(pdf)

Introduction

The newest COVID-19 relief bill from Congress – S. 178, the Delivering Immediate Relief to America’s Families, Schools and Small Businesses Act – could be a rare instance of big-ticket legislation that might actually cost less than its Congressional Budget Office (CBO) score. Also known as the “skinny relief” bill, its $529 billion price tag may be enormous on its own but it is much smaller than other trillion-dollar economic relief proposals, with new expenditures that are more targeted and provisions that repeal unused spending authority from previous pandemic relief packages enacted by Congress. However, CBO is scoring extensions of pandemic unemployment benefits – which comprise half of the bill’s spending – based on outdated projections from May rather than more recent data accounting for faster recovery than anticipated in the darkest month of the crisis.

Spending and Revenue Changes in the Proposal

The skinny relief bill, offered by Senate Majority Leader Mitch McConnell (R-TN) as an amendment to S. 178, is a pared back version of a much larger previous relief package. On August 6, Republican Senators introduced a set of stand-alone bills collectively referred to as the HEALS Act.[1] The package was loaded with spending provisions unrelated to the current crisis, including billions for defense programs and nearly $2 billion for a new Federal Bureau of Investigation’s headquarters.[2] Since the package was not voted on, CBO did not produce a cost estimate for the package but it was reported to cost around $1 trillion.[3]

CBO projects the skinny relief bill would increase spending by $384 billion in FY 2021, $498.8 billion over five years, and $501.7 billion through 2030.[4]

The most expensive provision would extend Pandemic Unemployment Insurance through December 2020 with a benefit enhancement of $300 per week. CBO estimates this would cost $187 billion. However, CBO calculated the score using its May interim projection for the unemployment rate.[5] At the time, CBO estimated an unemployment rate for the fourth quarter of 2020 at 11.5 percent and that 2021 would experience an average rate of 9.3 percent for the year. But just a few months later, CBO’s July update forecast a much-improved economic outlook with a fourth-quarter calendar year unemployment rate of 10.5 percent and an average rate of 8.4 percent for 2021.[6]

If the economy continues to recover faster than the projections, the cost of extending unemployment assistance could be partially reduced. The latest information from the Bureau of Labor Statistics pegged the September unemployment rate at 7.9 percent.[7]

The second largest provision in the bill would provide supplemental funding authority of $258 billion for the Paycheck Protection Program (PPP) and extend the authority to guarantee loans through the end of the year. CBO determined that these funds would be available for FY 2021 but that the new budget authorizations would only result in $130 billion in outlays. The remaining 50 percent of the authorized amount would go unspent.

The third-largest section of the bill would establish a $105 billion Education Stabilization Fund to assist local school districts with re-opening and other COVID-related costs. CBO estimates that 60 percent of the funding would occur over the next two years, with the remainder spread out through 2027.

The bill would also provide $57 billion over five years for public health and services emergency funding, $20 billion in emergency aid to farmers, $10 billion for Back to Work Child Care Grants, and $500 million for fisheries disaster assistance.

On the revenue side, CBO estimates that because unemployment benefit payments are subject to federal income taxes, the Treasury would collect $670 million in additional tax revenues over the decade. In addition to the higher receipts due to expanded unemployment benefits, the bill includes a tax credit for donations to eligible nonprofits that provide scholarships. Eighteen states currently have tax-credit scholarship programs providing families with financing options to attend non-public schools.[8] CBO estimates this would reduce revenues by $15 billion over five years. The Act would also increase the limitation on deductions for charitable contributions, estimated to reduce revenues by $3 billion.

Rescissions

The bill also includes some measures to offset the new spending programs detailed above. Section 1002 reduces budget authority from a section of the CARES Act that provided $454 billion Federal Reserve Emergency Lending Facilities. In the budget score for the CARES Act, CBO did not estimate any net outlays from this budget authority. On a net-present-value basis, the income and costs from the credit activities would offset. Because of the original score, and because much of the authority remains unused, CBO determined that the skinny bill would reduce the authorizations by $254 billion but there would be no reduction in spending.

CBO made a similar determination for Section 1004 of the skinny bill that rescinds $146 billion in budget authority provided to the Paycheck Protection Program (PPP). The CARES Act created the PPP with funding of $377 billion. At the time, CBO estimated that the full amount of the budget authority of $377 billion would result in outlays.[9] About a month later, Congress enacted the Paycheck Protection Program and Health Care Enhancement (PPPHCE) Act which bolstered the PPP with an additional $321.3 billion. CBO again estimated that the full amount would be spent.[10]

In its September budget outlook update, CBO reduced its estimate of PPP outlays by $130 billion as demand for loans declined and budget authority to guarantee loans expired on August 9th.[11] But more of the PPP authorizations have expired since then, so the rescission of $146 billion was not scored as producing any actual savings.

It is still important to rescind budget authority for spending programs even though the money will not actually be spent. The new funding provided in the skinny bill was designated as emergency spending thus excluding it from statutory budget caps and related enforcement.[12]

While it was not technically necessary to provide for rescissions and offsets in the bill, it is good budget policy to do so. This is especially important because Congress frequently uses rescission of expired budget authority as worthless offsets to higher spending included in regular appropriations bills. A debate on this issue played out in 2018 when the President revived a long-dormant budget process and sent Congress a stand-alone rescissions package to eliminate expired and unspent budget authority. The package was eventually defeated because it would have diminished the value of gimmicks that appropriators use to paper over higher spending.

Deficit Impact

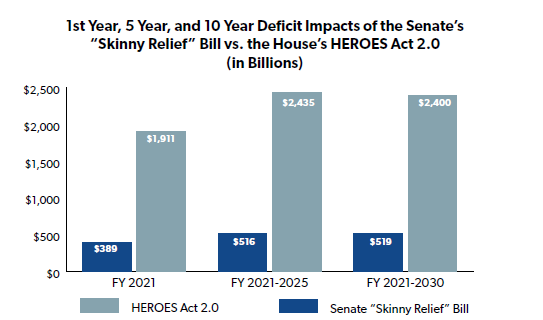

On net, the skinny relief bill would increase the 2021 deficit by $389 billion, and by $519 billion over the decade. House Democrats also scaled back their proposal for another round of pandemic and economic relief from $3.4 trillion in their original HEROES Act passed by the chamber in May to $2.4 trillion in the HEROES Act 2.0 passed by the chamber in early October. There is still a wide gap between the alternate versions.[13]

Conclusion

To date, Congress has enacted ten laws related to the pandemic and economic crisis with a total $2.4 trillion deficit impact over the decade.[14] Since the spring, shortly after passage of the $1.7 trillion CARES Act in late March and the $484 billion PPPHCE Act in late April, lawmakers have been debating on the need for another large-scale relief measure. No doubt due to political considerations, lawmakers were unable to agree on a deal for additional pandemic and economic relief with an election looming.

The debate will resume in November as the landscape for 2021 becomes clearer. As lawmakers consider additional relief, they should also remain cognizant of the yearly trillion-dollar deficits projected in the budget outlook. Additional relief should be temporary and targeted, and lawmakers should recommit to the bipartisan budget process reform discussions that had been making headway before this crisis.

[1] Senate Republican Policy Committee. (2020). “Update on the Coronavirus response: HEALS Act.” Retrieved from https://www.rpc.senate.gov/policy-papers/update-on-the-coronavirus-response-heals-act.

[2] Arnold, Brandon and Lautz, Andrew. “Congress Should Cut Extraneous Spending from HEALS Act.” National Taxpayers Union, July 28, 2020. https://www.ntu.org/publications/detail/congress-should-cut-extraneous-spending-from-heals-act.

[3] Stein, Jeff et al. “Here is What’s in the Senate GOP’s $1 trillion ‘Heals Act’ Package.” The Washington Post, July 27, 2020. https://www.washingtonpost.com/business/2020/07/27/senate-coronavirus-legislation-heals-act/.

[4] Congressional Budget Office. (2020). “Estimate for Senate Amendment 2652 to S. 178, the Delivering Immediate Relief to America’s Families, Schools and Small Businesses Act.” Retrieved from https://www.cbo.gov/system/files/2020-10/sa2652.pdf.pdf.

[5] Congressional Budget Office. (2020). “Interim Economic Projections for 2020 and 2021.” Retrieved from https://www.cbo.gov/publication/56351.

[6] Congressional Budget Office. (2020). “An Update to the Economic Outlook: 2020 to 2030.” Retrieved from https://www.cbo.gov/system/files/2020-07/56442-CBO-update-economic-outlook.pdf.

[7] Bureau of Labor Statistics. (2020). “The Employment Situation — September 2020.” Retrieved from https://www.bls.gov/news.release/pdf/empsit.pdf.

[8] EdChoice. “What is a Tax-Credit Scholarship?” Retrieved from https://www.edchoice.org/school-choice/types-of-school-choice/tax-credit-scholarship/ (Accessed October 2020.)

[9] Congressional Budget Office. (2020). “Preliminary Estimate of the Effects of H.R. 748, the CARES Act,

Public Law 116-136, Revised, With Corrections to the Revenue Effect of the Employee Retention Credit and to the Modification of a Limitation on Losses for Taxpayers Other Than Corporations - Revised April 27, 2020.” Retrieved from https://www.cbo.gov/system/files/2020-04/hr748.pdf.

[10] Congressional Budget Office. (2020). “CBO Estimate for H.R. 266, the Paycheck Protection Program and Health Care Enhancement Act as Passed by the Senate on April 21, 2020.” Retrieved from https://www.cbo.gov/system/files/2020-04/hr266.pdf.

[11] Congressional Budget Office. (2020). “An Update to the Budget Outlook: 2020 to 2030.” Retrieved from https://www.cbo.gov/publication/56517.

[12] Giroux, Matthew. “Budget Bulletin: Emergency Designations: Variations and Use.” Senate Committee on the Budget, June 30, 2016. https://www.budget.senate.gov/imo/media/doc/Emergency%20Designations%20BB063016.pdf.

[13] Brady, Demian. “HEROES Act 2.0 Would Boost Deficits by $2.4 Trillion.” National Taxpayers Union Foundation. October 21, 2020. https://www.ntu.org/foundation/detail/heroes-act-20-would-boost-deficits-by-24-trillion.

[14] Senate Budget Committee. (2020). “Coronavirus Resource Center: Budgetary Effects of COVID-19 Legislation.” Retrieved on October 29, 2020 from https://www.budget.senate.gov/coronavirus.