(pdf)

This filing season is even more taxing than others in recent history. As the National Taxpayers Union Foundation (NTUF) noted earlier this year, this is a disastrous tax season.[1] The Internal Revenue Service's (IRS) major backlog has caused headaches for filers while they wait for previous years’ refunds or other documents needed to file this year's tax. Worse, some letters the IRS sent to many filers with information on amounts of payments for last year's complicated advanced child tax credits had erroneous information. And of course, the IRS's poor performance of answering its phone lines has made it hard for taxpayers to get in touch with IRS agents.

Even if they were able to get through to a live person at the agency but had questions beyond the basics, they likely ended up having to pay out of pocket for advice from a tax preparation professional. It can be painful to have to pay a professional to help you figure out how to pay your taxes. But beyond that financial cost, there is also a massive time burden imposed on individuals and businesses because of the time spent filling out tax forms and filing each year under our complicated tax regime.

Using official data sources, these burdens can be calculated to estimate the total cost, in terms of both time and dollars, of complying with the U.S. tax code. NTUF’s annual study of the tax system finds that complexity is once again on the rise. The tax code, along with its volumes of regulations, is expanding, leaving taxpayers to spend more time laboring over forms when filing.

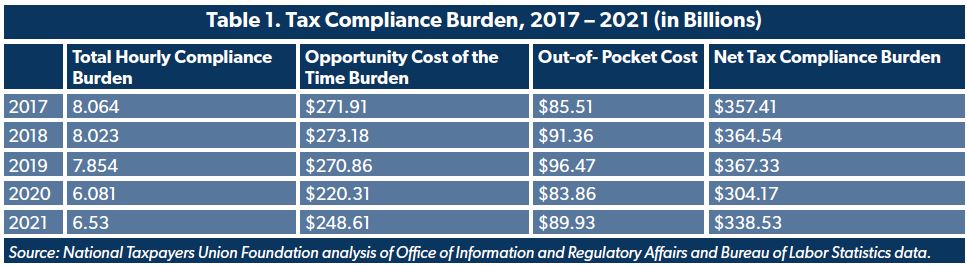

This tax season, taxpayers spent over 6.5 billion hours filing their taxes, an increase of 451 million hours over 2020 after the overall compliance burden had fallen over the previous three years. Based on average private sector salaries, this represents an opportunity cost of $249 billion. Adding in the nearly $90 billion spent out-of-pocket on tax preparation, the total compliance burden of the tax code totals $339 billion.

While the increase is concerning, it should be noted that nearly three-quarters of the increase is due to the IRS revising its estimate of the compliance burden of claiming the Qualified Business Income (QBI) deduction established in the Tax Cuts and Jobs Act (TCJA). Even though the provision was known to be complicated when the bill was passed, last year, the agency grossly underestimated the compliance burden at 30,000 hours. This year, it increased its estimate of the compliance burden of this provision by over 1 million percent to over 336 million hours.

The IRS should provide additional background information regarding changes of this magnitude. Taxpayers can also assist the IRS’s estimation process by providing comments and feedback to the agency when it annually posts revisions to tax forms and burden estimates in the Federal Register. With better and more timely data, lawmakers can take steps to simplify filing burdens.

The Tax Code’s Increasing Complexity and Compliance Burden

Time and Cost Burdens Increased in 2021 …

According to our analysis of data and supporting documentation that the Internal Revenue Service (IRS) files with the Office of Information and Regulatory Affairs (OIRA), altogether, complying with the tax code in 2021 consumed 6.53 billion hours for recordkeeping, learning about the law, filling out the required forms and schedules, and submitting information to the IRS.[2]

The cumulative time spent on taxes stretches out to over 745 thousand years. NASA’s New Horizon probe took nine and half years to travel to Pluto. It would be able to make 39 thousand roundtrips to the dwarf planet over the current compliant horizon.

We can calculate an estimate of the value of this time burden using private sector labor costs. According to the Bureau of Labor Statistics (BLS), U.S. non-federal civilian employers spent an average of $38.07 per hour worked by their employees in December 2021. This includes all wages, salaries and benefits provided.[3]

The opportunity cost of the billions of hours spent on taxes is equivalent to $249 billion in labor – valuable time that could have been devoted to more productive or pleasant pursuits, but was instead lost to tax code compliance. Add to that the $90 billion in estimated out-of-pocket costs taxpayers spent on software, professional preparation services, or other filing expenses, and the total economic value of the compliance burden imposed by the tax code can be calculated at $339 billion.

To put this figure into context, it is approaching the cost of the net interest payments on the federal debt projected by OMB this year, $356 billion, and is bigger than the GDP of all but 34 nations, surpassing Ireland, Denmark, and Singapore.

… But There’s More to the Story

The time burden has gone up, but not necessarily by as much as indicated in the data reported by the IRS. Any time any federal agency requires the public to fill out any sort of form, it is called an “information collection.” Every agency that issues a form is required under the Paperwork Reduction Act to estimate how long each respondent will take to fill it out, as well as any potential out-of-pocket expenses incurred as a result, and it must get approval from the Office of Management and Budget. In general, federal agencies must get each collection re-approved on a 3-year cycle, but most collections under the Internal Revenue Code are reviewed every year.

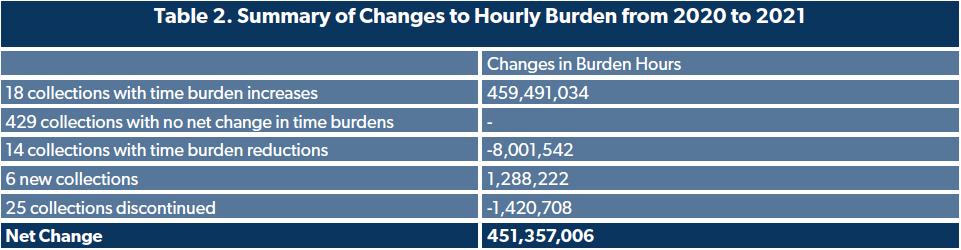

Table 2 provides a summary of the changes in time burden estimates since the previous tax year. The vast majority of the information collections were re-approved with no change, some were discontinued since last year, and a few were added. While there were fourteen collections with lower time estimates, saving filers 8 million hours, the biggest changes the IRS made were increased time burden estimates for 18 information collections by a total of 459 million hours. Nearly three-quarters of the change here was due to a revision of burden estimates under forms for the Qualified Business Income Deduction. Last year, the IRS estimated that 10,000 filers would spend a cumulative total of 30,000 hours working on these tax forms. The revision pumps the estimate up to over 41 million filers devoting 336 million hours.

The QBI deduction is available to small businesses known as “pass-throughs” because their profits are “passed through” the business and claimed by the owners of the business on their individual income tax returns. Before the pandemic, upwards of 90 percent of businesses were pass-throughs. The QBI deduction allows these taxpayers to deduct up to 20 percent of business expenses, and was added in the TCJA to keep pass-through taxation on par with corporate tax rates that received a different tax cut under the reform.

However, it was known to be a complicated fix even while it was being debated, so it was surprising that the IRS estimate before this year was so low, especially given that the 2019 IRS Complete Report (Publication 1304 (Rev. 12-2021)) showed that nearly 19 million filers claimed the deduction in 2018 and 22 million claimed it in 2019. The Supporting Statement filed with the change in the information collection did not provide much detail about the drastic revision. NTUF reached out to the IRS for additional information but did not receive a reply before publication of this paper.

Ceteris paribus, if the adjustment for the QBI had been accounted for last year, the net time compliance burden would have reflected 6.42 billion hours, resulting in a net increase this year of 113 million hours.

NTUF noted a similar issue last year regarding a major change that saw the business income tax burden estimate drop by two-thirds with little explanation at the time.[4] NTUF learned the reasons for the re-baselining of the estimate in a discussion with the IRS last December, and the agency also published a backgrounder about the change.[5] As part of its process for estimating time burdens, the IRS sends out surveys to taxpayers with detailed questions about how much time the individual or business spent on various tax preparation and filing activities. A few years back, the IRS realized that the survey questions to businesses were resulting in double counting of some of the recorded time burdens. They adjusted their survey questions and calculated the revised time estimates but waited to adjust the official reported estimate with the new methodological corrections so that the impacts of the TCJA – the first comprehensive overhaul of the tax code in a generation – could be seen under the IRS’ original paperwork burden baseline.

NTUF appreciates the IRS’s transparency in publishing an explainer of the re-baselining that happened last year. But to echo what NTUF recommended last year, the IRS should continue to shed more light on its taxpayer burden model and calculations and strive to do so in a timelier manner. Transparency of the data and model would allow for assessment and feedback to improve the calculations. The IRS should also work to provide more accountability on the massive compliance burdens imposed on taxpayers through the tax code so that lawmakers can address areas of concern. This effort could also help fill in the gaps in missing cost estimate burdens across major sections of the tax system (see below).

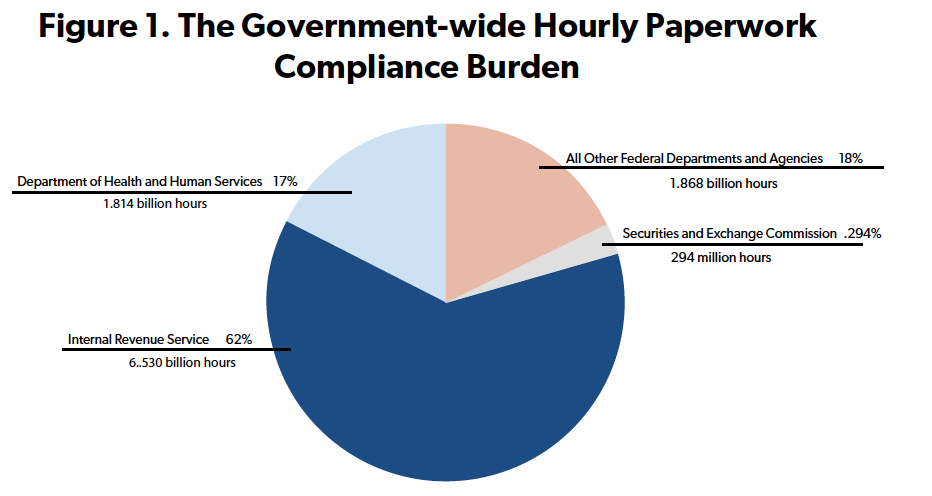

Tax Forms Dominate the Government-wide Paperwork Burden

The OMB’s Office of Information and Regulatory Affairs maintains a database of all the information collections across the federal departments and agencies. Currently there are 9,774 different collections. While the IRS’s various forms comprise just 5 percent of all the information collections, they consume nearly two-thirds of the 10.5-billion-hour paperwork burden imposed across all government agencies. The next largest source of paperwork is the Department of Health and Human Services, imposing 1.8 billion hours, 17 percent of the government. The Security and Exchange Commission requires 294 million hours complying with forms, topping the other departments.

The Tax Code is Expanding Again

One source of complexity and compliance confusion stems from the sheer size of the tax code. The tax code had relatively humble beginnings: the income tax was enacted in 1913 through a bill that was originally 27 pages in length. Amendments, regulations, and judicial rulings increased the length to 400 pages.[6] Through the steady implementation of new provisions, which required corresponding new regulations over the next 100-plus years, lawmakers expanded the tax system into a labyrinthine behemoth. The TCJA helped reduce compliance hours and also led to a period of successive years in which the tax code became slightly smaller.

The total number of pages of the tax code can vary widely depending on the formatting of columns, page widths, font, or margins in the documents. For example, this year’s PDF of the Internal Revenue Code, (Title 26 of the U.S Code of public laws) published on the House of Representatives’ website runs 6,874 pages (vs 6,571 last year) while the archived version of the Code from 2019 with a smaller font and two columns per page stands at 3,945 pages.

To help standardize year to year comparisons, NTUF has copied the texts of the Tax Code PDFs into Microsoft Word in order to use the program to generate a word count. The results may not be perfect given the number of cross-references to various sections of law through the code, but it provides a consistent methodology, and was also used in the past by the Office of the Taxpayer Advocate to find that in 2017 the code had 4 million words.

After passage of the TCJA, the number of words began to fall, receding to 3.96 million by 2020. But the tax code is again on rise, ticking up to 4,085,524 words in the latest version published on the House of Representatives’ website as of April 8, 2022.[7]

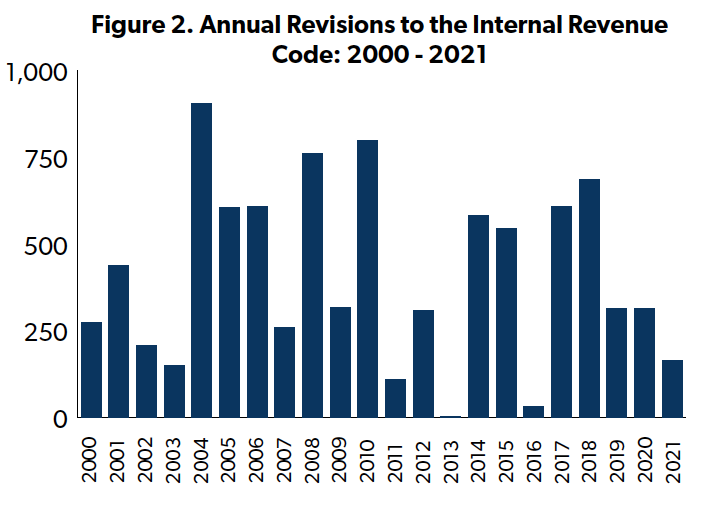

Lawmakers also make frequent revisions and additions to tax laws. From 2000 through 2021, Congress enacted, on average, 408 changes to the tax code each year (see Figure 2), ranging from a low of three in 2013 up to 797 in 2010.[8] While the changes in the past few years have been lower than average, they have been significant, including the recovery rebates in 2020 and 2021 and the new advance child tax credits in the American Rescue Plan Act (ARPA).

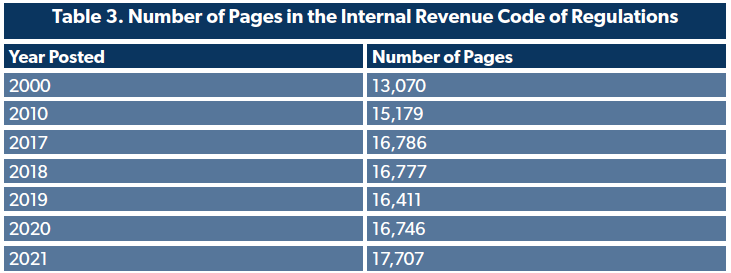

To interpret and implement all of these changes to tax laws, the Department of Treasury develops and publishes regulations across 22 volumes of the Code of Federal Regulations. The most recently available complete version of tax regulations, published online with revisions through April 2021, comprises a record length of 17,707 pages (including tables of contents and additional introductory prefaces in each volume).[9] The previous high mark was reached in 2017, then after two years of reductions, the regulatory count began to rise in 2020.

In addition to issuing all these regulations, the IRS also releases regular guidance, notices, announcements, private letter rulings, and technical advice memorandums in response to various issues that arise.[10] Some of these pertain to individual cases and have limited scope, other may involve substantive interpretations of tax laws.

For taxpayers with complicated finances, that is a lot of information to keep track of to ensure a proper understanding of applicable tax laws, regulations, and rulings. The ongoing issues related to the pandemic and complicated changes in law continue to impose difficulties on taxpayers seeking assistance and information from the IRS.

Getting filing advice from the IRS was already difficult. Previous editions of our annual tax complexity study have warned that the agency considers vast areas of the tax code as “out of scope” for the IRS tax preparation assistance programs like the Volunteer Income Tax Assistance and Tax Counseling for the Elderly.[11] The guidance means that IRS agents cannot answer questions about these specified areas of the tax laws. There are also areas that are “out of scope” for telephone assistance. An online guide for IRS account management lists 14 tax forms that are “out of scope” and also notes that the list is “not all inclusive.”[12] Apparently, the full list of “out of scope” services is also “out of scope.”

The Complexity Burden of Sections of the Tax Code

Overview of Tax Forms

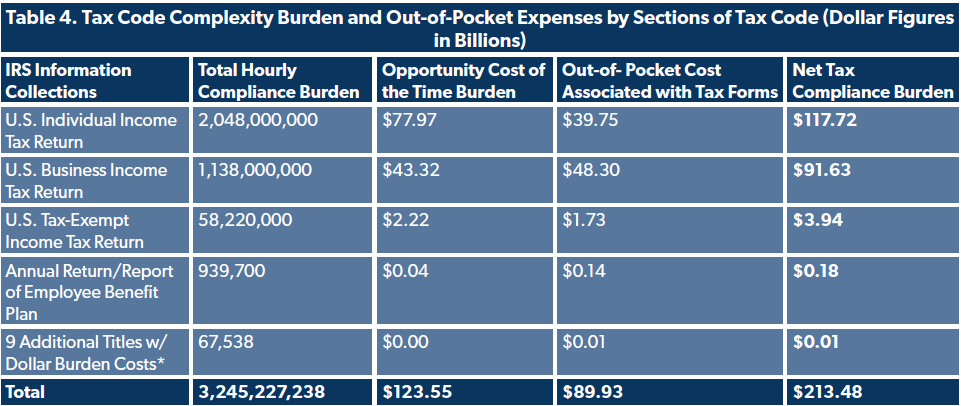

Table 4, below, breaks out the latest data on compliance burdens associated with the thirteen information collections for which the IRS has provided an out-of-pocket expense estimate. The top two areas, the individual and business tax forms, are discussed below. The third area concerns tax-exempt organizations, which are required to file forms with the IRS to provide transparency regarding financial information and for purposes of IRS enforcement and regulation of certain activities. The fourth collection on the list is a joint effort of the IRS and the Department of Labor pursuant to a law requiring administrators of employee pension and benefit plans to file annual returns or reports to the federal government. In addition to these, there are nine sets of paperwork that require 68 million hours and $7 million in out-of-pocket expenses.

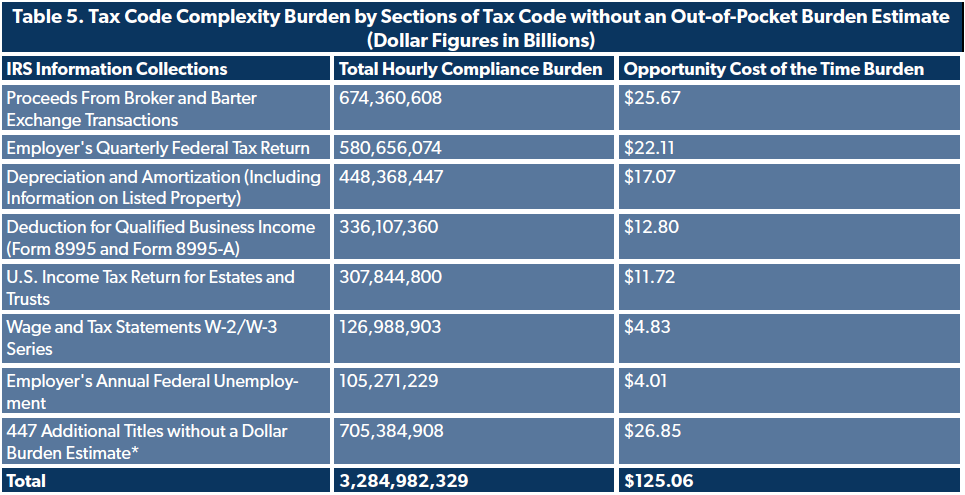

Table 5 shows the remaining 454 IRS collections that do not have an estimated out-of-pocket expense. The seven sets of paperwork with time burdens over 100 million hours are listed and the remaining 447 are grouped together. In some cases, an expense estimate is not listed because there is no actual associated cost. For example, W-2 forms are quick to fill out and do not impose any expenses. However, expense data is missing from some of these collections because the IRS has perhaps incorrectly projected that there are no associated expenses with the forms.

A noteworthy example of this was highlighted in NTUF’s 2021 tax complexity report. The IRS had previously reported that there were “no capital/start-up or ongoing operation/maintenance costs” associated with Form 4562, used for calculating Depreciation and Amortization (imposing 448 million compliance hours).[13] In response to that NTUF commented:

It is, of course, implausible that a form that imposes a time cost of nearly 450 million hours has no out-of-pocket costs associated with it, suggesting that compliance burdens could remain significantly underreported in some ways.[14]

In the Supporting Statement included with that form when it was reapproved in 2020, the IRS notes instead, “To ensure more accuracy and consistency across its information collections, IRS is currently in the process of revising the methodology it uses to estimate burden and costs. Once this methodology is complete, IRS will update this information collection to reflect a more precise estimate of burden and costs.”[15]

As that illustrates, in many cases the IRS simply does not have sufficient feedback from taxpayers to incorporate an expense estimate with many forms. Many of the collections in the database include the same IRS note listed above for Form 4562. This includes the notorious Form 1099-B, which takes up over 674 million hours of compliance. It is astonishing that the IRS expects to receive 1.4 billion submissions of this form, nearly 4 filings for every person in the country. It is no wonder that tax preparers consider it the worst tax form of all. Back in 2013, the IRS had requested information regarding expenses but received no responses. The IRS conducts surveys of taxpayers to gather data on time burdens and expenses. Collections are also posted for public comment in the Federal Register.

By taking some extra time to provide feedback to the IRS through its surveys and requests for feedback, taxpayers could do themselves a favor down the road. With better data, the IRS and policymakers will have a better idea of problem areas of the tax code, those which impose undue time and expense burdens relative to the amount of taxes they collect.

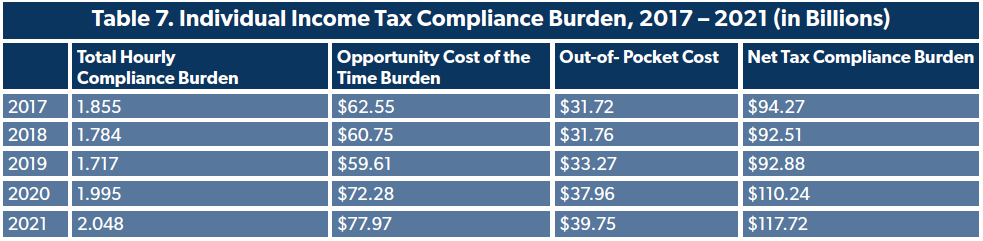

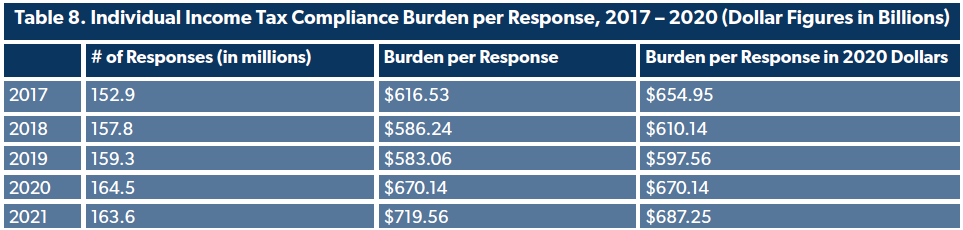

The Overall Individual Income Tax Compliance Burden

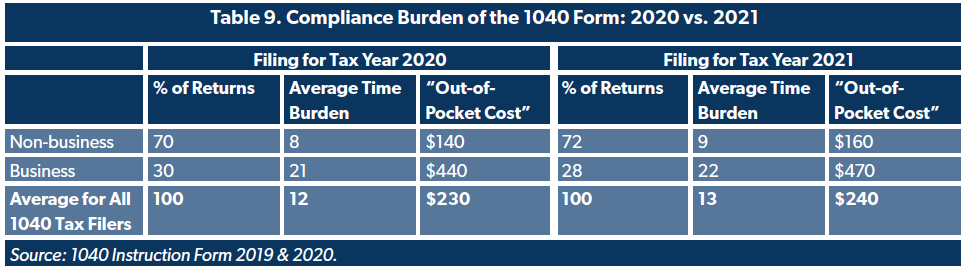

Some of the tax forms are targeted for very specific circumstances (including 53 with 100 or fewer respondents, eight with 10 or fewer, and two each with only a single respondent). The part of the tax code that most Americans are familiar with is the Form 1040 and its associated schedules and filings under the individual income tax. Reflective of the general upswing in complexity tracked in the data this year, the number of instructions associated with the 1040 and the primary schedules increased.

As shown in Tables 7 and 8, despite an estimated drop in the number of taxpayers filing individual income taxes, the overall hourly burden increased by 53 million hours.

The IRS notes that most of the change since last year is due to technical adjustments from updates to the macroeconomic model inputs factored into its taxpayer burden model and “from updated data and an improving 2021 economy that is also experiencing higher inflation.”[16] Additional changes were the result of legislative changes in ARPA, such as the expansion of the Earned Income Tax Credit to households with no children and the Advance Child Tax Credit, which will require taxpayers to reconcile amounts they received in advance with the amount they were actually eligible to receive. Some taxpayers may end up having to return a portion of the advance payments automatically made by the IRS. After all, opting out of the payments proved challenging because of online identification requirements the IRS established until it received pushback regarding privacy concerns. Combined, these added 12 million hours in compliance burdens and increased aggregate out-of-pocket costs by $165 million. Sometimes, when the government tries to help, it just ends up creating new problems for taxpayers.

It is also important to be aware that the experience of different taxpayers can vary greatly from the average time burden calculated by the IRS. Individuals have much lower time burdens than pass-through businesses that file individual income taxes.

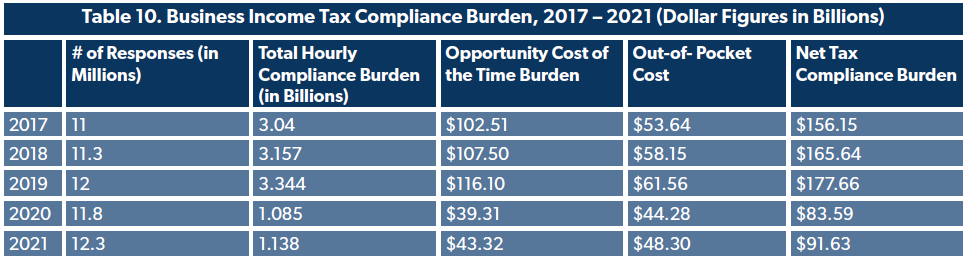

Business Income Tax Compliance Burden

Partnerships and corporations file taxes using Business Income Tax returns. The compliance burden ticked up because of an increased estimate of the number of filers and also because the IRS revised both its time compliance and expense estimates. The Supporting Statement did not go into great detail on the technical changes apart from noting updates to its macro estimates. The increase in filers is undoubtedly due to the economic improvements since last year, and the upward revision of expenses is likely attributable to the upswing in inflation.

Conclusion

The Supporting Statement for the Business Income Tax forms notes that the IRS’s compliance burden model “does not include a taxpayer’s tax liability, economic inefficiencies caused by suboptimal choices related to tax deductions or credits, or psychological costs.”[17] Obviously, this applies across the tax code, not just to business taxes.

NTUF has quantified the opportunity costs associated with the vast amount of time spent on tax forms, but it is difficult to replicate this for the costs of potentially poor choices in use of credits or deductions, let alone the level of stress and even dread that the IRS can instill in taxpayers who did their best to abide by the law. Many filers go on to experience compliance burdens long after Tax Day if the IRS has questions about the forms they submitted.

There are people who intentionally underreport income or attempt to fraudulently claim deductions they are not eligible for, but with the rising complexity of our code and the confusion many taxpayers face, many of those who make innocent mistakes on their taxes are treated like criminals by IRS enforcement agents. NTU and NTUF have chronicled too many horror stories of this over the years. Yet what we generally see in Congress is more funding into enforcement while taxpayer services lag behind and tax simplification reforms are left by the wayside.

The IRS compliance with the Paperwork Reduction Act is important to help identify problem areas of the tax code, but the gaps in the data reported above indicate that more work is needed to quantify the time and expense burdens and make the data available in a timelier manner, and with more detailed transparency describing the changes such as the IRS did with its re-baselining explainer. Taxpayers can play a role in this by filling out taxpayer burden surveys and providing public comment on IRS forms as they cycle through the Federal Register for regular review.

Ultimately, the burden of fixing our cumbersome and increasingly complicated and confusing tax code rests upon the shoulders of lawmakers in Congress.

[1] Wilford, Andrew et al. Taxpayers Desperately Need Help with Disastrous Filing Season. National Taxpayers Union Foundation. February 17, 2022. Retrieved from: https://www.ntu.org/foundation/detail/taxpayers-desperately-need-help-with-disastrous-filing-season.

[2] Office of Information and Regulatory Affairs. “Inventory of Currently Approved Information Collections.” Retrieved on April 7, 2022 from https://www.reginfo.gov/public/do/PRAMain.

[3] Bureau of Labor Statistics. “Employer Costs for Employee Compensation – December 2021.” March 18, 2021. https://www.bls.gov/news.release/pdf/ecec.pdf.

[4] Brady, Demian. Tax Complexity 2021: Compliance Burdens Ease for Third Year Since Tax Reform. National Taxpayers Union Foundation. April 15, 2021. Retrieved from: https://ntu.org/foundation/detail/tax-complexity-2021-compliance-burdens-ease-for-third-year-since-tax-reform.

[5] Internal Revenue Service. FY21 OMB 1545-0123 Rebaseline. 2021. Retrieved from: https://www.irs.gov/pub/irs-pdf/p5589.pdf.

[6] Wolters Kluwer, CCH. “Fact Sheet: 100-Year Tax History: The Length and Legacy of Tax Law.” 2013. Retrieved from: https://www.cch.com/wbot2013/factsheet.pdf.

[7] Office of the Law Revision Counsel. United States Code: Current Release Point. April 4, 2022. Retrieved from: https://uscode.house.gov/download/download.shtml.

[8] Office of the Law Revision Counsel. United States Code Classification Tables: 117th Congress, 1st Session. 2021. Retrieved from: https://uscode.house.gov/classification/tables.shtml.

[9] U.S. Government Publishing Office. Code of Federal Regulations (Annual Edition). 2021. Retrieved from: https://www.govinfo.gov/app/collection/cfr/

Note: Counts for some individual years may differ slightly from those reported in NTUF’s previous tax complexity studies. This is due to either reformatting or subsequent revisions of the posted volumes of regulations. For consistency, all the counts in Table 3 were completed on April 13, 2022.

[10] Internal Revenue Service. Understanding IRS Guidance – A Brief Primer. July 21, 2021. Retrieved from: https://www.irs.gov/uac/understanding-irs-guidance-a-brief-primer.

[11] Internal Revenue Service. VITA/TCE Volunteer Resource Guide. January 2021. Retrieved from https://www.irs.gov/pub/irs-pdf/p4012.pdf.

[12] Internal Revenue Service. Accounts Management and Compliance Services Overview. September 9, 2021. Retrieved from: https://www.irs.gov/irm/part21/irm_21-001-001.

[13] Internal Revenue Service, “Supporting Statement: Form 4562 Depreciation and Amortization (Including Information on Listed Property),” May 1, 2017. Retrieved from: https://www.reginfo.gov/public/do/PRAViewDocument?ref_nbr=201704-1545-011.

[14] Brady, Demian. Ibid.

[15] Internal Revenue Service, “Supporting Statement: Form 4562 Depreciation and Amortization (Including Information on Listed Property),” July 27, 2021. Retrieved from: https://www.reginfo.gov/public/do/PRAViewDocument?ref_nbr=202004-1545-027.

[16] Internal Revenue Service. Supporting Statement: U.S. Income Tax Return for Individual Taxpayers. January 21, 2022. Retrieved from: https://www.reginfo.gov/public/do/PRAViewDocument?ref_nbr=202111-1545-013.

[17] Internal Revenue Service. Supporting Statement: U. S. Business Income Tax Returns. January 24, 2022. Retrieved from: https://www.reginfo.gov/public/do/PRAViewDocument?ref_nbr=202108-1545-016.