue, the improvements may not be as dramatic as previously thought. Biden administration officials and some lawmakers have touted an improvement in “level of service” numbers from less than 20 percent last filing season to more than 80 percent this filing season, but as Senate Appropriations Ranking Member Susan Collins (R-ME) recently pointed out (link paywalled) more conservative “level of access” statistics indicate that “the number of calls being answered [is] closer to 52% through March 4 [2023], compared with 31.2% through March 5 a year earlier.” Former NTA Nina Olson, now Executive Director of the Center for Taxpayer Rights, argued that the “level of access” statistics paint a more accurate picture of IRS customer service success.

While a level of access improvement from 31 percent to 52 percent is certainly notable and worth applauding, the IRS can do a lot better. Those customer service metrics would likely not be acceptable at a consumer-facing Fortune 500 company, and they should not be acceptable for the part of the federal government more U.S. citizens interact with than any other.

So, if lawmakers or the Biden administration or the IRS agree that some enforcement funding in the IRA should be reallocated to customer service and modernization – and they should agree – how would policymakers do so?

NTA Collins points to four options: 1) stand-alone legislation from Congress, 2) adjustments in discretionary appropriations that account for the IRA’s imbalance, 3) enhanced transfer flexibility for the IRS, and 4) expansions to the scope of enforcement funding that enable enforcement accounts to fund new or additional activities.

As an advocate for Congress’ power over the nation’s purse strings, NTU generally believes that Congress should take the lead in redirecting already appropriated funds. Stand-alone legislation would be ideal, but may be unrealistic to expect in the politically charged and divided Congress.

Adjustments to discretionary appropriations may offer a more realistic legislative path forward, since lawmakers in both parties agree that Congress should pass discretionary appropriations for fiscal year (FY) 2024 as soon as practicable, and ideally before the October 1 start of FY 2024 (absent regular appropriations, Congress would need to pass a continuing resolution to keep vast swaths of the government open). House Republicans may be open to crafting legislation that corrects for the imbalance in the IRA by disproportionately funding customer service and modernization efforts in FY 2024 discretionary appropriations, but Senate Democrats may be more skeptical.

House Republicans, for their part, may be skeptical of either enhancing the IRS’s transfer flexibility or expanding the scope of enforcement funding, given the low levels of trust for the IRS in some pockets of the Republican Party right now.

In short, none of the four paths advocated for by Collins are easy, but NTUF stands ready to work with lawmakers who wish to craft bipartisan legislation increasing customer service funding available to the IRS. The IRS has made progress in this tax filing season, but a significant amount of work remains.