Issue Brief #178

June 28, 2018

By Andrew Wilford

(pdf)

The passage of the historic Tax Cuts and Jobs Act (TCJA) in late 2017 has seen Republicans riding high on a successful economy, but the job of fixing the mess that is the American tax code is far from over. Republicans know this and have turned their attention to what’s called Tax Reform 2.0, a second bite at the apple of making the American tax code fairer, flatter, and simpler.

One reform that should be foremost in the minds of Congressional tax writers is changing higher education tax policy to streamline a bloated portion of the code.

Access to a good education for all is a cornerstone of the American dream. Ensuring that every American can secure a high-quality education is important in an increasingly knowledge-based economy. Unfortunately, the way the federal government currently supports access to higher education is highly inefficient and often regressive. House Republicans attempted to reform this system as part of TCJA, but these reforms were left behind as the legislative process progressed and the provisions were dropped in the Senate version of the bill.

Now, with Congress looking at Tax Reform 2.0, reforms to higher education should once again be on the table.

The Current System

Currently, the federal government uses tax credits, grants, and loan programs to try to make education more affordable. However, this combination has resulted in a system that is difficult for students to navigate and often duplicative. Tax provisions intended to provide access have included:

American Opportunity Tax Credit (FY 2015 foregone revenue- $17 billion): A credit for qualified education expenses that provides a maximum of $2,500 per year, per student, for a maximum of four years. The credit covers 100 percent of the first $2,000 of expenses, then 25 percent of the next $2,000 for a maximum of $2,500. Additionally, $1,000 of this credit is refundable, meaning it can be collected even by those with zero income tax liability.

Dependent Exemption for Students Between the Ages of 19-23 (FY 2015 foregone revenue- $4.5 billion): Allows parents to claim a dependent exemption beyond the normal limit of 18 (up to age 23) if the dependent is enrolled in a qualifying institution for at least five months during the year.

Exclusion of Scholarships, Fellowship Grants (FY 2015 foregone revenue- $2.7 billion): Scholarship or fellowship grant income is currently tax-deductible if used towards tuition and related fees (not room and board).

Exclusion of Scholarships, Fellowship Grants (FY 2015 foregone revenue- $2.7 billion): Scholarship or fellowship grant income is currently tax-deductible if used towards tuition and related fees (not room and board).

Lifetime Learning Credit (FY 2015 foregone revenue- $2.7 billion): Provides a credit for expenses towards any postsecondary education tuition, regardless of age. The credit’s value is 20 percent of costs of tuition and related fees, for a maximum of $2,000.

Student Loan Interest Deduction (FY 2015 foregone revenue- $2 billion): Allows the deduction of interest payments on education loans, for a maximum of $2,500.

Total FY 2015 foregone revenue: $28.9 billion.

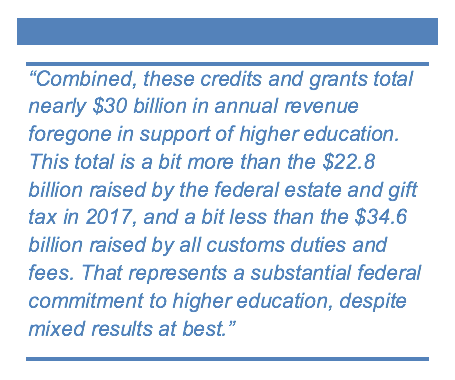

Combined, these credits and grants total nearly $30 billion in annual revenue foregone in support of higher education. This total is a bit more than the $22.8 billion raised by the federal estate and gift tax in 2017, and a bit less than the $34.6 billion raised by all customs duties and fees. That represents a substantial federal commitment to higher education, despite mixed results at best.

As these credits have become more generous, they have increasingly begun to push benefits towards wealthier Americans. A 2012 analysis by Stephen Burd found that higher education tax credits over the period between 2009-2011 benefited upper-income Americans to a significantly greater degree than the period between 1999-2001, around the time when many of these credits were instituted. Tax credits are, in general, an inefficient way to provide help with access to education to low-income students, as many individuals in this income group are not liable for significant tax bills to begin with.

This reflects a growing and unfortunate trend in federal involvement in higher education. Student loan programs such as Public Service Loan Forgiveness disproportionately benefit wealthier students. Income-based repayment, another program intended to provide relief on federal loans, has been found to primarily assist middle- and upper-income loanees that go on to graduate school. In other words, higher education tax credits tend to help wealthier graduate students that are already favored by other aspects of federal education policy.

Higher education tax incentives not only represent significant foregone revenue, they are ultimately of dubious value in achieving their stated goal. Research by George Bulman and Caroline Hoxby suggests that higher education tax credits have ultimately had no effect on ability to attend college or even the amount spent on college costs.

Higher education tax credits have also been plagued with fraud. A 2010 report by the Treasury Inspector General for Tax Administration studied claims filed over the span of just six months, and found that 2.1 million claims totaling $3.2 billion were erroneous.

Other concerns have arisen about higher education tax incentives’ side effects. Borman and Hoxby’s conclusion fits with a similar study by the Federal Reserve Bank of New York which found that tuition increases could be tied to increased federal aid in higher education.

Not all education policies are poorly-structured credits, however. One successful policy in place is the Qualified Tuition Program, better known as “Section 529 plans” in reference to the section of the Internal Revenue Code in which they appear. 529 Plans allow investment income to accumulate tax-free, and withdrawal is excluded from taxation as long as the money is used towards qualifying education expenses. This is similar in concept to other successful policies allowing tax-advantaged savings, like Individual Retirement Accounts.

The Republican Plan

The House tax plan made several significant changes to the way the tax code treats students pursuing higher education. The student loan interest deduction, which allows students to deduct interest payments on student loans up to $2,500, would have been eliminated. While some suggested that this would have harmed students with significant loan debt, the greatest amounts of debt are taken out by high-income graduate students. This means that high-income graduate students benefit most from the student loan interest deduction. The student loan interest deduction is also duplicative of other, similar loan forgiveness programs, including Income-Based Repayment and Public Service Loan Forgiveness.

The elimination of the student loan deduction has long been an area of bipartisan agreement. The Obama White House proposed repealing the student loan deduction along with an expanded American Opportunity Credit. The House plan aimed for similar reforms.

The House plan also would have consolidated three existing programs: the American Opportunity Credit, the Lifetime Learning Credit, and the Hope Scholarship Credit. These programs would have been brought together under an expanded American Opportunity Credit. The new American Opportunity Credit would have remained the same for the first four years, while adding a fifth year of eligibility. In this fifth year, the American Opportunity Credit would cover 100 percent of the first $1,000 of costs, then 25 percent of the next $1,000. The maximum value of the credit in its fifth year would therefore be $1,250.

The House Republican plan would also have phased out Coverdell Savings Accounts. Coverdell Savings Accounts are similar to 529 Plans, in that withdrawals are tax-free so long as they go towards qualified education-related expenses, with a few major differences. Coverdell Savings Accounts have a $2,000 annual contribution limit per beneficiary, and cannot be contributed to once a beneficiary turns 18. Generally, Coverdell Savings Accounts cannot be continued once the beneficiary turns 30. Under the House plan, current Coverdell Savings Accounts would have been allowed to be withdrawn for education-related expenses under favored tax status, or rolled into a 529 plan.

In lieu of Coverdell Savings Accounts, 529 Plans would have seen their eligibility expanded. 529 Plans currently can be used only for post-secondary education, but would be expanded to be eligible for private grade school and high school expenses, as well as apprenticeship programs. Usage of 529 plan withdrawals for these purposes would have been limited to $10,000 annually per beneficiary.

Expansion of 529 plan eligibility would make it easier to enroll in private schools for grade and high school. This would provide parents with more choice in determining where their children receive their education. While Congress did expand 529 eligibility to include K-12 expenses in TCJA, an effort to include homeschool and vocational expenses as well was left on the cutting room floor and should be revisited in future reform discussions.

Other eliminated deductions include the deduction for tuition waivers and the deduction for employer-provided tuition assistance. These deductions are politically popular, but of dubious value to students.

The tuition waiver deduction allows undergraduate students to deduct the cost of tuition waivers from taxable income. Graduate students may deduct these costs provided that they perform teaching or research duties. Graduate students are therefore receiving a form of payment for services rendered, which for anyone else would be termed taxable income. With the tuition waiver deduction in place, graduate students are able to get away with avoiding taxes on these “waivers.”

Employer-provided tuition assistance, on the other hand, is an element of a system of fringe benefits with its roots in World War II-era wage ceilings. To get around artificial wage constraints, unions successfully lobbied Congress to grant workplace benefits tax-exempt status. Instead of being paid in cash, employees received an array of benefits that drive up costs of services. The employer-provided health insurance exclusion, for example, distorts the cost of health care, making it more expensive for everyone.

Tax incentives for employer-provided tuition assistance have a similar effect. Tuition is made more expensive because the government is artificially increasing demand for graduate school. Tuition assistance can turn out to be a productive investment for businesses, but the federal government should not be distorting tuition prices through the tax code.

In total, this simplification of the tax code’s treatment of higher education would have raised $17.3 billion over 10 years. This increased revenue could, in turn, be put towards further tax cuts which will benefit all Americans through increased after-tax income.

Conclusion

The current system of higher education tax credits is expensive, heavily weighted against students most in need of help, and dubiously effective. If the federal government involves itself in higher education, it should target policies at improving college availability for the neediest Americans. As it stands, higher education tax credits are more likely be wasteful at best, benefiting graduate students with a high likelihood of substantial future incomes, and harmful at worst, driving up tuition prices.

Congress punted on higher education during Tax Reform 1.0, but Tax Reform 2.0 provides it with another possession that can help them put points on the board for taxpayers. Congress should use this opportunity to rationalize and update the way that tax policy affects education and ensure that taxpayer dollars are being used efficiently and effectively.

About the Author

Andrew Wilford is an Associate Policy Analyst with the National Taxpayers Union Foundation.