(pdf)

I.Introduction

This is the first tax filing season including the reforms and reductions implemented through the Tax Cuts and Jobs Act (TCJA). This analysis, which has been continually conducted and updated for nearly two decades, will address the compliance burden taxpayers face this year, the impact on complexity from the enacted tax reform law. Thanks to the TCJA, 90 percent of middle-class families received a tax cut, and the overall cost of complying with the individual income tax code was smaller. Business taxes were also reduced from 35 percent to a more globally-competitive 21 percent rate. However, there were trade-offs in complexity with the addition of complicated new international provisions.

II. The Tax Code’s Compliance Burden

A. The Total Burden

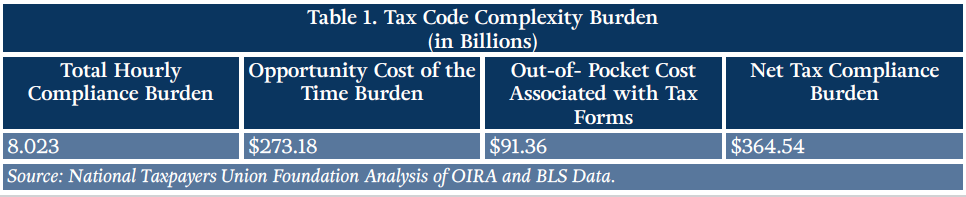

By April of each year, Americans become aware of how much they must pay in taxes, but the total burden and cost of our tax system reaches far beyond the net dollar amount owed to the Treasury. An immense amount of time is obligated each year to conforming with the tax laws. According to our analysis of data reported by the Office of Information and Regulatory Affairs (OIRA), altogether, complying with the Tax Code in 2018 consumed 8.02 billion hours for recordkeeping, learning about the law, filling out the required forms and schedules, and submitting information to the Internal Revenue Service (IRS).[1]

We can arrive at an estimate of the value of this time burden by framing it in terms of private sector labor costs. According to the Bureau of Labor Statistics (BLS), U.S. employers spent an average of $34.05 per hour worked on total non-federal civilian employee compensation in December 2018. (That figure includes benefits as well as wages and salaries).[2]

Thus, the billions of hours spent on taxes is equivalent to $273.2 billion in labor – a valuable opportunity cost that will instead be lost to Tax Code compliance. Add to that the $91.4 billion in estimated out-of-pocket costs taxpayers spent on software, professional preparation services, or other filing expenses, and the total economic value of the compliance burden imposed by the Tax Code can be calculated at $364.5 billion.

To put the compliance burden into perspective, it represents about 18 cents on every tax dollar projected to be collected through corporate and individual taxes this year. $365 billion is also:

- equivalent to 1.7 percent of current GDP;

- tops the amount of net interest payments on the federal debt last year ($325 billion); and

- exceeds the combined budgets of the Departments of Veterans Affairs and Agriculture ($355.93 billion).

Fortune publishes a yearly list of the Global 500, the largest companies in the world by revenue. Only one business on the list is worth more than the value of the compliance burden of the U.S. Tax Code: Walmart (with revenues of $500 billion).[3]The money lost to tax compliance is greater than the combined revenues of Apple and Google parent-company Alphabet, and is over twice as much as the revenues of Amazon. It outstrips the GDP of Israel, Ireland, and Denmark.[4]In other words, we flush down the drain of tax compliance not just entire companies-worth of productivity, but entire countries-worth as well.

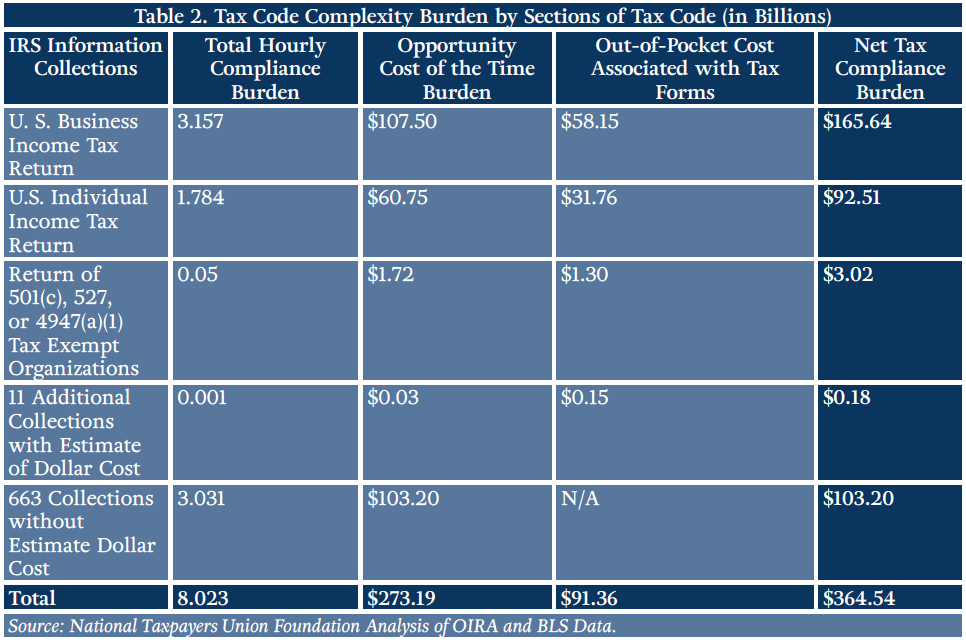

The total government-wide paperwork burden requires 11.3 billion hours in compliance time. The IRS comprises 71 percentof this amount at 8.023 billion hours. The next closest is the Department of Health and Human Services, imposing 1.4 billion paperwork compliance hours.

It is truly mind-boggling to consider the scale of 8.023 billion hours. This time frame is longer than 915 million years. Over this period, all 7 movies in the D.C. cinematic universe and all 22 movies in the Marvel cinematic universe (including the forthcoming Avengers: Endgame) could be binge watched 2,069,917 times consecutively.

B. Comparison to Last Year

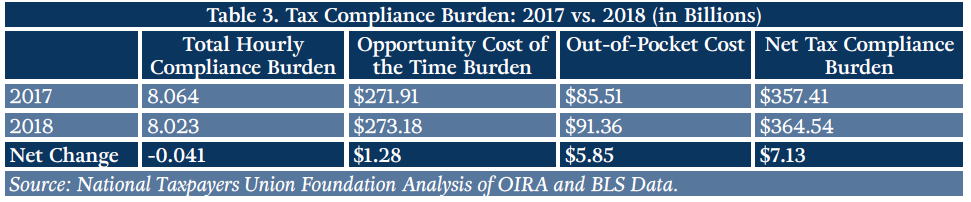

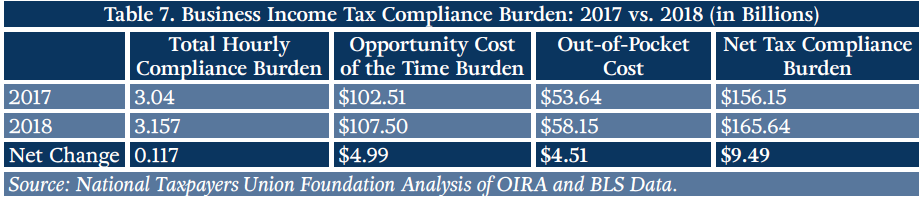

Compared to last year’s reported IRS data, the total hourly compliance burden fell by 41 million. However, the opportunity cost of this time rose by a net of $1.3 billion due to higher average wages and benefits as reported by the BLS compared to a year ago. It is also necessary to consider that the actual drop attributable to changes in the tax system would be greater were it not for the fact that the projected number of filers also increased– a natural consequence not only of population growth but more importantly of economic growth. Moreover, while the compliance burden was reduced on the individual income side of the tax code, businesses face new complexities and higher out-of-pocket expenses, as detailed below.

In order to make an apples to apples comparison, last year’s data was updated to include a datapoint that was not included in OIRA’s reginfo.gov database when NTUF accessed it last year. This year, the U.S. Business Income Tax collection projects an out-of-pocket expense of $58.2 billion (see Table 2, above). A corresponding figure for 2017 was not listed. The paperwork collection data for the Business Income Tax was updated in December 2018. The Supporting Statement (SS) for the revision shows that the 2017 dollar burden associated with this tax was $53.64 billion, a number that NTUF staff confirmed with the responsible OMB analyst.[5]NTUF has updated the compliance cost from last year’s Tax Complexity study to reflect this newly-available data in order to make comparisons easier.

As noted in Table 2, there are currently 663 IRS paperwork collections with a listed $0 cost. In some cases, the SS associated with a collection clarifies that the IRS does not expect that there are any costs. For example, regarding Form 4562 regarding Depreciation and Amortization (imposing 448 million compliance hours), the IRS notes, “There are no capital/start-up or ongoing operation/maintenance cost associated with this information collection.”[6]

There are other cases where the IRS has failed to report the estimated cost burden. For example, the U.S. Income Tax Return for Estates and Trusts and the Exempt Organization Business Income Tax Return do not list a cost, and the SS for each collection advises, “To ensure more accuracy and consistency across its information collections, IRS is currently in the process of revising the methodology it uses to estimate burden and costs. Once this methodology is complete, IRS will update this information collection to reflect a more precise estimate of burden and costs.”[7]

III. Individual Income Tax

A. 1040 Forms

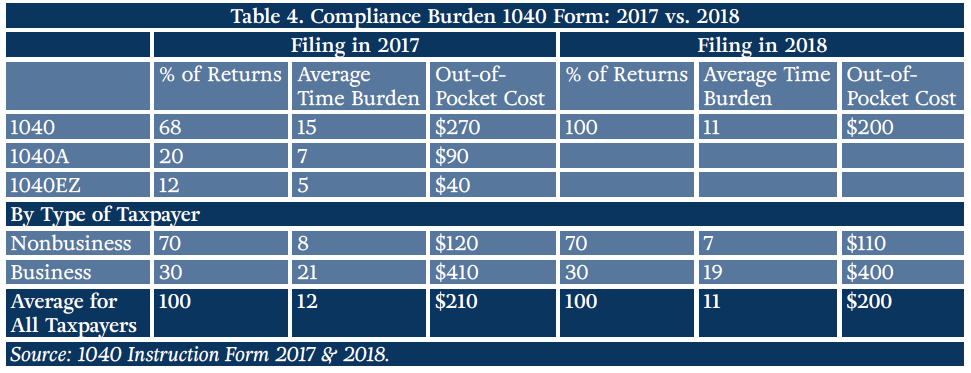

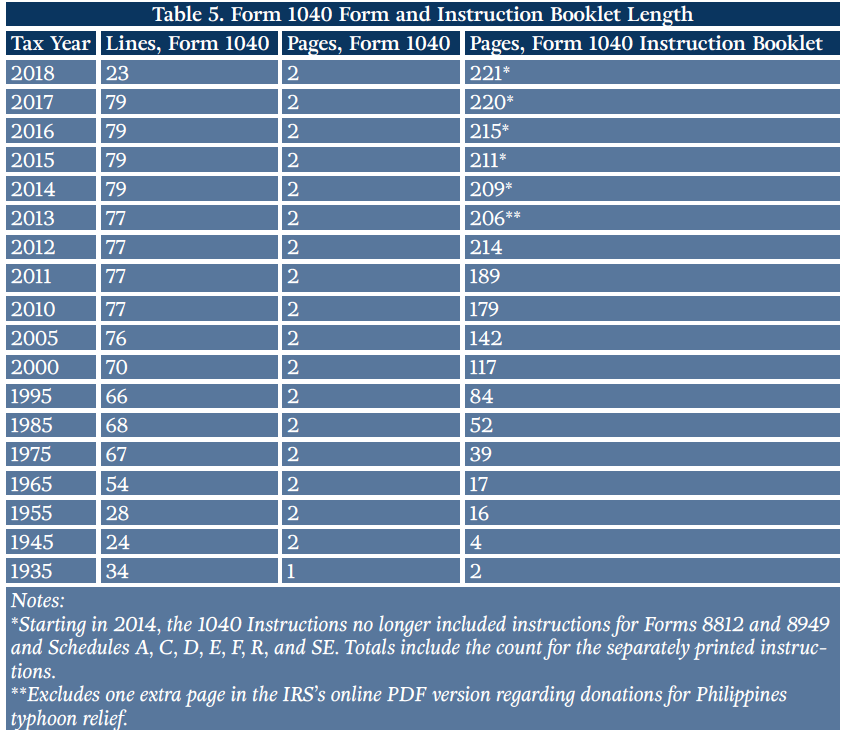

The basic form used by taxpayers to file their federal income taxes is the 1040. In previous years, taxpayers also had the option to use its simplified alternatives the 1040A and the 1040EZ. This filing season, the 1040 was modified and the 1040A and EZ were eliminated. The number of lines on the 1040 was reduced significantly from 79 lines to 26. An additional 6 new schedules were created for taxpayers with more complex returns. The Treasury Department’s Office of Tax Analysis projects that 25 percent of filers will not need to use any schedules this year.[8]In comparison, the 1040 Instructions for 2017 included a projection that 12 percent of filers would use the 1040EZ that year (see Table 4, below). Compared to last year, the IRS projects that 1040 filers will spend less time and face fewer out-of-pocket expenses.

B. Total Compliance Burden of the Individual Income Tax

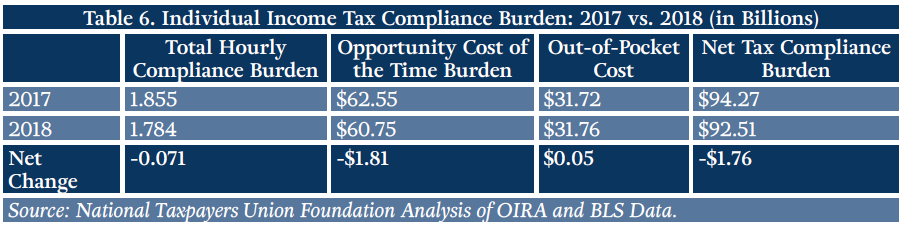

The compliance burden for the entire Individual Income Tax (IIT) collection will be reduced by a net of 71 million hours compared to last year. Although projected out-of-pocket cost estimates are up slightly, the net compliance burden is $1.76 billion lower than in 2017.

Many of the statutory changes enacted in the TCJA resulted in a net reduction of compliance burdens. The two largest include:

- Increase in the standard deduction: The IRS projects that 26 million fewer filers use Schedule A, thus saving 241 million hours and $2.9 billion in out-of-pocket costs.

- Increase in Alternative Minimum Tax threshold: the IRS estimates that the number of filers subjected to this onerous double-filing process will shrink from 10 million to less than 1 million, saving 13 million hours in compliance time and $557 million in out-of-pocket expenses.

There are, however, some statutory changes that will result in increased burdens, including:

- Section 199A Deduction for qualified business income: The TCJA created new deductions for pass-through businesses to deduct up to 20 percent of such business income from federal income taxes. Overall, this provision will save a great deal in net taxes paid but will require additional work from taxpayers to claim the deduction. The change is expected to increase the number of filers reporting sole proprietor and pass-through income and also to increase compliance burden for many of these filers, with an increase of 52 million hours and $1.3 billion in costs.

- New and modified credits: The TCJA increased the amount of the child tax credit and its phaseout threshold, created a new older dependent credit, and eliminated the domestic production credit. Combined, these are expected to increase the compliance burden by 2 million hours and $64 million out-of-pocket costs.

How does the burden of the average filer compare to last year? For 2018, the IRS’s IIT burden model projected 157.8 million filers, up from 152.9 million last year. Thus, the average compliance cost burden per filer was reduced by $30.29.

IV. Business Income Tax

Prior to the TCJA, the U.S. had the highest combined federal, state and local statutory corporate tax rate in the industrialized world. The TCJA dropped the federal rate from 35 percent to 21 percent. The law also eliminated the Corporate Alternative Minimum Tax, the domestic production credit, and several other general business credits. Combined, these saved filers 100 thousand hours and $4 million out-of-pocket expenses.

However, the law also increased complexity through international provisions that act essentially as a complicated alternative minimum tax, including the Global Intangible Low-Taxed Income (GILTI) provision, the Foreign-Derived Intangible Income Deduction, and the Base Erosion and Anti-Abuse Tax (BEAT). The IRS’ preliminary and limited projection in December 2018 estimated that, combined, these changes would increase the compliance burden by 900 thousand hours and $49 million. However, the IRS also noted that because the details regarding the administration and regulation of these new provisions were still being fleshed out, “an extensive evaluation of their direct costs cannot be provided at this time.”[9]

V. Components of Complexity

A. The Size of the Code

Tax laws are codified in U.S. Code Title 26, also known as the Internal Revenue Code (IRC). Wolters Kluwer Tax & Accounting estimates that the 1913 law that established the current income tax system was 27 pages in length. A report published that year including the “text of income tax amendments to the Constitution and Income Tax Act of 1913, plus regulations, rulings, official opinions, judicial decisions and forms” expanded the count of tax provisions to 400 pages.[10]

The Code has continued to steadily expand since then but the reported counts of the total number of pages can vary widely depending on the formatting of columns, page widths, or margins in the documents used … and whether the estimate includes the volumes of tax regulations. Last year, NTUF analyzed the IRC as published in 1998 and 2018 and found that over the 20-year period, the Tax Code had expanded by over 37,000 words per year, on average, reaching 3.97 million words. The currently available version of the Tax Code is slightly smaller, with 3.95 million words.[11]

A 2018 study of 300 posts made by President Trump on Twitter found that he used an average of 33 words per tweet.[12]At this Presidential Tweet Rate, it would take 119,933 tweets to add the entire 3.95 million-word Tax Code to the social media platform. Or, if for some reason you would prefer to listen to the Tax Code, that could take over 424 hours (roughly two and a half weeks straight) at Audible’s reported average reading speed of 9,300 words per hour.[13]

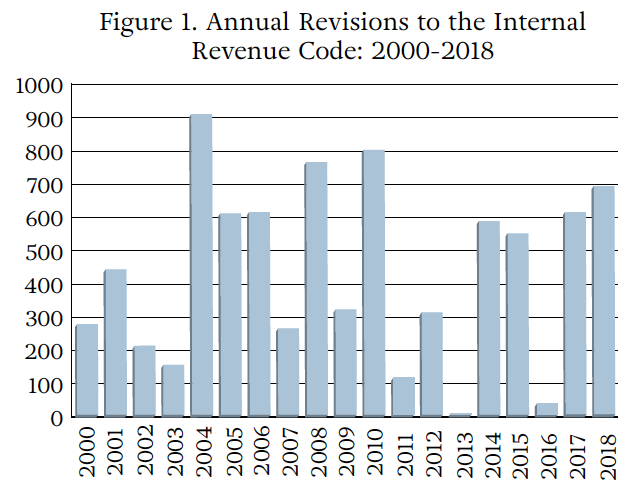

Since 2000, on average, 431 changes to the Tax Code were enacted each year (see Figure 1).[14]The number of changes recorded last year topped the amount in 2017 (the year the TCJA was enacted) due to the Consolidated Appropriations Act of 2018 which affected 557 revisions to the Tax Code, including technical corrections to laws pre-dating the TCJA.[15]

Keeping up with these annual changes and navigating through the labyrinthine laws is only part of the challenge for anyone trying to make sense of the system. The Department of the Treasury interprets the tax law in the 22 volumes of Title 26 of the Code of Federal Regulations. The most recently available version of Title 26 comprises 16,777 pages, down from 16,788 in the previous version.[16]The IRS also issues tax guidance through other means and can also retroactively impose regulation:

- Revenue Rulings: “A revenue ruling is an official interpretation by the IRS of the Internal Revenue Code, related statutes, tax treaties and regulations.”

- Revenue Procedures: “An official statement of a procedure that affects the rights or duties of taxpayers or other members of the public under the Internal Revenue Code, related statutes, tax treaties and regulations and that should be a matter of public knowledge.”

- Private Letter Rulings: “A written statement issued to a taxpayer that interprets and applies tax laws to the taxpayer’s specific set of facts.” While these are written in response to taxpayer requests for information to learn about the tax consequences of a transaction before it is made, the rulings “may not be relied upon as precedent.”

- Technical Advice Memoranda: “Guidance furnished by the Office of Chief Counsel upon the request of an IRS director or an area director, appeals, in response to technical or procedural questions that develop during a proceeding.”

- Notices: “A public pronouncement that may contain guidance that involves substantive interpretations of the Internal Revenue Code or other provisions of the law.”

- Announcements: “A public pronouncement that has only immediate or short-term value.”[17]

The IRS has been very busy issuing guidance pursuant to the reforms enacted in the TCJA. To date, the agency has published 21 proposed regulations, four Treasury Decisions of temporary or final regulations, 23 revenue procedures, four revenue rulings, and 49 notices.[18]

However, taxpayers are often left out in the cold if they have questions while preparing their annual taxes. First, it can be difficult to get through to the IRS. The difficulties that regularly occur, such as long telephone wait times, service levels, and unresolved mail correspondences, this filing season were exacerbated by the government shutdown.[19]

Second, entire areas of tax law are “out of scope” for telephone tax law assistance.[20]The IRS lists dozens of tax forms and topics for which it will not provide live assistance, including but not limited to international issues, the alternative minimum tax, trusts, and capital gains.[21]Many of these include what people might generally assume to be simple questions. Even certain changes made by the TCJA have also been designated out-of-scope, including “treatment of student loans discharged on account of death or disability or limitation on losses for taxpayers other than corporations.”[22]

Third, the IRS operates at least 60 different case management systems, which presents significant frustrations due to a lack of integration. This means that when a concerned taxpayer gets through to an IRS representative, that agent might not have access to that person’s file. This adds to the taxpayer’s wait time and aggravation as the representative tries to figure out who in the bureaucracy would be able to access the needed information.

Recordkeeping challenges can lead to inconsistencies that impact taxpayer rights: the Treasury Inspector General for Tax Administration identified discrepancies between taxpayer address or taxpayer representative information between the Master File and the Automated Non-Master File. Although complete details are not available, one possible example of address discrepancies was highlighted after media reports that Federal Reserve Board nominee Stephen Moore was assessed a $75,000 tax lien due to an error he had made on his taxes years ago. However, he claimed he had been unaware of the lien because the IRS was sending notices to an out-of-date mailing address. Tax expert and long-time IRS enrolled agent Ryan Ellis wrote on the matter:

… I’m familiar with this type of story. A taxpayer makes an honest mistake, the IRS computers start spitting out letters to which there is no reasonable appeal to a human being at the agency, and things spin out of control. This nightmare of a faceless bureaucracy churning letter after letter, leading to tax liens and levies, is a good argument against increasing the budget for the IRS.[23]

VI. Increased Use of Tax Preparation Assistance ... and Proposals for More Regulation

A.Increased Use of Tax Prep Assistance, and Higher Average Fees

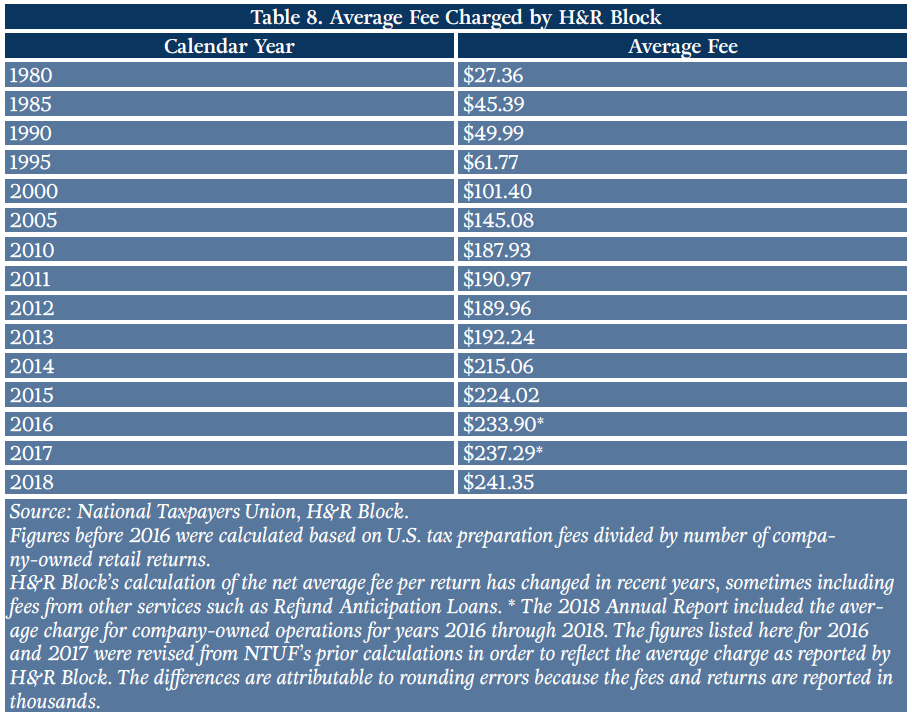

Because of tax complexity, the demand for tax assistance has increased: The IRS estimates that 95% of individual taxpayers use a paid preparer or tax software to complete their tax return and almost 90% of individual taxpayers e-file.[24]However, the average cost for prep assistance has been climbing along with the tax system’s complexity. For several years, National Taxpayers Union and National Taxpayers Union Foundation have tracked the average fee charged by H&R Block, one of the largest such preparation businesses in the country.[25]Perhaps not surprisingly, those fees have steadily increased along with the system’s complexity.

It should be noted that even after adjusting the $27.36 average fee from 1980 for inflation (equal to $85.86 in 2018 dollars), the cost of return preparation has nearly tripled since then, suggesting that the growth in tax complexity is outpacing even the technological and administrative improvements that have been made to professional preparation firms in that time.

B.IRS’s Heavy-Handed Attempts to Regulate Preparers

As more filers seek professional assistance, either to save time or out of fear of making an error and triggering an audit notice, the IRS has been attempting to increase its oversight for preparers. Under the law, the IRS has the authority to regulate “representatives” who “practice” before the agency. In 2011, the IRS, interpreting that as applying to all tax preparers, sought to impose a licensing system.

The IRS has also been seeking to increase regulation of tax return preparers through its annual budget submissions. The FY 2020 budget proposes yet again to try and expand authority to oversee paid preparers. The new regulatory power would be duplicative of existing mandates and related safeguards that are already in place. Each preparer must use a unique PTIN that can be used to identify patterns of fraudulent or questionable returns, preparers (and their firms) can also be liable for penalties for willfully taking unreasonable positions on filed returns,[26]and preparers have to fill out Form 8867, now known as the Paid Preparer’s Due Diligence Checklist, to ensure that they’ve taken certain steps to verify eligibility for certain refundable tax credits that are often a source of tax fraud. They face serious penalties, including injunctions, fines up to $100,000, and prison. Granting additional authority to the IRS could end up forcing many independent tax preparers out of business by increasing barriers to entry. The result could mean less competition and fewer choices for filers, as well as higher economy-wide compliance costs like those documented in this paper. Rather than expanding regulatory authority, the IRS should focus efforts on more efficient use of its current enforcement powers. The Treasury Inspector General for Tax Administration found “no evidence of a coordinated strategy in the IRS to address preparer misconduct.”[27]

C. "Return-Free” Could Impose More Reporting Burdens While Risking Taxpayers’ Privacy

Equally concerning is another long-standing scheme to establish a “Return-Free” system, which would have the IRS send pre-filled tax forms to citizens for their signatures.Advocates of this proposal point to countries such as Great Britain, Sweden, and Spain where this has been implemented, but fail to note that their tax systems are far simpler than in the U.S., or that it could require significant additional reporting mandates on employers that “would fall disproportionately on small businesses.”[28]They also fail to consider the IRS perpetual technological problems, its history of repeated abuse of power, and ongoing staffing challenges to ensure that IRS employees are adequately trained regarding taxpayer rights. It is also highly ironic to have the IRS automatically fill out the forms for taxpayers, yet questions to the IRS regarding tax form and schedule preparation have been ruled as “out-of-scope.”

In addition, the system could potentially short-change taxpayers of considerable savings. It is true that the IRS generally has a complete picture of a taxpayer’s income, but it rarely has a complete picture of what credits or deductions for which they might qualify. And naturally, it has no incentive to encourage taxpayers to take full advantage of provisions that could lower their tax bills. Worst of all, many Americans would likely be intimidated into submitting to the IRS’s supposed “voluntary” procedure out of fear that not doing so would provoke government retaliation. And, those taxpayers who dare challenge the information that the government pre-filled for them will have to run the gauntlet of the IRS’s ineffective customer service system.

In any case, a public-private partnership known as the Free File Alliance has for the past 15 years provided free electronic tax return filing to over 51 million moderate-income filers. For Tax Year 2017, Free File is available for filers with income ofless than $66,000. This service, overseen by more than a dozen online tax preparation firms, has saved consumers and taxpayers more than $1.5 billion in overhead costs since its inception, assuming a conservative $30 cost per prepared form.[29]These savings also accrue for the IRS itself due to the efficiency of processing fewer paper returns.

VII. A Better Tax System

Congress is currently considering the Taxpayer First Act of 2019 which would reform the IRS to improve safeguards for taxpayers when dealing with the IRS, upgrade management and customer service at the tax agency, make the Free File Alliance permanent, and create a pathway for modernizing administration of tax laws. If enacted, this would effectively bolster taxpayer rights.

Additional steps to reduce complexity could be addressed through a simple technical corrections bill to address unintended errors in the 2017 tax reform law. Before the 116th Congress was sworn in, the outgoing House Ways and Means Committee Chairman Kevin Brady (R-TX), published a discussion draft technical corrections bill that would fix many of the errors found in the TCJA. Such drafting errors are common in sweeping tax reform legislation.

One of the most important provisions this technical corrections bill would address is the infamous “retail glitch,” which unintentionally prevents qualified income property from being depreciated over the intended 15-year period. While one might be hopeful that there would be a bipartisan consensus to protect taxpayers from unintended complexity and confusion, that does not seem to be the case at this time.[30]

As noted above, the new GILTI and BEAT business tax provisions as well as the pass-through related provisions in the TCJA are expected to increase complexity and compliance burdens. The administration and lawmakers should seek to minimize the burdens of these provisions and their corresponding regulations, so that innocent taxpayers are not harmed.

One particular onerous and lingering source of complexity in the Tax Code is the Foreign Account Tax Compliance Act (FATCA). It was enacted to target so-called “fat cats” living abroad, yet its impact has been felt by earners across the spectrum, many of whom were forced to conclude that it was easier to renounce citizenship than comply with the law. The law imposes strict reporting requirements on foreign financial institutions, which has driven many to refuse to take on Americans as clients, imposing financial difficulties on U.S. citizens living in other countries. Texas A&M University Law Professor William Byrnes estimated that repeal of FATCA would reduce revenues by $150 million annually while cutting compliance costs on the economy by $200 million – a calculation that suggests the law imposes more burdens on the private sector than it raises for government.[31]Unfortunately, because FATCA’s burden is imposed on Americans and “accidental Americans” overseas, the impacted constituency is dispersed and has no direct representation in Congress, making overhaul or repeal of the egregious law an uphill battle.

VIII. Conclusion

The IRS projections for the 2019 filing season show that the overall time compliance burden fell from the previous year, a rarity except in periods of economic decline. The IRS does conduct regular surveys of taxpayers to get real data and feedback on how long it takes taxpayers to do all the record-keeping and other tax preparation or filing activities, and how much is spent out-of-pocket to prepare and file taxes. NTUF expects that this data will be available by the end of 2019.

Lawmakers need not wait until then to see how the revised Tax Code is working out. While TCJA made some commendable changes that reduce complexity, the currently available data points to remaining challenges that need to be addressed to ensure that the tax system is not imposing onerous, unnecessary burdens on taxpayers nor standing in the way of economic progress.

[1]Office of Information and Regulatory Affairs. “Inventory of Currently Approved Information Collections.” Accessed on April 5, 2019 at https://www.reginfo.gov/public/do/PRAMain.

[2]Bureau of Labor Statistics. “Employer Costs for Employee Compensation – December 2018,” Tuesday, March 19, 2019. https://www.bls.gov/news.release/pdf/ecec.pdf.

[3]Fortune. “Global 500.” Accessed April 9, 2019 at https://fortune.com/global500/.

[4]World Bank. “National Accounts Data, GDP (current US$).” Accessed April 10, 2019 at https://data.worldbank.org/indicator/NY.GDP.MKTP.CD?view=map&year_high_desc=trueAccessed.

[5]Internal Revenue Service.” Supporting Statement: U.S. Individual Income Tax Return,” December 20, 2018. https://www.reginfo.gov/public/do/PRAViewDocument?ref_nbr=201805-1545-019.

[6]Internal Revenue Service. “ Supporting Statement: Internal Revenue Service OMB Control Number 1545-0172 Form 4562 Depreciation and Amortization (Including Information on Listed Property),” May 1, 2017. https://www.reginfo.gov/public/do/PRAViewDocument?ref_nbr=201704-1545-011.

[7]Internal Revenue Service. “Supporting Statement: U.S. Income Tax Return for Estates and Trusts Form 1041, schedules, and PL 115-97, section 14103 OMB Control Number 1545-0092.” March 5, 2018. https://www.reginfo.gov/public/do/PRAViewDocument?ref_nbr=201803-1545-002.

[8]Internal Revenue Service. “Supporting Statement: U.S. Individual Income Tax Return OMB Control Number 1545-0074,” October 11, 2018. https://www.reginfo.gov/public/do/PRAViewDocument?ref_nbr=201808-1545-031.

[9]Internal Revenue Service. “Supporting Statement: U. S. Business Income Tax Returns OMB Control Number 1545-0123,” December 20, 2018. https://www.reginfo.gov/public/do/PRAViewDocument?ref_nbr=201805-1545-019.

[10]Wolters Kluwer, CCH. “Fact Sheet: 100-Year Tax History: The Length and Legacy of Tax Law,” 2013. https://www.cch.com/wbot2013/factsheet.pdf.

[11]U.S. House of Representatives Office of the Law Revision Counsel, Annual Historical Archives. Accessed April 11 at https://uscode.house.gov/download/annualhistoricalarchives/pdf/1998/index.html. Additional available yearly archives since 1994 can be found by changing the year in the link. The version published on March 16, 2018 was accessed April 12, 2018 at https://uscode.house.gov/download/download.shtml.

[12]Editist. “Quantifying Trump’s Love of Adverbs and Exclamation Points,” 2018. https://editist.com/trump-adverbs-exclamations/.

[13]Commins, Karen. “Simple math about audiobook rates,” KarenCommins.com, June 13, 2011. https://www.karencommins.com/2011/06/some_simple_math_about_audiobo.html/

[14]Office of the Law Revision Counsel. United States Code Classification Tables: 2018, U.S. House of Representatives. https://uscode.house.gov/classification/tables.shtml.

[15]H.R.1625 Consolidated Appropriations Act, 2018.https://www.congress.gov/bill/115th-congress/house-bill/1625/text.

[16]U.S. Government Publishing Office. Code of Federal Regulations (Annual Edition).Accessed April 9, 2019 at https://www.gpo.gov/fdsys/browse/collectionCfr.action?selectedYearFrom=2018&go=Go.

[17]Internal Revenue Service.Understanding IRS Guidance – A Brief Primer. December 18, 2018. https://www.irs.gov/uac/understanding-irs-guidance-a-brief-primer.

[18]Internal Revenue Service. Tax Reform Guidance, Updated April 1, 2019. https://www.irs.gov/newsroom/tax-reform-guidance.

[19]Moylan, Andrew and Wilford, Andrew. Congress and Administration Should Look Into Extending Tax Filing Deadline, March 7, 2019. https://www.ntu.org/library/doclib/2019/03/Congress-and-Administration-Should-Look-Into-Extending-Tax-Filing-Deadline-2.pdf.

[20]National Taxpayer Advocate. Annual Report to Congress: 2016 Executive Summary, January 2017, page 29. https://taxpayeradvocate.irs.gov/Media/Default/Documents/2016-ARC/ARC16_ExecSummary.pdf.

[21]Internal Revenue Service. Customer Account Services Chapter 21 Exhibit 21.1.1-1, September 4, 2018. Accessed April 10, 2019 at https://www.irs.gov/irm/part21/irm_21-001-001.html#d0e2109.

[22]National Taxpayer Advocate.Annual Report to Congress: 2018 Volume 1,February 12, 2019. https://taxpayeradvocate.irs.gov/Media/Default/Documents/2018-ARC/ARC18_Volume1.pdf.

[23]Ellis, Ryan. “The fake news about Stephen Moore’s tax audit,” Washington Examiner, March 28, 2019. https://www.washingtonexaminer.com/opinion/the-fake-news-about-stephen-moores-tax-audit.

[24]Internal Revenue Service. Supporting Statement: U.S. Individual Income Tax Return, December 20, 2018. https://www.reginfo.gov/public/do/PRAViewDocument?ref_nbr=201805-1545-019.

[25]H&R Block. Annual Reports, https://investors.hrblock.com/financial-information/annual-reports.

[26]Klasing, David. “Tax Preparers: Who May Be Liable, and For How Much,” March 27, 2014, Tax Law Offices of David W. Klasing Law Blog. https://klasing-associates.com/tax-preparers-may-liable-much/.

[27]Treasury Inspector General for Tax Administration.The Internal Revenue Service Lacks a Coordinated Strategy to Address Unregulated Return Preparer Misconduct, July 25, 2018. https://www.treasury.gov/tigta/auditreports/2018reports/201830042_oa_highlights.html.

[28]Novack, Janet. “Five Fallacies about Return-Free Tax Filing,” Forbes, April 9, 2013. https://www.forbes.com/sites/janetnovack/2013/04/09/five-fallacies-about-return-free-tax-filing/#2b32e0f72e92.

[29]Internal Revenue Service. “Free Tax Software Available Now through Free File; Partnership Launches its 16th Year of Free Assistance to Taxpayers,” January 12, 2018. https://www.irs.gov/newsroom/free-tax-software-available-now-through-free-file-partnership-launches-its-16th-year-of-free-assistance-to-taxpayers.

[30]Gardner, Parker. “Democrats are blocking bipartisan agreement on tax code fixes,” Washington Examiner, March 8, 2019. https://www.washingtonexaminer.com/opinion/democrats-are-blocking-bipartisan-agreement-on-tax-code-fixes.

[31]Green, Nigel. “A Corporate-Welfare Bonanza for Tax-Compliance Firms,” The Wall Street Journal, April 2, 2017. https://www.wsj.com/articles/a-corporate-welfare-bonanza-for-tax-compliance-firms-1491163938?mg=prod/accounts-wsj.