Introduction

Trillion-dollar deficits are a growing source of concern and debate in Congress. However, official accounting rules often essentially assume that borrowers will not default, obscuring the true cost of risky federal lending programs that expose taxpayers to substantial liabilities.

A new January 2026 report from the Congressional Budget Office (CBO) shows how large this distortion has become. Using an alternative fair-value accounting approach alongside the statutory method, CBO finds that the loans and guarantees the federal government is expected to issue this year contain more than $65 billion in additional subsidies that are not accounted for under current budget scoring rules.

As the federal debt will soon exceed the post-World War II high as a percentage of the U.S. economy, policymakers can no longer justify rules that obscure the true cost of deficit spending. To improve budget transparency, Representative Ralph Norman’s (R-SC) Fair-Value Accounting and Budget Act (H.R. 1388) would make fair-value accounting the official accounting method.

Background

In addition to discretionary spending through grants and direct spending through programs like Social Security and Medicaid, the government also issues direct loans and loan guarantees. These federal credit programs expose taxpayer dollars to risk when borrowers default on their loans or when guarantees are triggered, and taxpayers must assume the liability.

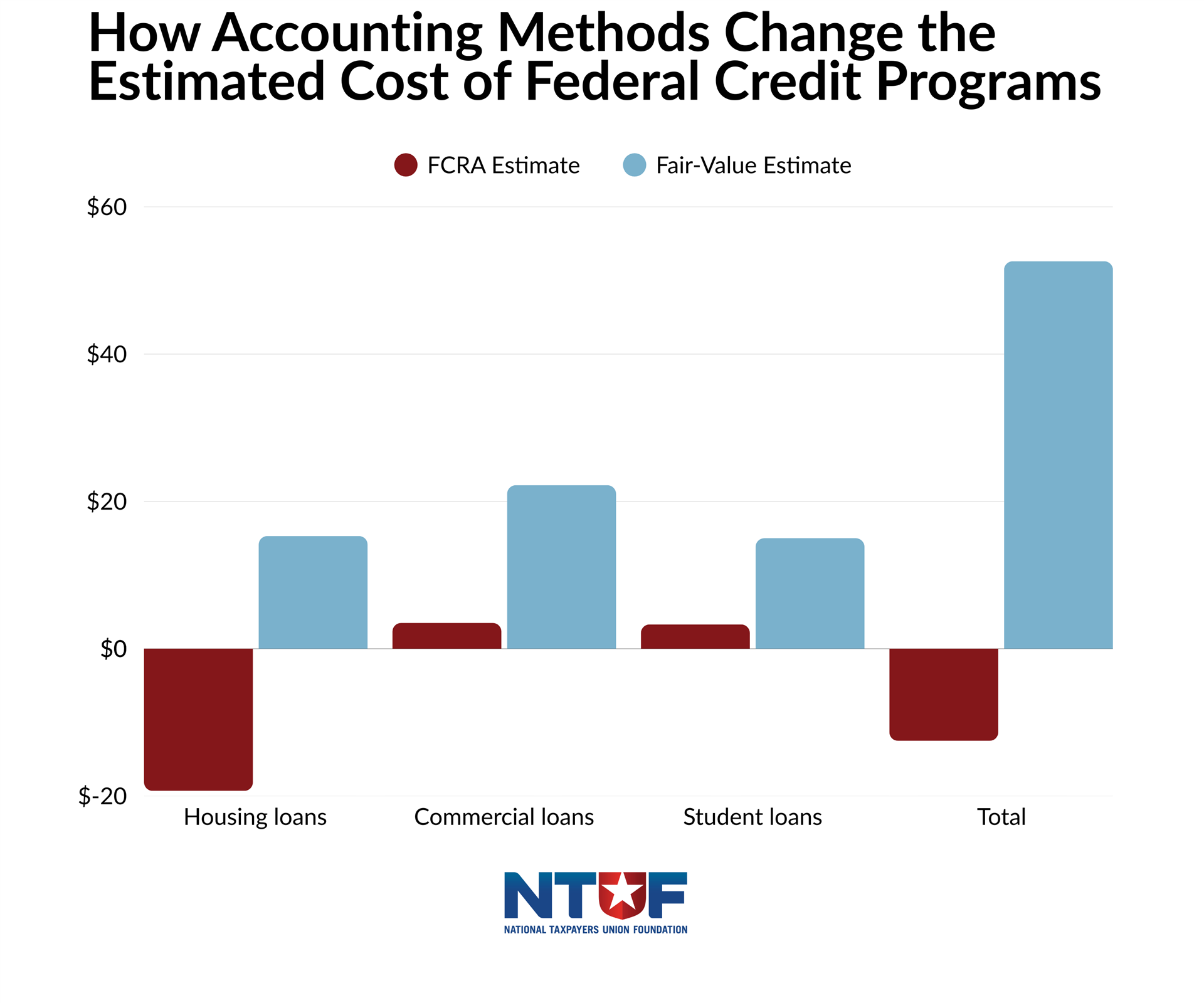

CBO expects roughly $1.9 trillion in new direct loans and loan guarantees this year. Under the accounting rules mandated by the Federal Credit Reform Act of 1990 (FCRA), those federal credit programs appear to reduce the deficit by $12.5 billion. However, using a fair-value approach that reflects market risk shows these new issuances would increase the deficit by $52.6 billion.

The gap stems from how each method measures cost. FCRA estimates the cost of federal credit by discounting future cash flows using Treasury rates, effectively treating risky loans and guarantees as if they were nearly risk-free. On the other hand, fair-value accounting uses the same cash flows but incorporates a market-based risk that private lenders use, adding a premium cost to the loan to account for the likelihood of defaults.

CBO has published side-by-side comparisons of these two approaches for years, and the pattern is consistent: once market risk is included, federal credit programs appear substantially more costly. Figure 1, below, illustrates the swing in costs under the two methodologies. The largest differences come from politically-sensitive programs that dominate the federal credit portfolio. Housing credit alone accounts for $34.7 billion of the difference, flipping from $19.3 billion in “savings” under FCRA to $15.3 billion in real costs under fair value. Commercial loans add another $18.7 billion, while student loans contribute $11.7 billion, rising from $3.3 billion to $15.0 billion once economic risk is properly counted.

Despite repeated warnings from budget analysts, the basic accounting framework has remained largely unchanged since 1990. Its persistence reflects more than technical inertia. By allowing policymakers to record federal lending as generating budgetary savings rather than costs, the current system makes it easier to expand popular credit programs without fully confronting their fiscal tradeoffs.

Trends in Federal Credit Programs

Table 1. Federal Credit Programs, Obligations, and Subsidy Costs in CBO’s Annual Reports

Year |

Number of Programs |

Obligations (Billions of 2023 Dollars) |

FCRA Subsidy Rate |

Fair-Value Subsidy Rate | FCRA Subsidy Cost (Billions of 2023 Dollars) | Fair-Value Subsidy Cost (Billions of 2023 Dollars) |

2018 | 78 | 2,022 | -3.1% | 2.2% | -62.9 | 44.2 |

2019 | 79 | 1,831 | -2.4% | 2.5% | -44.5 | 45.1 |

2020 | 85 | 1,692 | -2.2% | 2.5% | -36.6 | 43.1 |

2021 | 89 | 1,693 | -2.7% | 3% | -45.9 | 51.5 |

2022 | 112 | 2,255 | -1.9% | 2.7% | -41.6 | 60.4 |

2023 | 118 | 2,172 | -1.9% | 2.4% | -41.1 | 51.1 |

2024 | 131 | 1,553 | 0.7% | 4.9% | 10.9 | 76.7 |

2025 | 129 | ~1,900 | 0.1% | 3.5% | 2.4 | 65.2 |

2026 | 104 | 1743 | -0.7% | 2.8% | -11.5 | 48.4 |

Table 1 shows persistent divergence between how federal credit programs are recorded under FCRA and fair-value when market risk is incorporated. All figures are adjusted to 2023 dollars to allow for consistent comparison across years. Across most years, federal loans and guarantees often appear to generate savings or minimal costs under FCRA, while appearing as significant costs under fair-value estimates. This pattern holds even as the overall volume and scope of federal lending and loan guarantees have expanded across major sectors such as housing, student loans, and energy finance.

CBO’s latest report also provides additional context for the trends shown in Table 1 by highlighting the scale and composition of federal credit programs. In 2026, the agency identified 104 federal programs that provide credit assistance, of which 88 are discretionary programs funded through annual appropriations and 16 are mandatory programs and other commitments. Although discretionary programs make up the majority by number, mandatory programs account for most of the total dollar value of federal credit assistance.

CBO further finds that federal credit exposure is concentrated in a small number of large programs. Mortgage guarantee programs and federal student loan programs dominate overall credit activity. In particular, programs associated with Fannie Mae and Freddie Mac, along with student loan and VA mortgage guarantee programs, represent the largest sources of federal credit exposure and play a central role in shaping overall subsidy costs and fiscal risk.

Recent Reform Efforts

Congress has long been aware of this accounting discrepancy. Beginning in the early 2010s, lawmakers introduced multiple proposals to replace or supplement FCRA with fair-value accounting. Measures such as the Honest Budget Act in 2013 and the Budget and Accounting Transparency Act of 2014 were introduced across several Congresses. Some passed one chamber but ultimately stalled without enactment. Similar proposals have resurfaced repeatedly, reflecting ongoing concern about transparency in federal credit budgeting.

The most recent effort, Rep. Norman’s Fair-Value Accounting and Budget Act (H.R. 1388), would require the Congressional Budget Office to provide fair-value estimates for any legislation that establishes or modifies federal loan or loan-guarantee programs. The bill would build on CBO’s existing analytical work and give lawmakers a clearer picture of the taxpayer exposure embedded in federal credit programs.

“For far too long, our government has operated inefficiently, leading to poor lawmaking with hefty costs to the American taxpayer,” Norman said. “Every member of Congress should support greater transparency in government spending.”

Implementing this reform is increasingly crucial in light of the perilous $38 trillion federal debt and amid calls to expand the Export Import Bank of the United States (EXIM). President Trump recently announced a new Strategic Critical Minerals Reserve initiative backed by a $10 billion loan from the Bank. Better budget transparency is needed to account for the risk of the government’s expanded credit activity.

Conclusion: Accounting as Democratic Transparency

By understating the cost of federal credit programs, FCRA obscures the tradeoffs associated with some of the government’s largest and most popular subsidies. Fair-value accounting would not eliminate federal credit or resolve disagreements about its role, but it would make those tradeoffs more transparent.

Institutionalizing consistent fair-value reporting would strengthen fiscal transparency. Clearer accounting would ensure that future debates over federal lending for housing, education, and business are informed by a more complete understanding of the true cost to taxpayers.